Image © Adobe Images

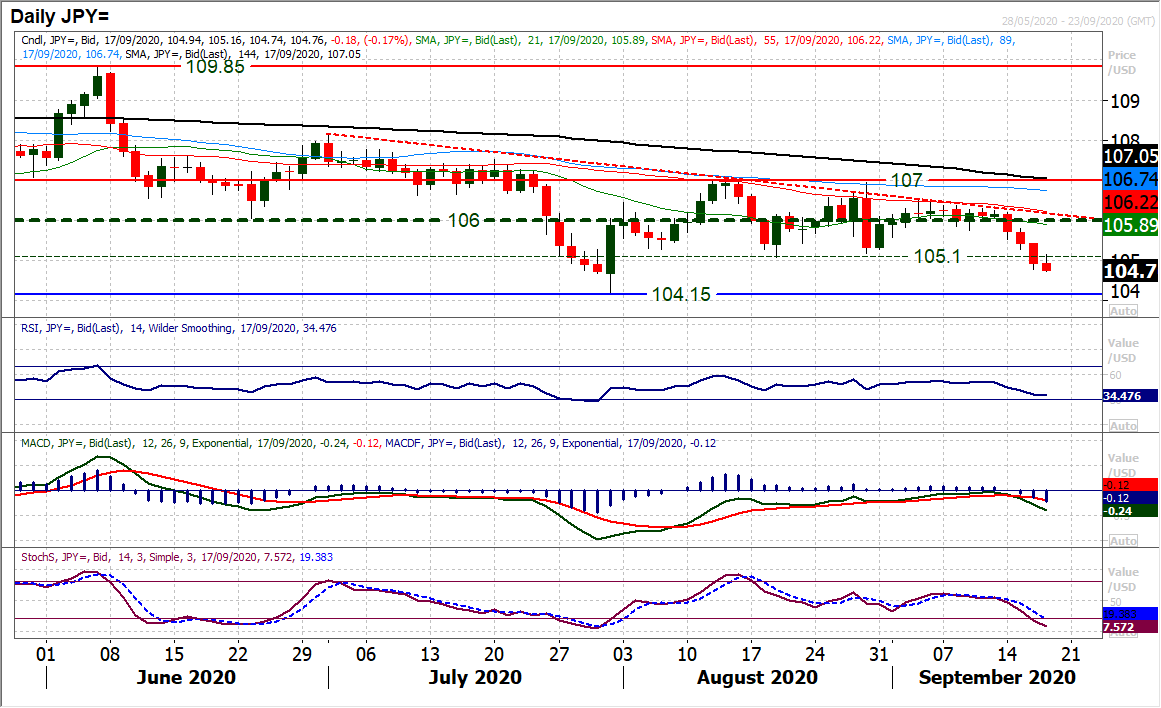

The USD/JPY exchange rate is seen at 104.77 as the Yen's 'ultra safe haven' credentials come into play amidst a clear 'risk off' market event. Analyst Richard Perry of Hantec Markets says the exchange rate is undergoing a breakdown that could yield further gains for the Yen.

The dollar failed to get any traction out of the yen in the wake of the FOMC decision (largely due to the subdued moves on US Treasuries).

Although there has been a basis of support forming overnight on USD/JPY, yesterday’s closing breach of 105.10 is an important break.

It completes a range breakdown of just under 200 pips and certainly opens pressure on 104.15.

The apparent lack of dollar rebound plays into this. Technical momentum indicators swinging lower with downside potential suggest that near term rallies are a struggle now.

The hourly chart shows resistance mounting at 105.30/105.55 as an intraday sell-zone under the more considerable resistance 105.75/106.00. Initial support is at 104.80 but we expect 104.15 to be tested in due course.

Below that there is minor support at 103.10 before the March spike low at 101.17. Key resistance remains 106/107.

In the wake of Fed chair Powell’s speech at Jackson Hole, markets have had a few weeks to position for a new dovish paradigm of FOMC monetary policy.

As part of its new average inflation targeting policy, yesterday the Fed statement says that it will “aim to achieve inflation moderately above 2% for some time”.

It was a high bar that the Fed needed to overcome for renewed dollar weakening. It appears that they have missed it.

In not defining the “time” (either with a level or length of time) this led to a couple of dovish FOMC members dissenting the move (Kashkari and Kaplan).

Although the FOMC dot plots suggest rates are on hold at least until 2023, the market took this as not hitting dovish expectations.

The dollar has notably strengthened across the forex major pairs as a result, whilst Wall Street has slipped back.

This Fed meeting certainly does not change the narrative of looser for longer, but for now, there is a kick back and potential near term short covering dollar rally.

It will be interesting to see how long this lasts before the medium term dollar correction resumes. Resistance at 93.50/94.00 on Dollar Index is key.

The Bank of Japan as expected has left rates unchanged at -0.1% and the 10 year JGB target yield of 0%. The yen has held up well on the back of this amidst a strengthening dollar. Traders will also be looking out for how dovish the Bank of England leans today.

After the BoJ overnight, there is one more major central bank on the economic calendar, with the Bank of England announcing monetary policy, along with a smattering of US data too. First up though is the final reading of Eurozone inflation for August.

After the surprise move to headline deflation, Eurozone headline HICP is expected to remain at -0.2% (-0.2% flash, +0.4% final July), whilst Eurozone core HICP is expected to remain at +0.4% (+0.4% flash, +1.2% final July).

The Bank of England is announcing monetary policy at 1200BST which is expected to once more be kept steady, with the interest rate of +0.1% and asset purchase stock at £745bn.

The vote on rates is expected to be unanimous. The US data is all released at 1330BST with the Weekly Jobless Claims expected to once more reduce, to 850,000 last week (from 884,000 previously).

The Philly Fed Business Index for September is expected to drop slightly to +15.0 (from +17.2 in August). US Building Permits for August are expected to improve by +2.5% to 1.52m (from 1.48m in July), whilst US Housing Starts are expected to decline by -1.2% to 1.48m (from 1.50m in July).