Image © Adobe Images

Investors are being told to position for further spasms in the U.S. regional banking space, a development that could lead to further declines in some equities, bonds and the Dollar.

"After Silicon Valley Bank, Signature Bank, First Republic Bank and now potentially PacWest Bank, Western Alliance Bank and First Horizon Bank all having been subject to financial meltdowns, the proverbial cat will be very difficult to put back into the bag," says Pär Magnusson, Fixed Income Strategist at Swedbank.

U.S. bank stocks and the USD fell sharply again on Thursday, dragged down by fears PacWest and Western Alliance would be the next two regional lenders to cease operations.

As some banks come under pressure other banks in the sector tighten their lending conditions in order to shore up their own capital. This means leas money flowing into the economy, ultimately leading to a slowdown.

The Federal Reserve therefore need not raise interest rates further and money markets now show 100 basis points of cuts are expected by year-end.

Expectations for rate cuts weigh on U.S. bond yields which in turn leads to losses by the Dollar.

Sterling has meanwhile emerged as a relative 'safe haven' amidst the banking crisis as the UK has avoided the issues seen in the U.S. and Europe (where Credit Suisse was rescued by UBS).

UK banks saw increased regulations and capital holding requirements following the 2008 financial crisis with authorities seeking to ensure another crisis would never again be repeated.

U.S. banks also saw stricter rules and regulations, but these were eased under the Trump administration when regulations were loosened to boost growth in the sector and the economy.

"It is hard not to see the irony of regional U.S. banks having successfully lobbied for less regulations during the Trump administration only to find that less regulations now is making them vulnerable to bank runs," says Magnusson.

A 2018 Trump law allowed regional banks to break free from annual Federal Reserve stress tests that forced them to maintain certain levels of capital and liquidity to ensure they could withstand bouts of elevated withdrawals.

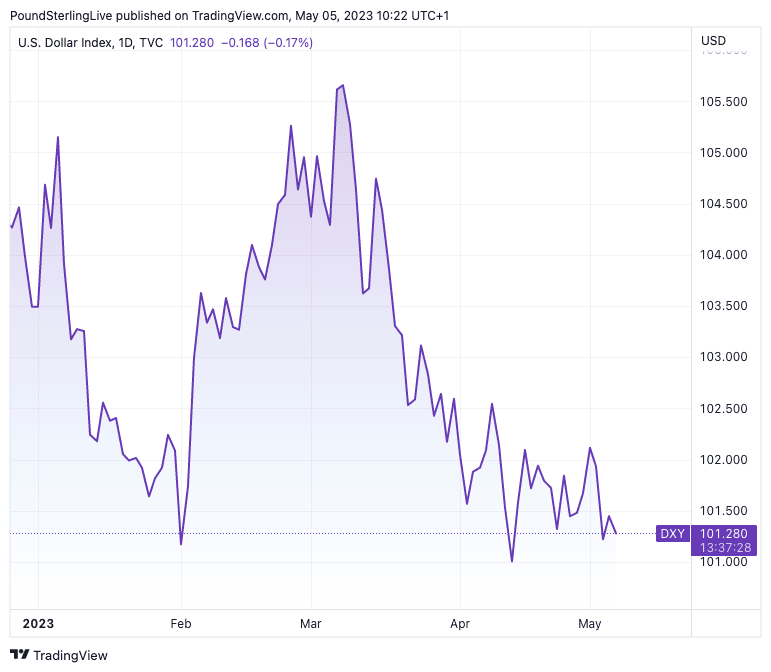

Above: The Dollar index is under pressure.

Magnusson explains a number of issues that have put U.S. regional banks are now unable to meet customer deposit withdrawal requests:

The first - and this was particularly relevant to SVB which failed in March - was the heavy investment in long-term government debt.

The value of this long-term debt has fallen as the Federal Reserve hikes interest rates, meaning the likes of SVB saw their asset base shrink at a time when depositors were increasingly eager to withdraw their deposits.

Another issue relates to the exposure of regional banks to real estate lending, an obvious vulnerability when property values fall in response to higher mortgage costs.

Data shows the average exposure to commercial real estate loans among regional banks is 29%, whereas it's only 6% among large banks.

"The U.S. regional bank crisis is spreading. With every bank that succumbs to shrinking deposits and/or market distrust, the probability of more banks falling victim to similar fates grows. A vicious spiral may be about to take hold. A general risk-off reaction is becoming increasingly likely, and you should position for this risk," says Magnusson.

Given the Dollar has proven vulnerable to domestic banking issues, any deepening of the crisis could prompt further declines.

On the other hand, any sense that the crisis is over could spark a reversal higher in the Dollar, sending GBPUSD lower.

For now, though, this crisis continues to simmer, despite the best efforts of regulators.

GBP/USD Forecasts Q2 2023Period: Q2 2023 Onwards |