Image © Adobe Images

Pound Sterling resumes its selloff against the U.S. Dollar amidst heightened tariff fears.

The U.S. Dollar is outperforming global peers as markets digest weekend tariff developments that saw Donald Trump carry out his threat to impose a 25% import tax on Canadian and Mexican goods.

The U.S. imposed a 10% tariff on Chinese goods and said the EU was also set to be tariffed. Canada announced retaliatory tariffs, and Mexico and China said they would do the same.

The context of the moves is important: since the President's inauguration, the sense in FX markets was that Trump was watering down threats and the worst-case tail-risk scenarios were being priced out. As a result, the Dollar weakened.

However, on Monday, the direction of travel is certainly bullish for dollars.

"Trade War 2.0 begins," says Rohit Arora, Strategist at UBS. "With markets underpricing tariffs premium, our global strategists maintain a preference for Quality and defensives in equities, and for USD and JPY vs. CNH and EUR in FX."

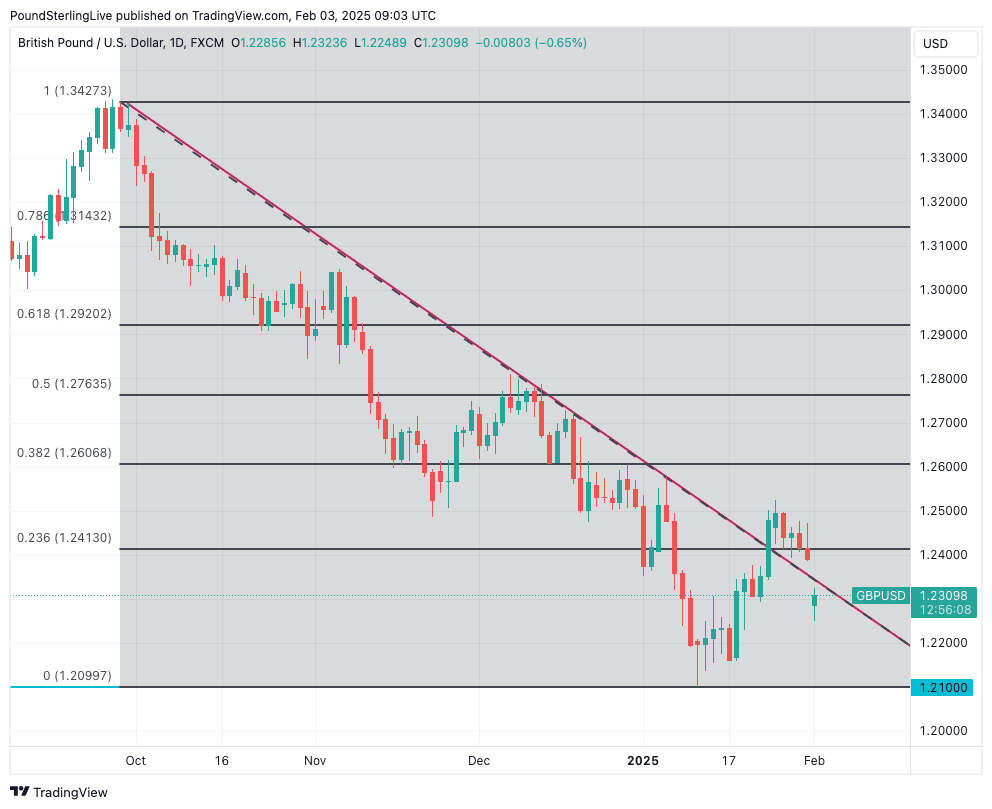

The Pound to Dollar exchange rate (GBPUSD) gapped lower in early Asian trade and looks set to resume a downtrend that has been in place since October 2024.

GBPUSD is back below the downtrend line, confirming the recent uptick was a counter-trend relief rally. To be sure, a more concerted recovery would have emerged had Trump shied away from imposing tariffs, but GBPUSD is now forecast to test year lows at 1.21 ahead of a break lower.

Above: GBPUSD at daily intervals showing the post-October selloff.

The fundamental narrative is clear: the trade war 'trade' is to buy dollars. However, GBP does look better protected against USD strength than most G10 peers and GBPUSD weakness will be less severe than in other currency pairs.

This is because the UK has a rare goods trade deficit with the U.S., limiting any impact of potential tariffs.

In fact, GBP is the third-best performing G10, tagging alongside safe havens like the JPY and CHF, meaning it can carve itself a role as a relatively safe haven in the tariff trade era.

Highly accurate consensus projections for the next four quarters, compiled from leading investment banks.

Access the full forecast →

"The dollar surged as the tariff wars begin," says Dr. Win Thin, Global Head of Markets Strategy at Brown Brothers Harriman. "Sterling is outperforming as the U.K. avoids tariffs."

Trump's comments on the UK contrast with those about the EU, saying he would definitely proceed with tariffs against the EU as he says the bloc was treating the U.S. "very bad" with a $300BN trade deficit.

Simon French, lead economist at Panmure Liberum, says the UK has relatively little direct exposure to any tariffs on its goods exports to the U.S. ($64bn/year).

"The transmission is more likely to be a slowing of global economic growth, which the UK is geared into, and tighter financial conditions than the domestic economy needs," says French.

Week Ahead to be Dominated by Bank of England Decision

Tariff developments will be the preeminent driver of global FX, but Pound Sterling also has the Bank of England decision to look forward to.

A 25 basis point cut to Bank Rate is to be delivered, with the Monetary Policy Committee likely indicating it will maintain a cautious yet determined stance on delivering further cuts.

The message the Bank will want to put across is that it wants to maintain its quarterly pace of interest rate cuts, which implies a total of four for 2024. Current market thinking is that it will only be able to carry out three.

So, there is some potential for adjustment in fixed-income and foreign exchange markets towards accepting more cuts.

The textbook says this will weigh on the Pound, but the UK currency has already taken a sizeable hit in 2025 and the downside is looking far better protected than was the case at the start of the year when it looked richly valued.

For GBPUSD in particular, the Bank could prompt some volatility, but ultimately, it is the bigger global picture that will remain in charge. And here, all signs point to further weakness in the coming days and weeks.