There is a view prevalent amongst analysts that the Dollar’s days are numbered: that the reflationary backdraught from Trump’s election promises has evaporated, that risky assets (equities, property) are overvalued and that growth will stall, dipping to 1.7% over the next few years.

“The third great Dollar rally of the post-Bretton Woods era is over,” announced Société Générale’s head strategist Kit Juckes, in a recent note, “the currency is in for a period of extended depreciation.”

Data released just before yesterday’s FOMC meeting would appear to support this after it showed a conspicuous flop in both inflation and retail sales – the engine room of the American economy.

Yet Fed Chair Yellen’s apparent dismissal of the dismal data and her insistence on highlighting the economy’s positives cautioned against too negative a view.

Martin Enlund at Nordea Markets suggests the Dollar is not, in fact, ‘down and out’ as suggested and that Dollar bears should exercise caution.

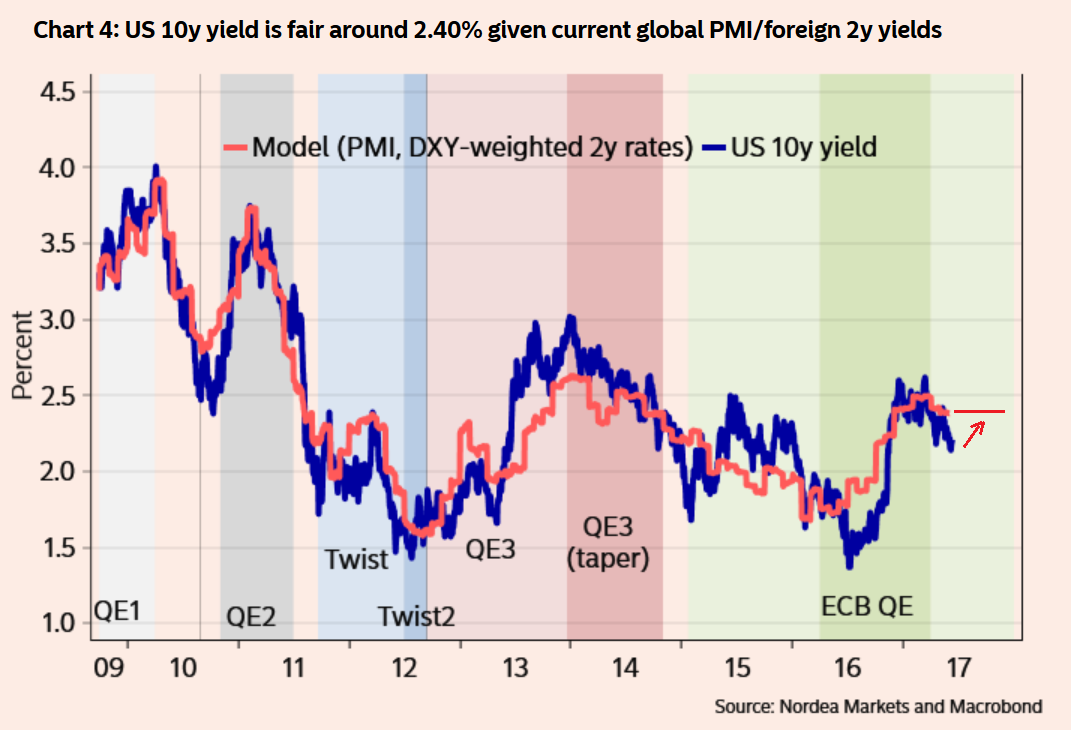

His argument stems from an analysis of US treasury yields, which tend to foretell of movements in the Dollar, because higher yields tend to attract more capital inflows.

“Doubting reflation has increasingly been the story in markets since March. In contrast to back then (when 10y yields traded above 2.6%...), it’s now easy to argue the case for lower yields based on for instance falling inflation rates or deteriorating business sentiment. Maybe it’s even too easy, which is why we want to offer some thoughts on why your flatteners / dollar shorts / yield-chasing strategies might be vulnerable…” said Enlund.

