"We have learned over the past 18 months or so that one good core CPI print proves nothing, but we see good reasons to think this one is the real deal" - Pantheon Macroeconomics.

Image © Adobe Images

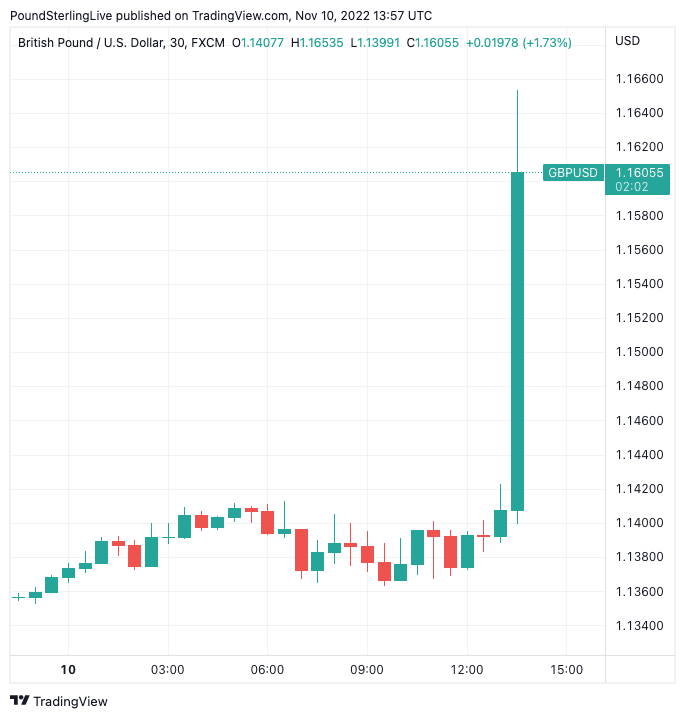

The British Pound leapt 2.0% against the U.S. Dollar and maintained a 1.0% advance against the Euro following the release of U.S. inflation data that was softer across the board and kept alive hopes the Federal Reserve would slow its pace of rate hikes.

The headline CPI inflation figure showed 0.4% month-on-month growth in October, slower than the consensus estimate of 0.6% and matching September's 0.4%.

In the year to October inflation rose 7.7% said the U.S. Bureau of Labor Statistics, defying estimates for 8.0% and marking a sharp slowdown on September's 8.2%.

Core CPI - a measure the Fed will be particularly interested in - rose 6.3% year-on-year, below estimates of 6.5% and below September's 6.6%. The month-on-month figure stood at 0.3%, a halving of the previous month's reading.

"Markets will positively receive today’s news, it should help bonds and equities in the short term while being a headwind for the US dollar," says Willem Sels, Global Chief Investment Officer at HSBC Private Banking and Wealth Management.

The Pound to Dollar exchange rate rose 2.40% to 1.1640, its highest level since September 13. This means those transferring into dollars via the typical high-street bank will see rates at approximately 1.14 on offer, but those using competitive payment providers will see rates just nudging 1.16.

Above: GBP/USD at 30-minute intervals showing the strong reaction to the U.S. inflation reading. To better time your payment requirements, consider setting a free FX rate alert here.

The Dollar was a percent lower against the Euro (1.0134) and 1.60% lower against the Australian Dollar (0.6534), with a loss of 0.90% registered against the Canadian Dollar (1.3403).

Looking ahead, Sels says "one swallow does not make a spring, and we should not conclude from today’s news that the inflation fight is over."

HSBC Wealth Management thinks the Fed will continue to hike rates to 5% and then keep them there throughout 2023 or even longer.

"It is only when the Fed finishes its rate hikes and the global economy is showing signs of stabilisation that equity markets can see a sustained bounce," says Sels, in an observation that could also prove pertinent for the Dollar.

Investors are paying particular attention to the details of the report, noting a slowdown in inflation across a broader spectrum of items.

"We have learned over the past 18 months or so that one good core CPI print proves nothing, but we see good reasons to think this one is the real deal," says Ian Shepherdson, Chief Economist at Pantheon Macroeconomics.

These include lower used car prices, a drop in some transport services, a decline in health care service prices and a lower increase in owner's equivalent rents.

"The fever appears to be breaking in rents, a few months earlier than we expected," says Shepherdson.

Food price inflation also slowed, but monthly energy inflation picked up.

"Inflation will continue to slow in coming months, which will significantly reduce the need for continued aggressive rate hikes. This reading supports our view of a 50bp hike in December," says Knut A. Magnussen, Senior Economist at DNB Bank.

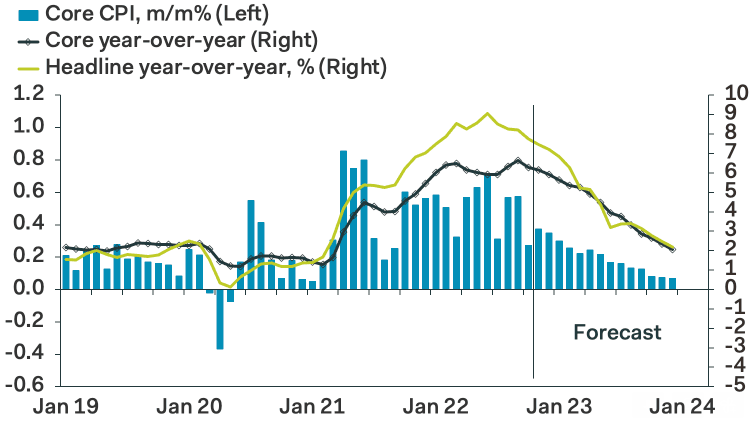

Above chart is courtesy of Pantheon Macroeconomics.

"U.S. inflation has probably passed its peak. However, a very rapid decline should not be expected, as rents in particular, the most important expenditure item, still showed no signs of easing in October," says Dr. Christoph Balz, Senior Economist at Commerzbank. "One should not read too much into a single data point".

Recent data suggests wage growth is trending lower while job creation has also peaked.

"If this is confirmed by the next jobs data and the November inflation figures, there is a lot to be said for a slower Fed pace. We maintain our forecast that the Fed will raise rates by only 50 basis points at the next meeting on December 13/14. Even smaller steps are to be expected at the beginning of 2023," says Balz.

Economists will now turn their attention to December's jobs and inflation reports, both of which will be the last major data point the Fed will account for ahead of their December decision.