- -GBP/USD back above 1.25 in thin, choppy holiday trade

- -Strong U.S. payrolls & PMI details an incitement for Fed

- -After policymakers indicate rates could leapfrog market

Image © Adobe Images

The Pound to Dollar exchange rate rebounded from earlier losses late this week but was hampered again in thin holiday trade on Friday after the May non-farm payrolls and Services PMI reports offered an incitement to a Federal Reserve (Fed) that appeared to become more hawkish in recent days.

Sterling’s Wednesday slide beneath the 1.25 handle was reversed as the Dollar declined broadly in holiday thinned trade on Thursday but the Pound was left spluttering by Friday after U.S. data appeared to invite the Fed to contemplate an even faster pace of interest rate rises in the months ahead.

“Overall, with hiring remaining at a solid pace, we’re clearly still on track for 50bps rate hikes at the next two FOMC meetings. We’ll need to see employment gains running well below the current pace to prevent the further tightening in labor markets that the Fed wants to avoid,” says Katherine Judge, an economist at CIBC Capital Markets, in reference to Friday’s non-farm payrolls report.

Official measures of U.S. wage growth softened slightly in May along with the pace of job growth, although perhaps not by enough to change much for the Fed, while the S&P Global Services PMI survey suggested employment, pay growth and inflation could all be likely to rise further up ahead.

Above: Pound to Dollar rate shown at hourly intervals alongside EUR/USD. Click image for closer inspection.

Above: Pound to Dollar rate shown at hourly intervals alongside EUR/USD. Click image for closer inspection.

“Inflationary pressures remained historically elevated in May. The rate of increase in cost burdens accelerated again to reach a new series high. Panellists stated that greater input prices stemmed from hikes in fuel, energy and supplier costs, alongside increased wage bills,” S&P reported.

The S&P Global PMI changed little in May, although it and some of the above details were contradicted by the equivalent Institute for Supply Management survey emerging a short time later, which fell 1.2 points to 55.9.

“The sector’s slowdown was due to a decline in business activity and slowing supplier deliveries. The Employment Index (50.2 percent) returned to expansion territory, and the Backlog of Orders Index grew, though at a slower rate. COVID-19 continues to disrupt the services sector, as well as the war in Ukraine. Labor is still a big issue, and prices continue to increase,” the industry body said.

What matters most is that both surveys suggested that demand for workers is still rising alongside their demands for wages and some other prices, as these are things that could stoke inflation and encourage the Fed to continue lifting interest rates in large increments through the rest of the year.

Source: ISM. Click image for closer inspection.

Source: ISM. Click image for closer inspection.

Weaker May regional PMIs and sharp falls in new and existing home sales suggest higher interest rates, higher costs and global uncertainties are beginning to sap US rebound momentum too. The labour market remains a pillar of strength for now," says Richard Franulovich, head of FX strategy at Westpac. "Against that backdrop, [Dollar Index] could range between 101-105 for a while, but a decisive long-term peak is not yet in place."

The Dollar rallied following both sets of data, pushing the Pound, Euro and other currencies lower following a Thursday recovery that had been accompanied by gains for risk assets and a further recovery by China’s influential Renminbi, which may also have impacted other currencies.

“The RMB continued to rally, acting as an offset to weakness in G10. Attention amongst market participants remained fixated on policy support, and possibly bargain hunting in asset valuation terms (the CNH rallied 0.28% vs the USD),” says Stephen Gallo, European head of FX strategy at BMO Capital Markets.

This came after fiscal and monetary policymakers in Beijing reportedly signalled that stimulus is on the way for the world’s second largest economy, which is also potentially positive for other trade oriented economies and currencies that have large linkages with China.

Above: U.S. Dollar Index shown at daily intervals alongside competing influences of key U.S. bond yields and Renminbi.

Above: U.S. Dollar Index shown at daily intervals alongside competing influences of key U.S. bond yields and Renminbi.

All of this rounded off a week in which various members of the Fed board and regional reserve bank presidents made clear they could yet elect to lift interest rates to, or even above the oft-referenced ‘neutral rate’ this year.

“With the interest rate moves we have made so far, the current target range of the federal funds rate is 75 to 100 basis points. This is well below the range of estimates of the longer-run nominal policy rate that would be neutral in the sense of neither stimulating nor restraining economic activity when inflation is 2 percent,” Federal Reserve Bank of Cleveland President Loretta Mester said.

“In my view, with inflation as elevated as it is, the funds rate will probably need to go above its longer-run neutral level to rein in inflation. But we cannot make that call today because it will depend on how much demand moderates and what happens on the supply side of the economy. So, we need to continue monitoring economic and financial developments closely,” she added in an address to the Philadelphia Council for Business Economics.

Elsewhere in Fed chatter Vice Chair of the board Lael Brainard indicated that current market pricing for interest rates is the least that should be expected, while board colleague Christopher Waller came across almost as hawkish as Federal Reserve Bank of St Louis President James Bullard.

