- USD sees widespread gains in possible deat cat bounce.

- After USD fall risks prompting U.S.-EU, Fed-ECB fallout.

- BoE inadvertently mediates peaceful solution Thursday?

- As UK story permits less 'dovish' stance & GBP repricing.

- GBP can ease EUR TWI, enable further orderly USD fall.

Image © Adobe Images

- GBP/USD spot rate at time of writing: 1.3656

- Bank transfer rate (indicative guide): 1.3278-1.3374

- FX specialist providers (indicative guide): 1.3451-1.3560

- More information on FX specialist rates here

The Dollar Index built further on its 2021 gain this Wednesday amid what could soon be cast as a 'dead cat bounce' for the broad barometer of the U.S. currency, following a 2020 decline that has stoked tensions among central banks and risks making a battlefield out of foreign exchange markets in some parts.

Dollars were bought widely in what was said by some analysts to be profit-taking by investors on earlier wagers against the greenback and in favour of Europe's single currency, which has a more-than 57% weighting in the ICE Dollar Index and a 32.6% share of the Bloomberg Dollar Spot Index.

Losses for Europe's single currency, which was the biggest faller against the greenback on Wednesday, are often enough on their own to lift the various indices that attempt to measure the broad Dollar although the U.S. unit was higher against many of its major counterparts on an intraday basis and had gained on all barring one for 2021.

"One of our major concerns with respect to our reflation themes for 2021 has been their broad consensus in the market," says David Sneddon, head of technical analysis at Credit Suisse. "Some of these now need to be “stress tested” before core trends can resume. We feel this is especially true for USD."

Above: ICE Dollar Index shown at 4-hour intervals alongside Euro-Dollar rate (orange).

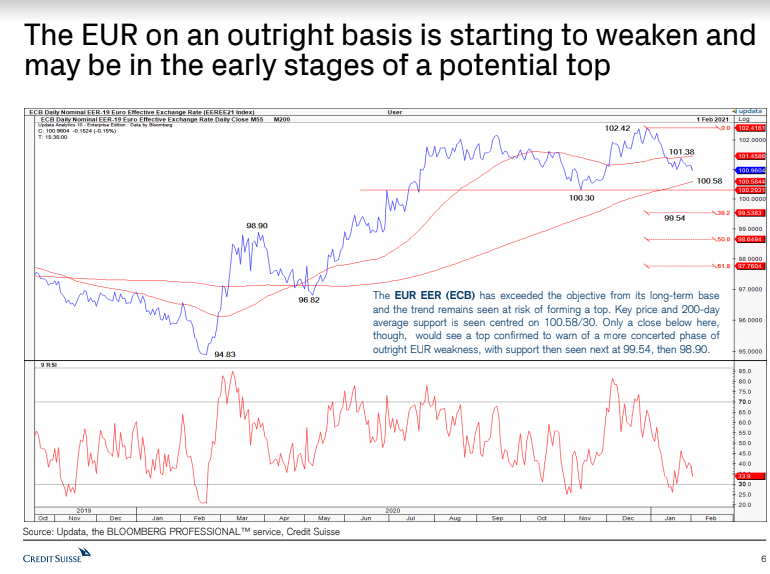

"EURUSD is probably the currency most at risk of a deeper pullback in our view, as not only has it achieved its “measured base objective” at 1.2355; however, we are also seeing signs the EUR is weakening in its own right. With a small top already in place we look for further weakness to 1.1945/14, potentially even as far as 1.18/1.17," Sneddon writes in a recent research presentation.

The 2021 rebound leaves the ICE Dollar Index carrying a -6.7% decline for the year to February 03 but has drawn increasing attention of late for its defiance of a market consensus which argues that a further protracted decline still lurks on the path ahead. Commodity and emerging market currencies are expected to benefit most from the rout, although almost all Dollar bearish outlooks come with forecasts for further gains in the Euro-Dollar rate this year, albeit that increases are anticipated to varying degrees.

"In January, the USD reclaimed lost territory in response to severe lockdown measures in Europe, disappointing economic growth data globally, slow progress in vaccinations, rumors about the Federal Reserve tapering asset purchases and speculations about a large fiscal stimulus package in the US," says Thomas Flury, head of FX strategies at UBS Global Wealth Management. "We keep our EURUSD forecasts at 1.25 for June, and at 1.27 for September and December; and we add a March 2022 forecast, also at 1.27. We expect the pairing to hover in a 1.20–1.25 range over the next couple of months, eventually moving toward 1.25–1.30 later in the year."

Source: Credit Suisse. Technical analysis of Euro's equilibrium exchange rate. Click image for closer inspection.

