Image © Adobe Images

The Dollar-Yen exchange rate has fallen a further 0.20% to reach 104.62 at the time of publication on Tuesday. Analyst Richard Perry of Hantec Markets continues to favour the Yen over the Dollar, based on his studies of the technical setup.

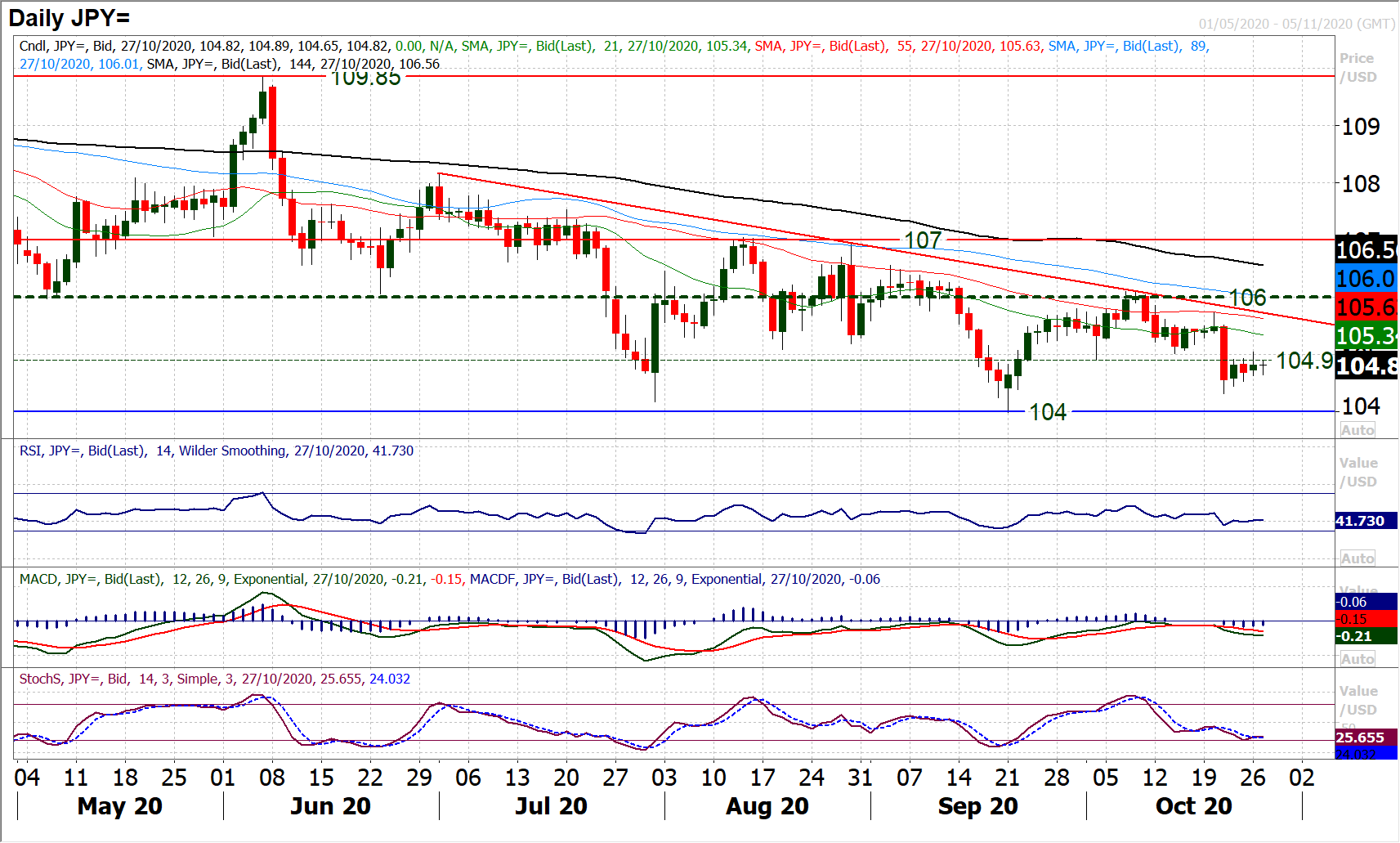

Since the big breakdown last week below 104.90, there has been an attempt to build support on Dollar/Yen.

A moderate pick up over the past few sessions has set in, but the bulls have been unable to get any real progress going in a recovery.

We consistently see overhead supply between 104.90/105.20 as restricting the rally.

This is continuing this morning and there is no change to our view that we see Dollar/Yen as a sell into strength.

The barrier of a four month downtrend comes in around 105.75 now, just around last week’s latest lower high.

Even if the dollar can eek out some marginal gains versus the yen in the coming days, we would be looking for another lower high between 104.90/105.50 area.

Momentum remains correctively configured (especially RSI and MACD) and near term strength appears to be fleeting before selling pressure resumes.

With a run of higher lows in recent sessions, 104.65 (yesterday’s low) is initial support, and a breach would simply re-open pressure on 104.30 again.

We continue to favour short positions towards 104.00 in due course. A close above 106.10 is needed to seriously suggest a sustainable recovery is underway.

Whilst markets have seemingly been hopeful (or should that be “duped”?) by the apparent signs of progress in the fiscal stimulus negotiations, as yet, there is nothing to show for it.

We are now just one week before polling day for the US Presidential and Senate election (where 35 of the 100 seats are up for re-election).

Despite the Democrat House Speaker Pelosi remaining “optimistic” there is an apparent fatigue setting in for market sentiment.

Agreement will not happen before the elections and after that, it is open to significant uncertainty on the results.

This lack of certainty on fiscal stimulus, coming as COVID-19 infections hit record levels in the US and the second wave takes full force across Europe, is leaving markets increasingly nervous.

Equities felt the full force of these concerns yesterday as Wall Street fell sharply, also with the dollar gaining strength on a safe haven bias.

There is a slight unwind of these moves early today, but how far this develops in the coming days will be shown through bond markets.

A flattening of the US yield curve (which continues this morning with US 2s/10s spread narrowing) would reflect risk aversion.

Wall Street futures have stabilised early today, but if bond yields continue to fall (and curve flatten), the dollar will climb and market sentiment will favour safe havens (such as the yen and the dollar)

It is a big US theme to the economic calendar today, but don’t forget the US announcements are an hour ahead this week as the daylight savings time shift is not until next weekend.

US Durable Goods Orders are at 1230GMT with core ex-transport good expected to increase by +0.4% in the month of September (after a +0.6% increase in August).

The Case Shiller House Price Index for August is at 1300GMT and is expected to improve to 4.2% (after +3.9% YoY in July).

The key data release for the day is US Conference Board’s Consumer Confidence at 1400GMT which is forecast to improve slightly to 102.0 in October (from 101.8 in September).