- GBP/USD set for tentative recovery as Brexit trade talks extended again.

- But path ahead could be bumpy as phoney war plays out in December.

- Ratchet-clause row suggests deal in bag, but GBP recovery to be slow.

- 'No deal' downside could see GBP at 1.15, as deal offers view of 1.37.

Image © Pound Sterling Live

- GBP/USD spot rate at time of writing: 1.3226

- Bank transfer rate (indicative guide): 1.2863-1.2956

- FX specialist providers (indicative guide): 1.3028-1.3133

- More information on FX specialist rates here

The Pound-to-Dollar rate faces a testing period of heightened volatility and political theatre as a likely-phoney war plays out in the Brexit trade negotiations, although the latest manoeuvres from the two sides could offer Sterling an attempt at stabilisation on Monday.

Pound Sterling could be in for a tepid and cautious recovery to open the new week after Prime Minister Boris Johnson and European Commission chief Ursula Von Der Leyen announced on Sunday that Brexit trade negotiations would continue beyond the latest "final deadline".

However, the risk of renewed losses remains, more so after Johnson continued to warn on Sunday that "we remain very far apart on these key issues...get ready, with confidence, for January 1 - trade on WTO terms if we have to."

The two sides had previously agreed to call off talks on Sunday if an agreement wasn't reached by then.

"It's impossible to know whether the UK/EU decision to blast through another Brexit “deadline” today means a deal has become more likely or whether both sides believe that a no deal is the end destination but just want to show that they are doing all they can to avoid it. No new “deadline” has been set, so there could be some political and economic fireworks one way or another on New Year’s Eve," says Paul Dales, chief UK economist at Capital Economics, who says the Pound-Dollar rate could fall from 1.32 on Sunday to around 1.15 if the two sides default to a relationship governed by World Trade Organization terms.

Sterling was resoundingly the worst performing major currency last week, suffering a loss of -1.5% against the Dollar, after Prime Minister Johnson said a 'no deal' Brexit is now the most likely outcome from talks with the EU.

The Pound-to-Dollar rate fell from above 1.34 at last Sunday's open to a low of 1.3133 on Friday before paring losses into the weekend.

"We will look for a fresh attempt to find a floor," says David Sneddon, head of technical analysis at Credit Suisse, who's flagged 1.3129 and 1.3106 as technical supports for the Pound. "Resistance moves to 1.3373 initially, then 1.3478. A weekly close above 1.3514 remains needed to see a major base secured to mark an important change of trend higher. We would then see resistance at 1.3620 initially – the 38.2% retracement of the entire 2014/2020 decline - where we would expect an initial pause."

Above: Pound-to-Dollar rate shown at hourly intervals.

Sterling had traded back to December 2019's post-election highs previously, reflecting what was effectively a wager by investors that a trade deal had been all but ratified. The rally had been encouraged by reports suggesting that progress was steadily being made, with only differences over fisheries access singled out in on-the-record remarks made by negotiators and Prime Minister Johnson. But a row over a newly introduced so-called ratchet clause cast a shadow over the market's sunlit uplands last week.

"While a very close call, we continue to think the UK-EU trade deal is more likely than not. We can easily see the negotiations dragging beyond this Sunday (which would be in line with the recent trend of breaking yet another deadline) but the deal should eventually be reached, with a possible compromise on the level playing field and agreeing on the so-called ratchet clause (where both sides mutually agree to raise standards)," says Petr Krpata, chief EMEA strategist for currencies and interest rates at ING. "This should provide an upside to GBP/USD and push the cross above the 1.35 level, towards 1.37."

{wbamp-hide start}{wbamp-hide end}{wbamp-show start}{wbamp-show end}

The ratchet clause could be a red herring rather than a serious negotiating pursuit of the EU as a dynamic UK alignment with EU rules as they evolve has never been Europe's stated objective. Brussels set out, using the EU withdrawal agreement and accompanying political declaration, only to have the UK retain its existing rulebook as it stands at the end of the transition period but was resisted by Boris Johnson this year after the trade talks began.

The new demand could simply be an act of benevolence toward a Prime Minister who's already conceded defeat over whether existing EU standards should remain in force after the transition ends. Under these circumstances Johnson, who agreed in his political declaration to keep the EU's rules on various matters before attempting to abandon the commitment, would need to contrive some kind of a win in order to sell his new agreement at home.

Johnson may calculate that a soon-to-be announced European climbdown over a recently-introduced and surplus demand will help him to do that. Credit Suisse warned of exactly this kind of scenario at the beginning of December.