First, he notes how US data is likely to start surprising to the upside, and this will probably drive up 10-yr bond yields, and thus also the Dollar.

“The seasonal pattern since 2010 suggests the US surprise index - currently the lowest within the G10 - will head higher over the next few months.”

In the chart below, which compares 10-year yields to a proprietary indicator based on the US economic surprise index and US futures positioning, the indicator has risen strongly recently and is about to enter the “Risk of Higher Yields” zone, whilst at the same time actual yields have strangely dipped.

This non-confirmation suggests yields are lagging but cannot ignore the ignals form surprise and positioning for too long, and are therefore likely to rise, eventually, in corroboration.

The next chart shows US Dollar/10-year futures market positioning at a bearish extreme not exceeded since 2006, whilst a proxy for fair value (the 10year/2year spread) is much elevated.

This suggests positioning will not remain bearish for too long before climbing back up towards fair value.

Enlund suggests the US Fed’s disposal of its balance sheet assets could be a driver of such a rise.

“Stronger data, or if the Fed opts to use its balance sheet to tighten, these positions should be vulnerable (the consensus is that a shrinking Fed balance sheet will lead to lower prices/higher yields as one important buyer disappears from the market,” said Nordea’s chief analyst.

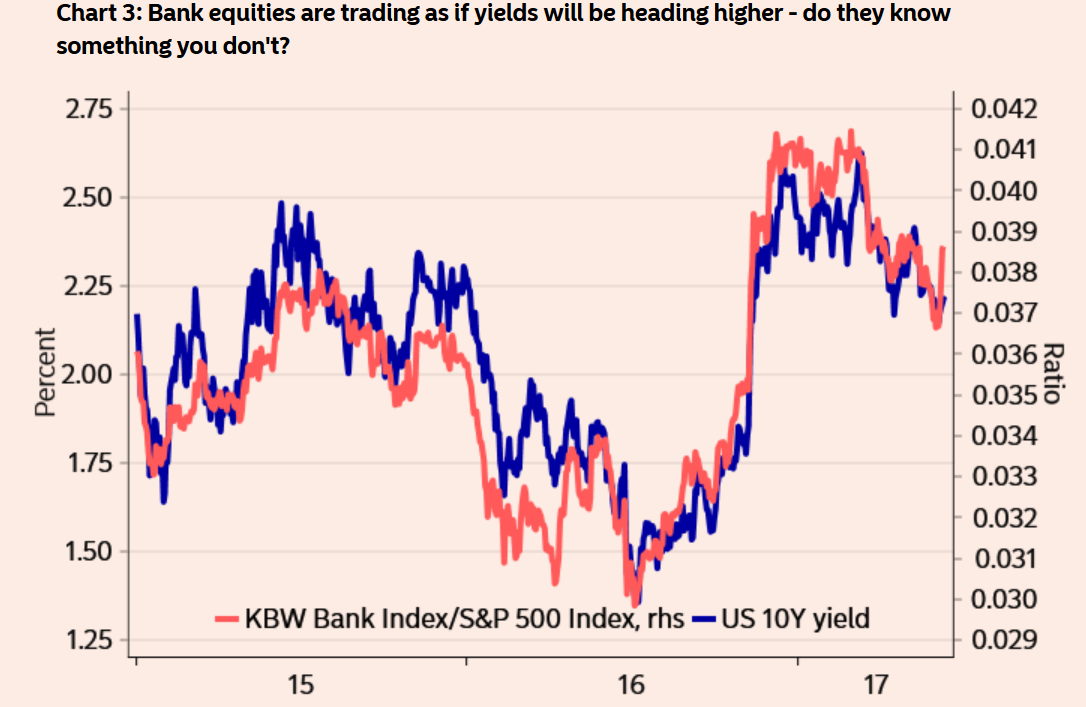

Equity markets may also be signalling further upside for both yields and the Dollar as Bank stocks are on the rise, despite fears about equity ‘overvaluation’.

