Above: File image of Fed Chair Powell. Image © Federal Reserve.

- GBP/USD reference rates at publication:

Spot: 1.3624 - High street bank rates (indicative band): 1.3247-1.3343

- Payment specialist rates (indicative band): 1.3500-1.3556

- Find out about specialist rates, here

- Or, set up an exchange rate alert, here

The Pound to Dollar exchange rate (GBP/USD) is entering a pivotal 48 hour period that is bookended by the Federal Reserve policy decision on Wednesday and Thursday's Bank of England policy meeting.

The Fed is expected to announce the reduction of its quantitative easing programme - a process called tapering - while the Bank of England could raise interest rates.

"Cable steadies above 1.36 handle as traders brace for Fed and BoE in the next 48 hours," says Kenneth Broux, a strategist with Société Générale. "Support 1.3570, resistance 1.3700."

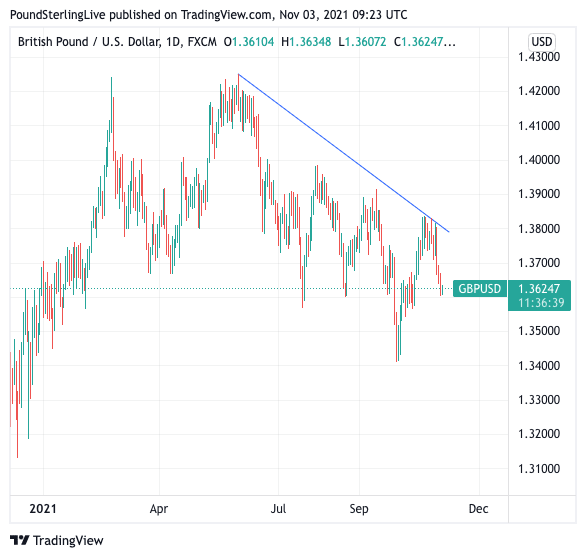

GBP/USD has been falling back from its October highs at 1.3835 over recent days to 1.3623 in anticipation of the two decisions: the declines suggest the market is expecting a more 'dovish-than-excpected' Bank of England and a more 'hawkish-than-expected' Federal Reserve.

Above: GBP/USD daily chart.

In his last comments before the Fed started its pre-meeting purdah period, Fed Chair Powell said that now was the time to start tapering asset purchases and so a formal announcement today seems inevitable.

The Fed looks set announce a reduction in $120BN / month bond-buying programme, ahead of a full completion in 2022.

Rhys Herbert, an economist at Lloyds Bank, says until recently it was generally assumed that the Fed would announce an initial reduction of $15BN to its $120BN monthly programme, with similar sized reductions in the subsequent months, that would end the process around mid-2022.

Markets are priced for at least two policy rate hikes to follow soon after in 2022.

But what is now less certain "is the path of tapering," says Herbert. "More recently some Fed policymakers have said that they favour a faster rate of reduction.

Such calls come on the back of spiking inflation, the majority of which is being fuelled by supply chain bottlenecks and surging energy prices.

However, evidence that inflation is being generated by labour shortages and wage prices would be of greater concern to Fed policy makers as such containing such price pressures falls under their remit.

"Anything north of $15 billion would be deemed hawkish, especially if it is around the upper end of the range of analyst expectation i.e. circa $30 billion. A larger reduction in QE would probably lead to further hawkish market bets as it would bring forward expectations for the start of rate rises," says Victor Argonov, senior analyst at EXANTE.

Broux says a ‘hawkish taper’ message could be linked to wages after pay in the U.S. rose by the most on record in third quarter in quarter-on-quarter terms, and by 4.2% year-on-year.

"The dollar will be off to the races if Chair Powell does not try to mollify market expectations for lift-off shortly after QE has ended next year," says Broux.

The Dollar would rally under such a hawkish outcome, with the Pound-Dollar rate eyeing a move towards 1.35 again ahead of the 2021 low at 1.3412.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

Herbert says if the Fed does opt for a quicker pace of tapering, or even indicate that the pace may pick up later, this will be seen as a more-hawkish signal that it is potentially readying itself for an earlier than previously indicated rise in interest rates.

However the Fed is unlikely to provide much explicit new guidance on interest rates, which could limit Dollar gains.

Indeed, Powell said recently he was not yet ready to start discussing rate increases.

"That suggests that while today’s policy statement and Powell’s press conference will stress remaining vigilant regarding the rise in inflation and the need to act if necessary, the Fed will not go further at this point," says Herbert.

He says Powell is likely to repeat the often used line that the bulk of the current rise in inflation is "transitory" and that the 'bar' in terms of the evidence they want to see to justify a rate hike is much higher than it was for tapering asset purchases.

To what extent markets believe Powell will prove a test of Fed credibility.

Central banks the world over continue to take a cautious approach to raising interest rates in the future, arguing inflation will come down eventually.

The reason for such guidance is that central banks don't want to raise the cost of financing in their respective economies sooner than absolutely necessary, recognising this would pose headwinds to economic growth.

An example of such guidance comes from the Reserve Bank of Australia which is adamant it won't raise rates until at least 2023/2024, but the market is pricing in as much as 75 basis points of hikes in 2022 alone.

A similar disconnect applies to the Fed as up to two rate hikes are priced into Fed-linked money markets, suggesting investors are not yet willing to suck up any guidance that rate hikes will not immediately follow the cessation of quantitative easing in 2022.

"It is likely we may see an initial spike in the dollar — and yields — if the FOMC confirms market expectations by tapering its asset purchases programme by $15 billion," says Argonov.

"Whether that potential spike would then turn into a full-on rally, or gets immediately sold, would depend on the Fed’s wider views on inflation and the economy, and in turn, on interest rates outlook," he adds.