Image © Adobe Images

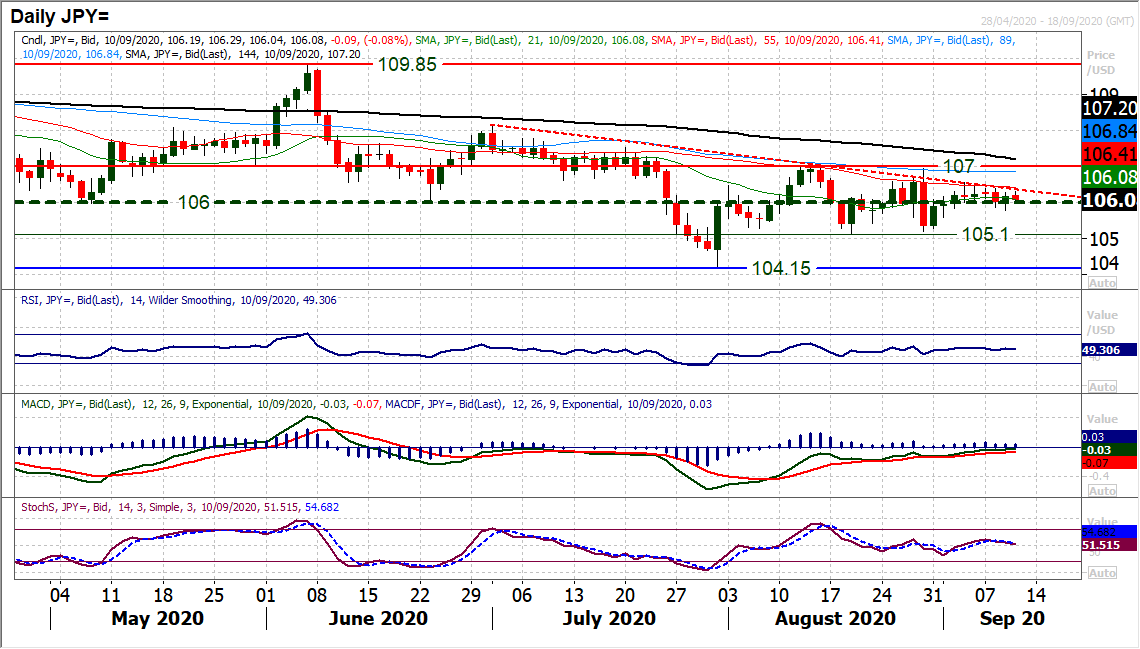

The Dollar-Yen exchange rate is at 106.11 at the time of writing on Thursday and despite the consolidation underway analyst and technical forecaster Richard Perry of Hantec Markets continues to favour the Yen over the Dollar.

An intraday bounce into the close has once more neutralised the outlook on Dollar-Yen.

A range between 105.10/107.00 is into its sixth week now and given the tendency for the market to gravitate around 106.00 (an old mid-range pivot) it is difficult to take much of a decisive near to medium term view right now.

Our bias remains to sell into strength though.

The old key floor for the summer months between 106/107 is now broadly resistance and a barrier to gains.

The resistance also comes in with the 55 day moving average (today at 106.40) and a 10-week downtrend (at 106.35 today).

However, conviction is lacking right now in the near term moves.

A close under 106.00 would see our preferred test of 105.10 resume.

Initial resistance 106.40/106.55.

The ECB meeting dominates today’s economic calendar.

European Central Bank monetary policy is announced at 1245BST with no change to the main refinancing rate of 0.0% or the deposit rate of -0.50%.

However, the react action will come with the assessment of forward guidance.

Will an “average” inflation element be introduced? Will the PEPP purchases level be increased, and by how much?

The press conference of ECB President Lagarde is at 1330BST and should also be watched for the assessment of inflation and the strength of the euro.

Aside from the ECB, at 1330BST Weekly Jobless Claims are expected to improve further to 846,000 (down from 881,000 last week). The EIA Weekly Crude Oil inventories are a day late due to Labor Day and are at 1600BST with an expectation of a drawdown of -1.1m barrels (-9.3m barrels last week).

The wild ride on Wall Street continued yesterday as the beaten down tech sector found support for a rebound. The question will now be how sustainable is this support and whether the recent sell-off is over.

The impact on broader sentiment has been significant too. A dollar rally has coincided with the recent tech sell-off, however, now with tech (and Wall Street) rebounding, we see the dollar coming off again. This is being seen through major forex, whilst gold has also ticked higher.

The focus for today will again be on the path of US futures, but also looking towards the ECB policy decision. A rebound on the euro came yesterday on reports that ECB members were confident of the Eurozone economic outlook, however, will this be the stance of ECB President Lagarde today.

How does the ECB react to the record low on core inflation? Also what of the strength of the euro, which induced ECB chief economist Philip Lane to concern over its impact on the Eurozone economy? There is a sense of consolidation early today. How dovish the ECB comes across will likely be another driver to the next EUR and by association USD move.