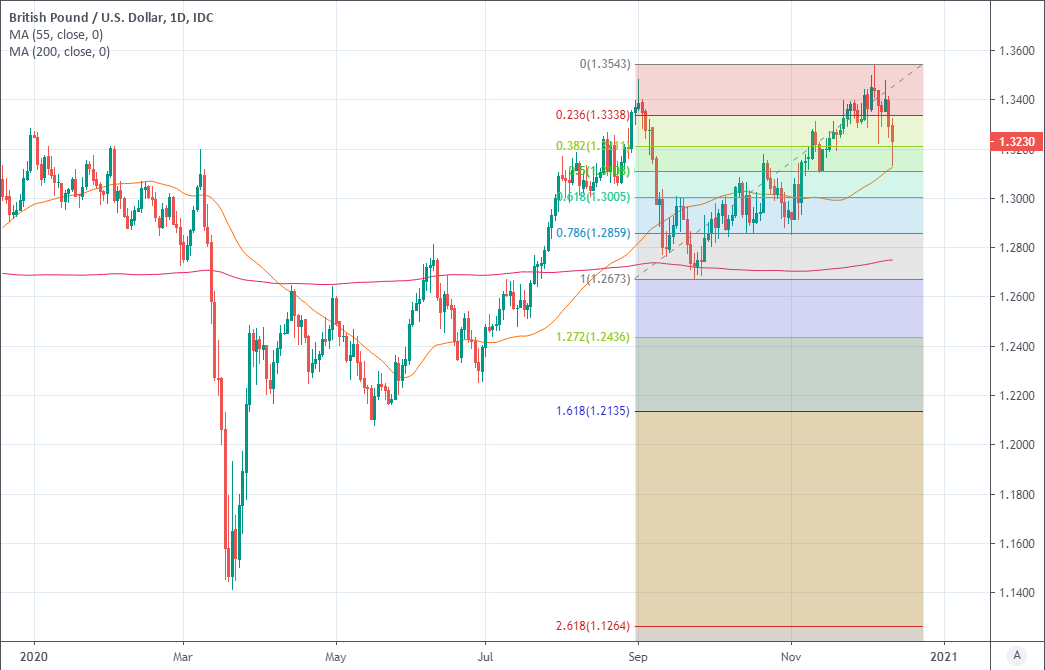

Above: GBP/USD with 55 & 200-day averages as well as Fibonacci retracements of September rally indicating support.

This would imply that Sterling exchange rates are to become for the duration of December the site of a phoney diplomatic war in which contrived fluctuations in the perceived odds of a 'no deal' Brexit preside over volatile price action until an agreement is eventually announced.

"BoJo and Von Der Leeyen suddenly sound like ”no-dealers” in the media, which is probably the best possible signal you can get that neither has any intention of actually allowing a cliff-edge scenario to unfold from 1st of January. Is it not classic public relation tactics to tell the public that there is a clear risk that everything will fall apart unless a prolongation is agreed upon?" asks Martin Enlund, chief FX strategist at Nordea Markets. "For those who hope for a big trade deal, a prolongation may be the worst-case scenario since there are no incentives for any of the parties to break the stalemate unless an external trigger-move is introduced to the game. A cliff-edge no deal would be exactly such a scenario. A prolongation will just lead to more of the same."

Policy decisions by the Federal Reserve and Bank of England will also get some airtime this week may offer Sterling some additional support, especially if the Fed surprises the market by doing more than simply adapting its forward guidance about interest rates and quantitative easing (QE). However, last week's Food & Drug Administration approval of the Pfizer and BioNTech coronavirus vaccine for emergency use may mean this is less likely now.

Likewise with the Bank of England, which is presiding over the economy and currency of a country that was first to deliver the vaccine in the field last week. The Fed decision is expected at 19:00 London time on Wednesday while the BoE will update on its policy outlook at 12:00 Thursday.

"The EU has reached agreement on its budget and recovery fund, but a Brexit deal is still outstanding, and the US Congress has not yet agreed on a fiscal package," says Fabrice Montagné, an economist at Barclays. "The start of the vaccination campaign this month may support confidence, but more realistically only when the outbreak effectively slows (especially in terms of hospital admissions) and restrictions are lifted. For now, we continue to expect Q4 20 GDP to print -1.5% q/q. We continue to monitor the progress of the Oxford/Astrazeneca vaccine candidate given the UK’s relative reliance on this producer. This week, a peer-review of the analysis of the phase 3 programme confirmed that the vaccine is safe and effective. The data is currently with the UK regulator for approval, with little clarity on precisely when this will happen."

Above: GBP/USD with 55 & 200-week averages & Fibonacci retracements of post-referendum fall indicating resistances.