Image © Adobe Stock

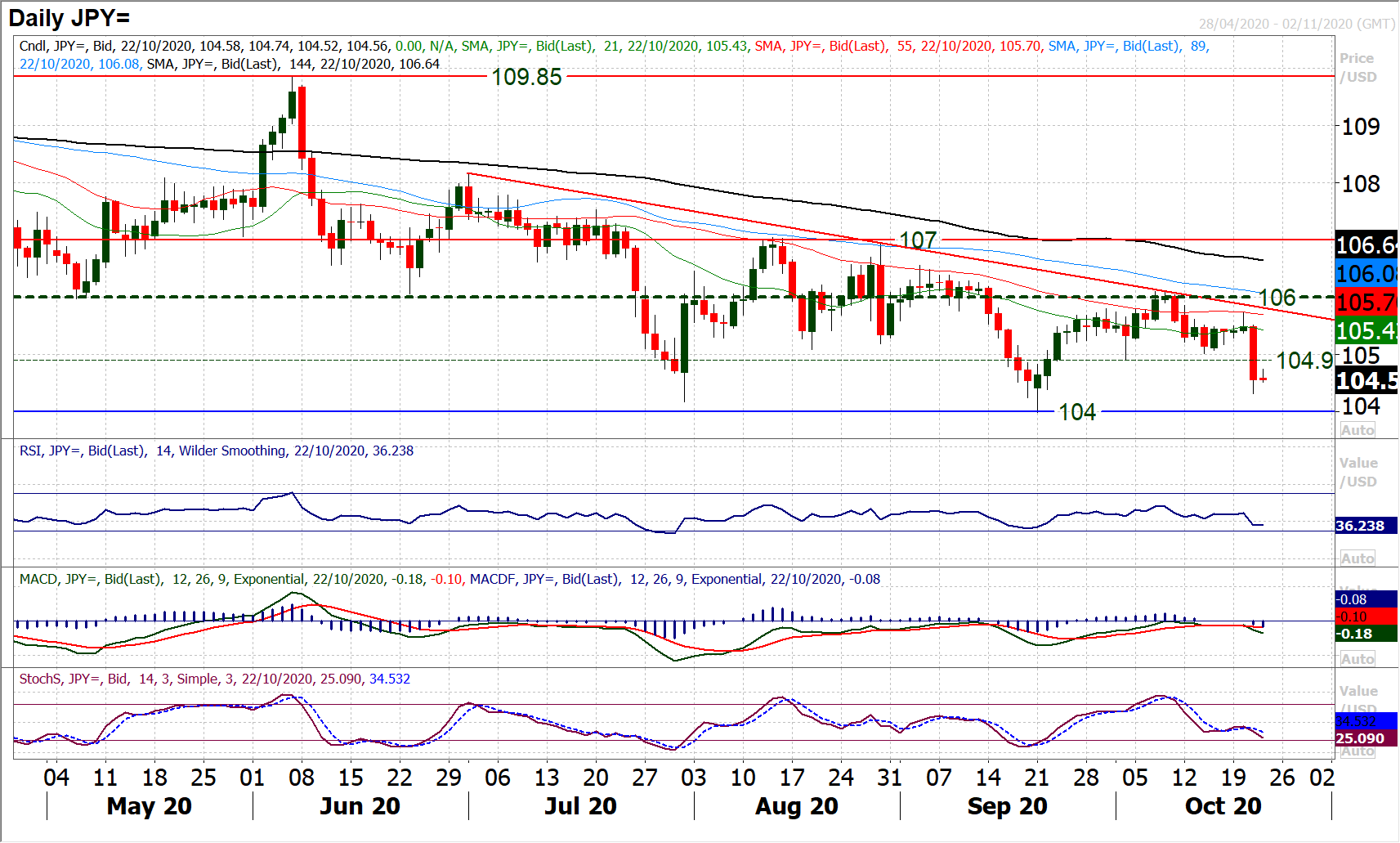

The Dollar-Yen exchange rate fell a sizeable 0.88% on Wednesday and is seen at 104.50 on Tuesday. Following the sizeable move, analyst Richard Perry at Hantec Markets considers the potential next levels the pair might achieve.

The dust is still settling on some significant dollar selling yesterday.

Dollar/Yen took a big dive to put an end to weeks of moves lacking conviction.

A decisive break below 104.90 has opened a test of 104.00 now.

We continue to see the strategy of selling into near term strength as being the best way to play the pair right now. Resistance is now overhead between 104.90/105.20 capturing the overhead supply of several old lows of the past few weeks.

Daily momentum indicators also renew their negative configuration and also with downside potential Under 104.00 the market is testing key March lows at 103.10 and then 101.15.

Already a dead cat bounce is beginning to roll over around 104.75 this morning. Yesterday’s low at 104.32 is initial support.

After weeks of uncertainty, suddenly there seems to be traction in two major macro factors, or at least this is what market reaction would suggest.

With Nancy Pelosi’s self-imposed 48 hour deadline, not really a deadline at all, the Democrats and the White House are seemingly close to agreement on fiscal stimulus.

The White House is apparently willing to offer $1.9 trillion, closer to the Democrats’ $2.2 trillion, but the talks continue over whether the two sides can actually sign something. The question is whether anything can be done before the election.

Although logistically, this is looking increasingly unlikely, no matter, the market is taking a view that this is a done deal nonetheless.

Subsequently the safe haven dollar has come under significant selling pressure and the market seems to be taking a view now.

On the other side of the Atlantic, the UK and EU have seemingly made enough progress towards their own agreement on a post-Brexit trade deal.

Talks will intensify now and will take place every day for the potential to have an agreement in place by mid-November.

Sterling has spiked sharply higher on this and unless there is anything to suggest talks breaking down, it should now be underpinned for the coming weeks.

However, despite all this, there are question marks in the market, reflected by the fact that equities are not sharply higher. In fact the one key indicator of risk appetite is under pressure.

Wall Street closed lower yesterday and futures are lower again today. Oil is also under pressure. This is a significant disconnect with yesterday’s market moves.

Watch to see if bond yields begin to unwind again, something which would play into corrective pressure on equities.

There is a bit of a US focus to the economic calendar today. The Weekly Jobless Claims at 1330BST are expected to improve to 860,000 (down from last week’s unexpectedly high 898,000). US Existing Home Sales at 1500BST are expected to increase by +5% to 6.30m in September (from 6.00m in August). The Eurozone Consumer Confidence is at 1500BST and is expected to deteriorate in October to -15.0 (from -13.9 in September).

There are a couple of Bank of England speakers this morning to watch for. The BoE’s Chief Economist Andy Haldane speaks at 0930BST, with Haldane often seen as a controversial speaker. Then at 1025BST BoE Governor Andrew Bailey also speaks, where any comments about negative rates are sure to be pounced upon.