“Could it be that equity markets are smarter than bond markets currently?

“Sounds far-fetched, I know, but still banks are trading as if yields are heading higher. Maybe this is a warning sign,” said Enlund.

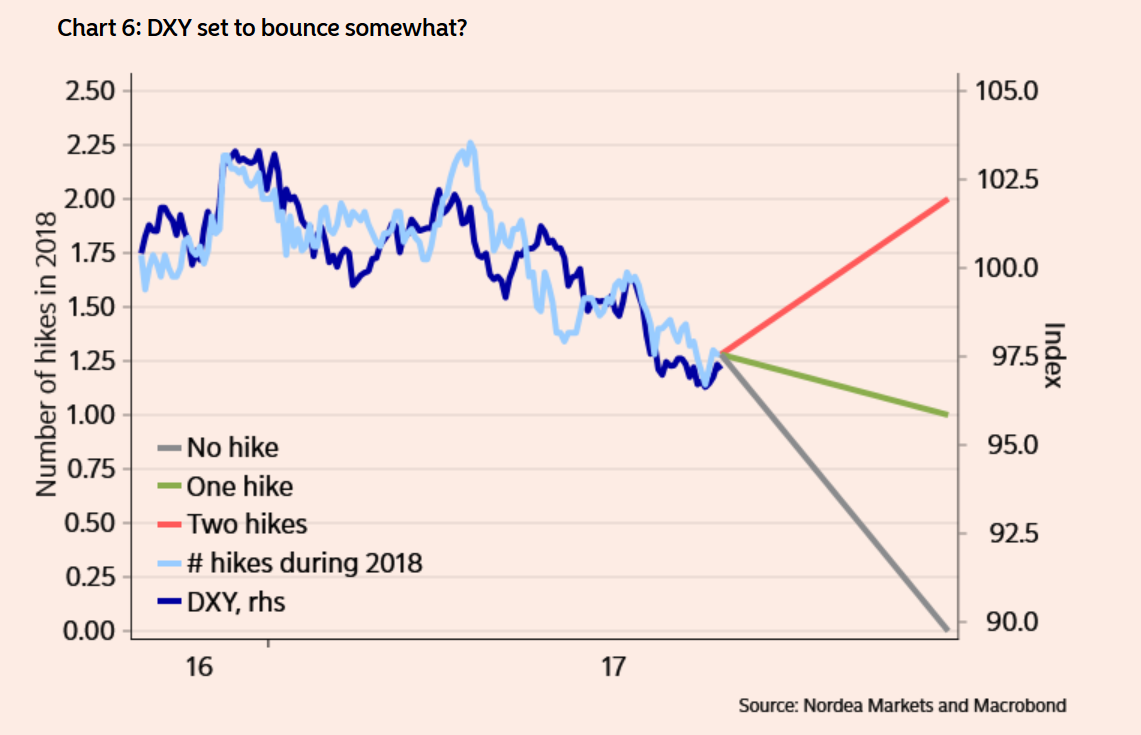

Enlund’s analysis of both the 10-year yield and the Dollar’s likely trajectory in different scenarios - based on how many times the Federal Reserve hikes rates - seems to favour their current trajectory, based on Fed expectations of 1 hike in 2018.

These projections are illustrated in the chart below and illustrate that one hike is the bare minimum which should be expected.

Given there will probably be more than just one hike in 2018, however, the risk is to the trajectory rising.

“The US 10y yield has correlated nicely with 2018 Fed hike expectations recently. Given only one rate hike priced in for 2018, the downside in Fed pricing / yields should thus be limited - even if the Fed is fairly dovish. Putting it simply, it should be hard for markets to expect less than one hike in a non-recession scenario,” said the Nordea Strategist.

Similar scenario modelling for the Dollar Index (DXY) tells the same tale - of limited downside, bar a recession, and probably more likely more upside.

“A bounce in the surprise index over the next few months implies that the USD should fare better. Indeed, we are looking for a short-term recoil in EUR/USD, providing better opportunities for going long,” said Enlund.