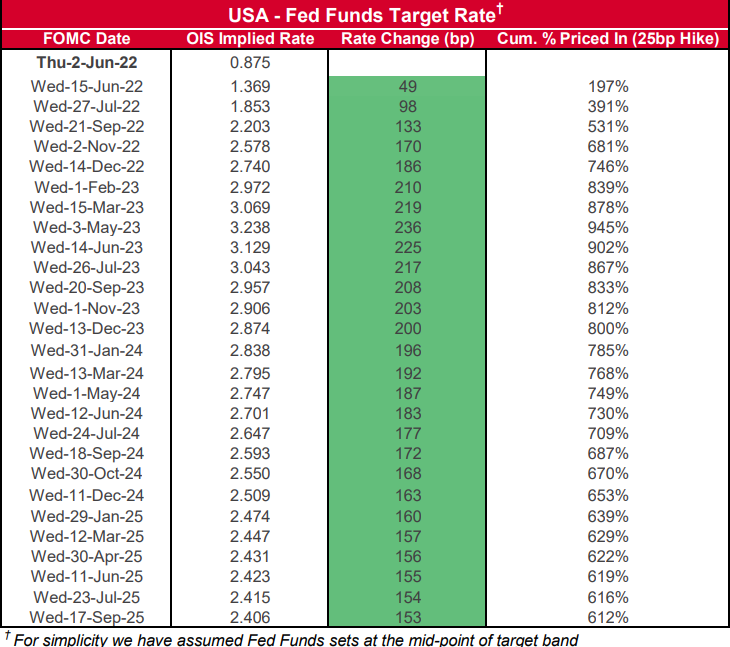

Above: Expectations for the midpoint of the 25 basis point wide Fed Funds rate range as implied by overnight index swap market. Click image for closer inspection.

“We’re certainly going to do what’s necessary to bring inflation back down. We are starting from a position of strength. The economy has a lot of momentum. The other factor that I think is very positive is that business balance sheets, household balance sheets, start this process from a very healthy position,” Vice Chair of the Federal Reserve Board Lael Brainard said on Thursday.

“On inflation I am going to be looking to see a consistent string of decelerating monthly prints on core inflation before I am going to feel more confident that we’re getting to the kind of inflation trajectory that is going to get us back to our two percent goal. In terms of our tools, they are very effective at cooling aggregate demand,” she said in an interview with CNBC News.

Previously, Federal Reserve Bank of St Louis President James Bullard had said on Wednesday that inflation in the U.S. is comparable to levels seen in the 1970s and warned that U.S. inflation expectations could become unmoored without credible Fed action.

James Bullard’s concern is that without this the Fed would risk inviting a new regime of high inflation and volatile economic outcomes.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of late March and April recoveries highlighting various areas of technical resistance for Sterling. Click image for more detailed inspection.

Above: Pound to Dollar rate shown at daily intervals with Fibonacci retracements of late March and April recoveries highlighting various areas of technical resistance for Sterling. Click image for more detailed inspection.

Bullar reminded that the Fed has raised the policy rate, has promised to raise the policy rate further in the future, and has begun the process of shrinking a balance sheet that swelled to around $9 trillion during the pandemic period.

The risk is that Friday’s data merely encourages Bullard and other members of the Federal Open Market Committee to push U.S. interest rates to the top end - or even above the oft referenced ‘neutral rate’ before the year is out.

The neutral rate is estimated to be somewhere between 2% and 3% so meeting it would imply an uplift in market pricing and gains for the U.S. Dollar.

“This situation is risking the Fed’s credibility with respect to its inflation target and associated mandate to provide stable prices in the U.S.,” he said.

“Forward guidance on these dimensions is helping the Fed move policy more quickly to the degree necessary to keep inflation under control,” he added.

Above: U.S. Dollar Index shown at daily intervals with Fibonacci retracements of June 2021 Federal Reserve induced recovery indicating various areas of technical support. Click image for more detailed inspection.

Above: U.S. Dollar Index shown at daily intervals with Fibonacci retracements of June 2021 Federal Reserve induced recovery indicating various areas of technical support. Click image for more detailed inspection.

Bullard also said that “real-time indicators of U.S. GDP growth suggest continued expansion in the quarters ahead.”

All of this came after Fed Board Governor Christopher Waller said in a virtual presentation to the Institute for Monetary and Financial Stability (IMFS) at Goethe University in Frankfurt, Germany, implied that he too could favour what would be a similar stance to that of James Bullard.

“I support tightening policy by another 50 basis points for several meetings. In particular, I am not taking 50 basis-point hikes off the table until I see inflation coming down closer to our 2 percent target. And, by the end of this year, I support having the policy rate at a level above neutral so that it is reducing demand for products and labor, bringing it more in line with supply and thus helping rein in inflation,” he said in one part.

“This is my projection today, given where we stand and how I expect the economy to evolve. Of course, my future decisions will depend on incoming data. In the next couple of weeks, for example, the May employment and CPI reports will be released. Those are two key pieces of data I will be watching to get information about the continuing strength of the labor market and about the momentum in price increases,” he added.