- Chinese ports shuttered by Covid outbreak

- Pressure on global shipping costs rise

- Higher-for-longer inflation likely

- USD benefits in this environment

Above: Port terminal, Shanghai, China. Image © Adobe Stock.

- GBP/USD reference rates at publication:

- Spot: 1.3812

- Bank transfers (indicative guide): 1.3430-1.3520

- Money transfer specialist rates (indicative): 1.3688-1.3715

- More information on securing specialist rates, here

- Set up an exchange rate alert, here

The global supply chain squeeze is by no means over, and if anything, could be about to get worse as the Delta variant enters China.

For currencies, this could only mean further Dollar strength according to a number of investment bank analysts we follow.

News out of China is that its largest two container ports of Shanghai and Ningbo Zhoushan are facing severe bottlenecks, which should serve as a warning to investors that the pandemic has not yet completed its disruption of the global supply chain.

Ningbo's Meidong container terminal has closed due to the detection of Covid, the port handles containers for the China-Europe, China-Middle East route as well as the OCEAN Alliance lines.

"The closed terminal accounts for ~25% of container cargo through the port that is further to tighten already strained international supply chain," says John Meyer, Head of Research at SP Angel.

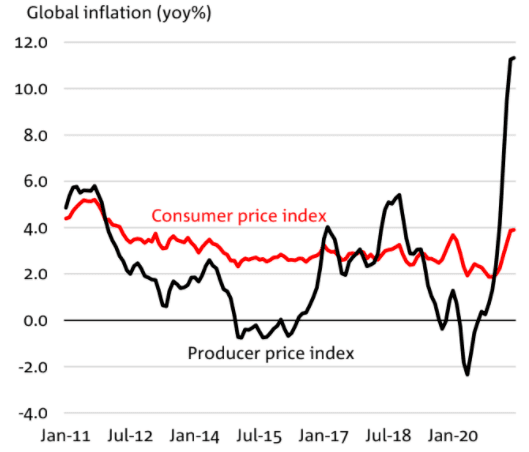

Signs that supply-side pressures are building once more suggests the run of high inflation readings in the U.S. - and indeed globally - could persist for longer than had been initially expected as supply and demand mismatches extend.

Above: Global inflation is elevated, image courtesy of NAB.

If supply-driven inflation persists for longer than expected those assets that have appreciated over recent months as part of an 'hot inflation trade' will potentially find ongoing support; the Dollar is the G10 FX's space's prime candidate.

The latest port lockdown was apparently put in place due to a single port worker who tested positive for the virus, the harsh reaction should serve as a warning that further disruptions are likely given the determined spread of the Delta variant through Asia.

The closure has resulted in 40 container vessels waiting to dock at Zhoushan, the outer anchorage of Ningbo.

"Many vessels are being re-routed to Shanghai where 30 container vessels are currently queuing. All this comes in the wake of Typhoon In-Fa which reduced container handling in late July," says Humphrey Percy at SGM Foreign Exchange Ltd.

Percy notes that in Southern China Covid containment measures in ports near Shenzhen led to similar numbers of container vessels being held up.

"So what does it mean for shipping rates? Inevitably costs are rising further with rates for a 40 foot container reaching $20,000 on the China to USA route exacerbated further by increasing retail orders ahead of the H2 shopping season putting strain on global supply chains. So in a nutshell it will take longer and cost more for the West to source goods manufactured in China," says Percy.

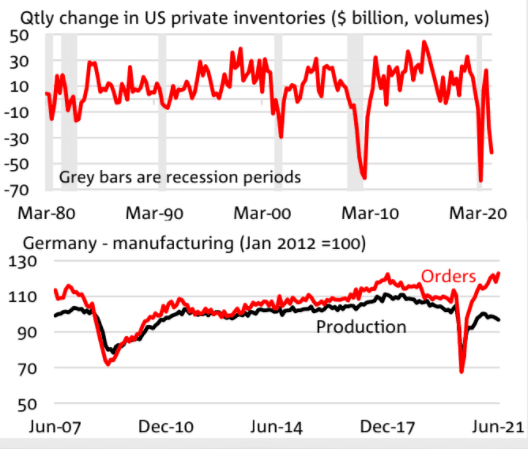

Above: Global supply chain mismatches contributes to a mismatch in supply and demand, image courtesy of NAB.

"Producers continue to suffer severe supply chain issues caused by shortages of commodities, key inputs (e.g. semiconductors) as well as labour, while dislocations and delays at ports have apparently worsened in recent weeks," says Holger Schmieding, Chief Economist at Berenberg Bank.

Supply shortages may take until early 2022 to fully resolve due to complex production structures, according to Berenberg.

Meyer says the suspension is expected to add further stress to supply chains already struggling with peak U.S. consumer season between August and November.

"The delta surge in Asia could exacerbate the overall supply disruptions leading to other upside inflation risks," says Mikael Sarwe, Head of Strategy, Sweden at Nordea Markets.

An outbreak of a similar scale in May at Shenzen’s Yantian port triggered a month-long lockdown and Meyer says it was a major contributor to North Asia-to-West Coast North America spot rates to hitting an all-time high.

Shipping company Hapag-Lloyd told their clients that they "expect a delay in planned sailings that might affect…cargo planning" as a result of the latest squeeze.

And shipping ports globally are still facing major congestion, with 30 ships anchored in the San Pedro Bay outside the Los Angeles/Long beach port complex yesterday.

