Image © Adobe Images

The British pound's recent recovery leaves it well poised against the dollar.

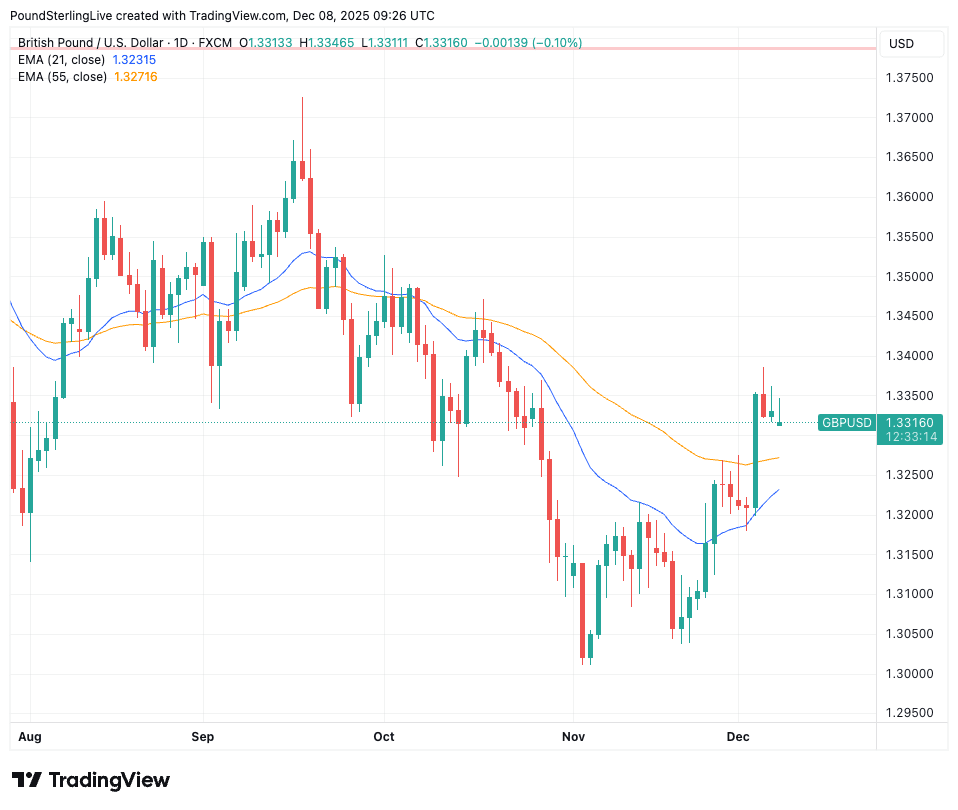

The pound to dollar exchange rate (GBP/USD) rose to its highest level since October 21 at 1.3385 last week, in a surge that flips the short-term outlook to constructive.

The move saw the pair break above the 21-day and 55-day exponential moving averages (EMA), which is a sign of building upside momentum.

From here, we would anticipate further upside and a potential test of 1.34 later in the week, provided the Federal Reserve decision doesn't rejuvenate the dollar (more on this below).

That being said, we are also not surprised to see GBP/USD coming under some pressure in the early stages of the new week on account of building nerves ahead of the Fed decision.

Weakness could prompt a test of the 55-day EMA at 1.3271, but there should be enough support ahead of this to verify our stance that weakness is likely to be shallow at this juncture.

Of course, the dollar could roar back to life and upend these predictions if the Federal Reserve policy decision, due Wednesday, strikes a particularly 'hawkish' tone.

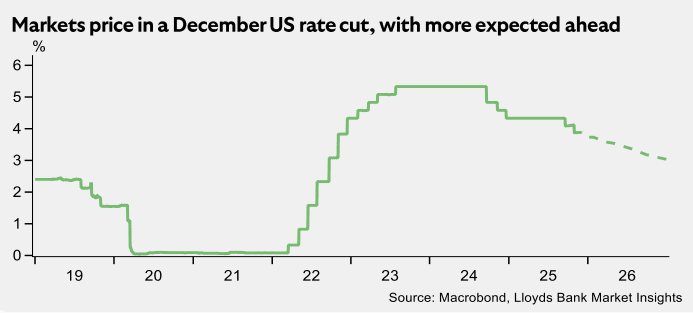

Markets have almost fully priced in a 25 basis point interest rate cut, which would take the Fed funds target range to 3.50–3.75%, leaving it to the guidance and updated forecats to set the agenda for dollar exchange rates.

The decision to cut will rest on a series of economic surveys that confirm the labour market is softening.

Last week saw GBP/USD jump to 1.3333 after the U.S. November ADP employment report read -32k, disappointing consensus expectations for a 10k gain in employment.

Highly accurate consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

The rate cut itself won't be remarkable enough to drive any sizeable FX market reaction.

Instead, it's the outlook for interest rates in 2026 that will be of greater interest. Here, there's uncertainty owing to divisions within the Fed's FOMC.

"Some members remain concerned about inflation staying above target, while others place greater emphasis on signs of labour market weakness," says Hann-Ju Ho, Senior Economist at Lloyds Market Insights.

The Fed’s statement and Chair Powell’s press conference, along with updated economic projections, will also provide insight into policy intentions for 2026. This meeting includes updated forecasts, including interest rate projections (the dot plot).

Above: What markets expect from the Fed.

"The September projections showed a consensus of 3.625% for end-2025, consistent with a 25bp cut on Wednesday, but only 25bp of additional easing in 2026, less than markets currently expect. It will be interesting to see whether the dot plot projection shifts, given the current divisions within the Committee," says Hann-Ju Ho.

In the UK, the central bank will also be in focus, even if we are still ten days out from the next interest rate decision.

From Monday through Tuesday, Bank of England MPC members Lombardelli, Taylor, Mann and Dhingra will cross the airwaves, with a number appearing before Parliament's Treasury Select Committee.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

They represent a good mix of stances towards monetary policy, and we would expect some convergence towards verifying market expectations for a rate cut on December 18 and then again in 2026.

With a December hike in the price, we think the British pound will be more sensitive to guidance as to what happens in 2026.

Here, Governor Andrew Bailey's address to the FT Global Boardroom event in London, will be key.

He will deliver the remarks Thursday, and there's a chance he will sound more confident about further rate cuts, which should weigh on the pound, all else equal.

The key UK data release in the coming week is October GDP, due Friday. Economists expect subdued economic momentum to have persisted, with flat growth at the start of the quarter.

This points to downside risks for the Bank of England's baseline forecast of 0.3% growth in Q4, which will only encourage a sense that interest rates need to come down.