2021's Dollar rebound aughurs memories of consensus views from years gone past, which mostly fell flat in the face of outperformance from the U.S. economy and underperformances in parts of continental Europe that all too often sabotaged the Euro currency's attempts at turning the tables on the greenback.

This is after the 2017 rally was curtailed by strong U.S. growth and interest rate rises from the Federal Reserve (Fed), which came against a backdrop of slowing growth, falling inflation and renewed quantitative easing from a European Central Bank (ECB) whose concerns about recent increases in EUR/USD have become palpable in January, and may be key to the outlook for not only the Euro but also the anticipated widespread U.S. Dollar downturn.

"We have sympathy for this [“US exceptionalism”] view, but we also have our reservations. Our outlook for the USD is that it will weaken but that this is a cyclical move rather than a structural one, limiting the scale and longevity of the sell-off. We expect relative economic growth to become a greater part of the narrative as the grip of risk appetite on FX fades through the year," says Daragh Maher, America's head of FX strategy at HSBC, noting a recent turn in the Transatlantic growth outlook that purports to favour North American currencies. "We think it unwise and premature to extrapolate the last two days’ price action where the USD and equities have moved in tandem."

Above: Euro-to-Dollar rate shown at daily intervals with GBP/USD (orange) and S&P 500 Index futures (blue).

Europe's single currency has been weakening against many major rivals, and the U.S. Dollar strengthening, ever since ECB President Christine Lagarde and fellow European rate setters appeared to make a more concerted effort in January to reign in EUR/USD. Since January 13 when Lagarde told a Reuters Online audience that she and the bank are "extremely attentive" to the exchange rate, the trade-weighted Euro has fallen due to a combination of declines in EUR/USD and EUR/CNH as well as gains in GBP/EUR.

This is important context for the foreign exchange market because it indicates that ECB fears for the deliverability of its ever-elusive inflation target are imposing constraints on and to some extent dictating price action in more than just the EUR/USD rate. What matters most for the Dollar Index and EUR/USD direction in the short-term is the answer to whether or not a further downward adjustment in either or both of EUR/GBP and EUR/CNH is likely.

"On the back of USD weakness, a whiff of currency wars has been noticeable in the markets for some months. The ECB is the latest central bank to push back against the soft USD," says Jane Foley, a senior FX strategist at Rabobank. "While we see scope for EUR/USD to pullback towards the 1.20 area this quarter as investors reassess the change in fundamentals, we expect to see 1.22/1.23 again later on in the year."

Above: EUR/USD (blue line) with EUR/CNH (orange) and Pound-Euro rate (red & green) at 4-hour intervals.

Without such adjustments, a EUR/USD recovery (and the consensus U.S. Dollar decline) would simply eat into whatever is left of the already-insufficient inflation pressures, at a point when ECB policymakers have just emerged from what is a lost decade for Europe as far as the bank's inflation target is concerned and are again growing fearful for the European inflation outlook.