"The pandemic has disrupted global supply in product and labour markets. This is a shock. The global economy benefitted from plentiful supply of both for the last two decades and now things are disrupted. Inflation is resulting from the disruption," says Chris Iggo, CIO Core Investments, AXA Investment Managers.

Research from Accenture finds 94% of Fortune 1000 companies are seeing supply chain disruptions from COVID-19, 75% of companies have had negative or strongly negative impacts on their businesses and 55% of companies plan to downgrade their growth outlooks (or have already done so.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

"We fear that inflation is still with us and will be for some time," says John Velis, FX and Macro Strategist for the Americas at BNY Mellon.

U.S. inflation is currently burning hot (i.e. well above the Federal Reserve's 2.0% target) on a combination of global supply issues and a strong economic rebound.

Data out this week meanwhile suggest inflationary pressures are becoming broader, i.e. starting to show up in a wider selection of goods and services in the inflation basket.

"Our forecast is that core CPI will remain close to or probably over 4% y/y until Q2 2022. When it then starts to drop towards 2%, the labour market will be tight and wage increases high, meaning that the Fed’s medium-term inflation forecasts should remain above 2%. Or paraphrasing Powell – an inflation backdrop the Fed would like to see and thereby act on with rate hikes from late 2022," says Nordea's Sarwe.

In an environment of heightened inflation expectations - which has broadly been a dominant theme for markets in 2021 - it serves to identify the currency market winners.

On this count the Dollar stands out and is therefore liable to be one of the outperformers going forward if the higher-for-longer inflation theme continues to play out in the U.S., forcing the Federal Reserve to bring forward the timing of their first intended interest rate rise.

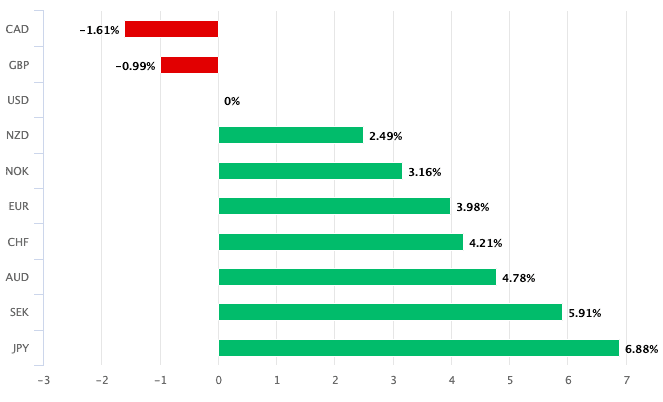

"The USD remains the best performing G10 currency and we expect the outperformance to continue as the FX markets continue to position for the approaching start of Fed policy normalisation," says Valentin Marinov, Head of FX Strategy at Crédit Agricole.

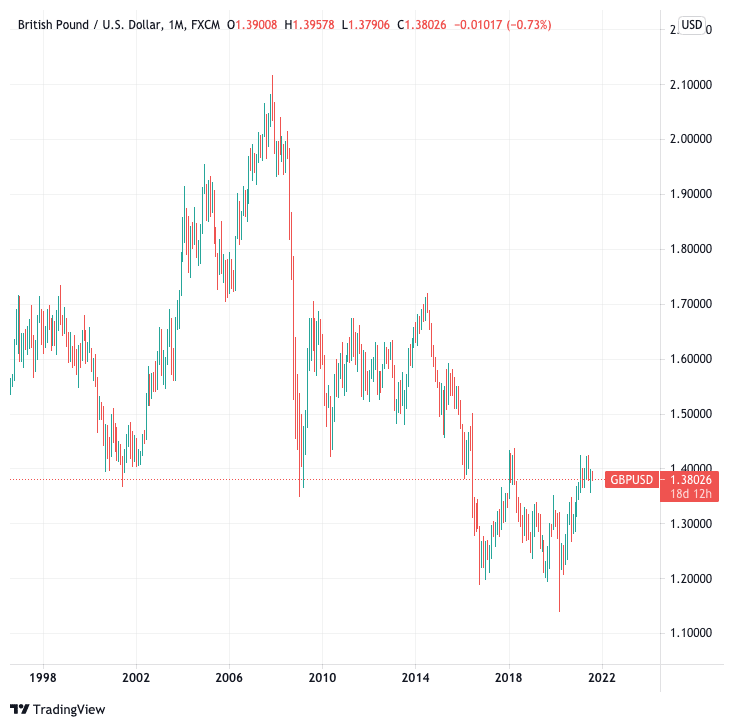

Above: On current trends the Dollar will soon turn positive against the Pound for 2021.

Nordea Markets are also backing further Dollar strength:

"EUR/USD knocked on the 1.17 door, but pulled back from it as US CPI failed to surprise to the upside. RELATIVE tapering timing, real rates and growth/inflation continue to favour the USD over the EUR, so we stay short EUR/USD," says Sarwe.

Meanwhile, a note from the foreign exchange trading front-line at JP Morgan's London trading desk:

"I think the Fed narrative shift over the last week will continue to linger in the market’s mind into the minutes next week so hard to see the dollar selling off too much until then."

For the Pound-to-Dollar exchange rate the developments come at a time of downside pressures that means the pair has lost value during August and remains anchored near the bottom of a long-term multi-year range.

Kenneth Broux, a strategist with Société Générale, says the in the near-term Pound-Dollar is on course for its biggest drop in four weeks as markets ignore solid GDP and higher stocks.

Support is identified by Broux at 1.3779 (the 200 day moving average), resistance issue seen at 1.3890.

The fundamental backdrop meanwhile suggests limited scope for a concerted push higher.