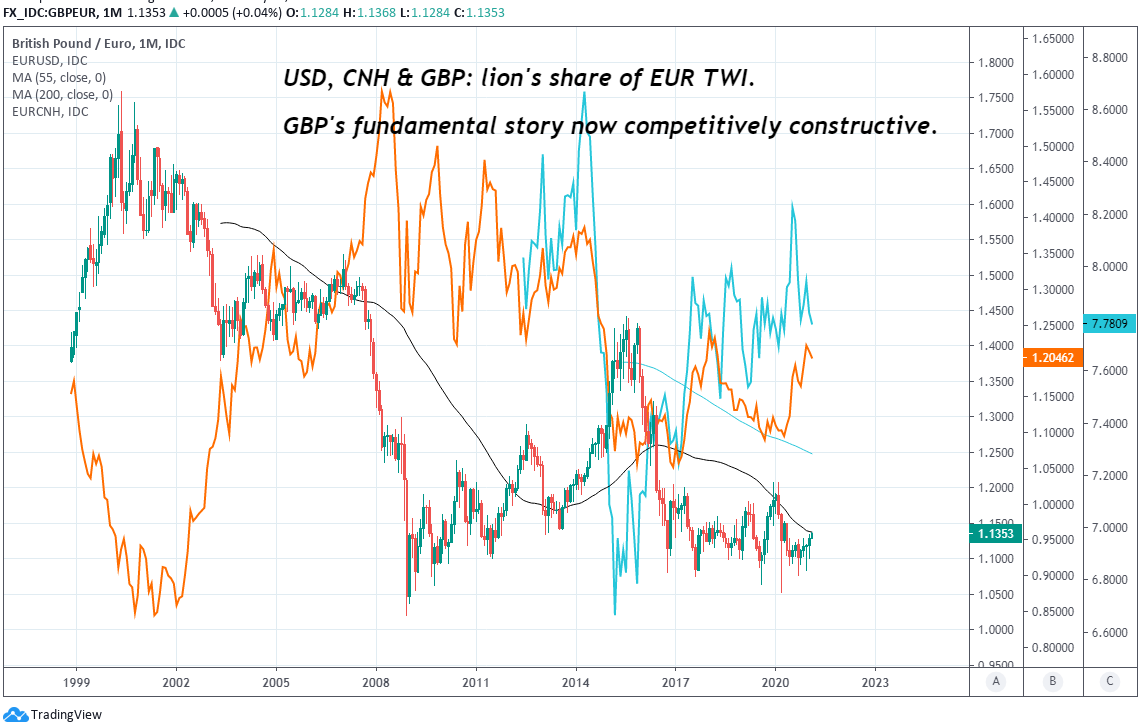

Irrespective of whichever precise measure or other version of such a barometer is used, trade-weighted Euros are substantially composed of the Dollar, Chinese Yuan and Pound Sterling. This means that marked increases in EUR/GBP, EUR/CNH and EUR/USD can impact the prices of import and export goods with the effect of making imported goods become cheaper and exacerbating the downward pressure on European inflation, much to the chagrin of the ECB.

"Last year the EUR recovery was partly driven by rising EU exports to China - so it doesn’t help that China looks to be entering a period of slower economic activity," says Jordan Rochester, a strategist at Nomura. "European inflation spiking higher and ECB communications on the strength of the currency add uncertainty for front-end rates and also the longevity of PEPP beyond this year, both of which would be growth and EUR negative."

Above: GBP/USD can lift GBP/EUR (blue), reducing the trade-weighted Euro & EUR/USD's (orange) compulsion to fall.

This is where the Bank of England (BoE) and Thursday's policy decision enter into the broader picture, if EUR/USD is to remain supported at the psychologically important 1.20 level over the coming days, weeks and months. In part because the only mechanically viable pathway through which EUR/GBP and EUR/CNH can decline is via a higher GBP/USD and even lower USD/CNH. EUR/GBP always closely reflects relative price action in EUR/USD and GBP/USD, likewise with USD/CNH and EUR/CNH.

"We continue to believe the GBP will be one of the G10 currencies most heavily shaped by economic data during the first-half of the year. It's also important to stress that EURGBP is currently trading at its average of the last 4.5 years since the Brexit referendum (0.88). The extent and speed at which investors build their GBP exposures from here will depend on the aforementioned factors, risk appetite levels, and how the Eurozone shapes up," says Stephen Gallo, European head of FX strategy at BMO Capital Markets. "We'd expect minor intraday moves in the GBP based on the MPC's word choices."

The Pound-Dollar rate and Sterling more broadly have taken the consensus by surprise this year, just like the Dollar and thanks in no small part to a vaccine rollout that has so-far been faster than in other major economies including the U.S. and Europe. This offers the UK a shot at outperforming neighbours in any recovery ahead and provides at least some semblance of assurance to the BoE about the comparative outlook for the UK. This could lead the bank to take a more optimistic, or simply less pessimistic, policy view on Thursday and adopt a more Sterling-friendly stance.

Above: Pound-to-Dollar rate shown at weekly intervals alongside ICE Dollar Index.

Furthermore, and with Sterling exchange rates still only around the midpoint of post-referendum ranges rather than being at extremes like in Europe, the BoE arguably has less reason than others to want to stand in the way of a currency appreciation. Not least of all because it's not lost sight of its inflation target in the same way policymakers in Europe and elsewhere have.

To the extent that the BoE's words and actions are able to lift the GBP/USD rate on Thursday, the Euro-to-Dollar rate may have a greater chance of finding support around 1.20 and as a result, the nascent rebound in the U.S. Dollar Index could yet come to be described as little more than a 'dead cat bounce' that soon fades. However, and in the absence of a further lift in GBP/USD, the writing is already on the wall for the Euro and consensus U.S. Dollar view.

"In as much as we don't expect significant volatility in the GBP tomorrow, we would expect the Bank's relatively upbeat views on the FY outlook to mostly offset the impact of any near-term caution (particularly with the ceiling on top of EURGBP starting to look more formidable). We're less enthused about adding to GBPUSD longs above 1.36 for the time being, but we think there is scope for weakness to be fairly limited in view of vaccine optimism," BMO's Gallo says.

Above: Pound-to-Euro rate shown at monthly intervals with EUR/USD (orange) & EUR/China rate (blue).