Image © Adobe Images

- USD rebounds from payrolls loss but choir of bearish voices grows.

- Analysts debating whether first Fed cut comes in June or September.

- But difference matters little for USD as calls for depreciation grow louder.

The Dollar was back on its front foot Monday after having risen against all G10 rivals during the morning session but analyst commentary on the currency in the wake of last Friday's nonfarm payrolls report suggests it might only be a matter of time before losses resume as market expectations for Federal Reserve interest rate cuts rise.

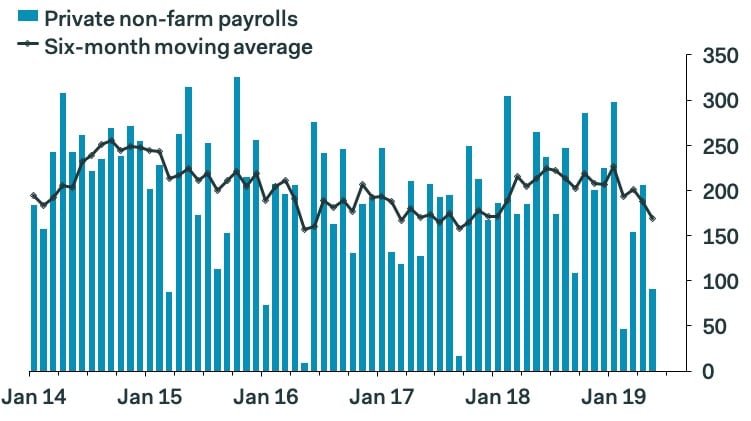

Expectations for Fed rate cuts and a weaker Dollar rose following May's nonfarm payrolls report, which revealed jobs growth that was far below the level anticipated by the market. What's more, and adding insult to injury, Bureau for Labor Statistics estimates of jobs growth in March and April were revised down by a combined 75k.

That helped push the 2019 average down to just 164k, well below the 223k average seen throughout the 2018 year. The data was seen validating market bets suggesting the Fed will cut its interest rate on multiple occasions before the year is out.

"The 75k gain in NFP in data for May released on Friday was far weaker than expected, especially incorporating the 75k downward revision to previous months," says Lee Hardman at MUFG. "All downturns start with a decelerating in the pace of job creation and hence another few months of employment slowdown would be persuasive evidence for the Fed to take action."

Above: Pantheon Macroeconomics graph showing monthly payrolls figures with six-month average.

Analysts are debating, and markets currently attempting to determine, whether the first interest rate cut will come in June or if the Fed will wait until September. However, Hardman says the bank has a history of moving slowly at the end of a business cycle to provide support to the economy so it may not give much of a clue about forthcoming policy action at next week's meeting and, ultimately, that it still might not cut rates for quite some time to come.

But the issue of whether the first interest rate cut comes this month or at the end of the second quarter matters little for the Dollar because the cat that matters is now well and truly out of the bag. Analysts have long been bearish in their views on the outlook for the Dollar but expectations of multiple Fed rate cuts are emboldening the choir of voices now calling for depreciation.

Markets care about the Fed story because changes in interest rates, as well as the outlook for them, can have a significant influence over international capital

flows as well as speculative short-term trading activity. Capital flows tend to move in the direction of the most advantageous or improving returns, with a threat of lower rates normally seeing investors driven out of and deterred away from a currency while rising rates have the opposite effect.

"It has been a poor start to the month for USD as the chorus of dovish Fed rhetoric continuous to build against the backdrop of deteriorating US macro data and mounting trade war tensions," says Kamal Sharma, a strategist at Bank of America. "A sustained pick-up in FX volatility combined with further US macro deterioration exposes the USD to sustained downside over the coming weeks."

Above: USD/JPY rate shown at weekly intervals.

Sharma and the Bank of America team are betting against the USD/NOK and USD/JPY exchange rates. They say the former will be sent lower not only by the deteriorating U.S. story, but also by resilient oil prices and a Norwegian central bank that is lifting its own interest rates. The USD/JPY rate is expected to decline in line with U.S. bond yields, stock markets and any increase in tensions between the U.S. and China.

The 2019 consensus had always been for the White House's 2018 tax cuts to wear off, leading to an automatic slowdown in the economy that already risked ending the 2015-present Federal Reserve rate hiking cycle, but surveys have recently pointed to a sharp loss of momentum in the manufacturing sector which have led some to fear that President Donald Trump's trade war with China is now beginning to hurt the domestic economy too.

President Donald Trump lifted from 10% to 25% the tariff levied on annual imports from China totalling some $200 bn in May, but there is another $300 bn of annual Chinese exports to the U.S. that is also set to be hit with a 25% tariff. The tariff fight then escalated further still when each side began deploying so-called blacklists against companies headquartered in the other's countries, which left the spat looking more like an all-out economic and geopolitical conflict than just a tariff fight.

"We turn bearish on USD. Recent USD weakness may accelerate as long positions become unwound, particularly against AUD and CAD," says Gek Teng Khoo, a strategist at Morgan Stanley. "Rest-of-World weakness is likely to cause investors to move forward market expectations of Fed cuts, weakening the USD and lowering front-end interest rate differentials. We suggest fading USD rallies. DXY has broken support at 97.50. A break below 96.95 suggests further tactical downside momentum."

Above: Dollar index shown at weekly intervals.

The spat with China is raising costs for U.S. companies and consumers while denting business confidence the world over. Until mid-May, investor risk aversion resulting from the war of attrition between the world's two largest economies had kept the Dollar supported but the increasing signs the conflict is taking its toll on the U.S. economy have changed all of that for the time being.

However, and even in spite of the Dollar's newfound weakness, it remains an open question whether the Pound Sterling will participate in any global riposte against the mighty greenback given a Brexit process that is increasingly fraught with risk and signs the UK economy is also weakening.

"The Irish border remains the stumbling block. May has already failed to solve this dilemma. And Johnson is unlikely to fare any better unless he turns out to find a solution to please all sides that nobody else thought of beforehand. Not very likely," Antje Praefcke, an analyst at Commerzbank. "Johnson will likely set the tone during the next days. And this means trouble ahead for sterling."

The UK has still not left the EU and with Prime Minister Theresa May resigning from post as leader of the governing Conservative Party, a contest is now underway to find the UK's next Prime Minister. But with this comes increasing risk of a general election, a 'no deal' Brexit and of remaining in the EU.

Only time can tell what will be the fate of the UK's relationship with the EU and which of the political parties will withdraw the UK from the bloc, if it even leaves at all, but analysts are increasingly conscious of the many pitfalls in the road ahead and are now warning of a bumpy ride to come.

"GBP/USD remains upside corrective very near term and last week reached the 23.6% retracement at 1.2753. It will need to regain this on a closing basis in order to alleviate immediate downside pressure and avert further losses to the 1.2444 December 2018 low," says Karen Jones, head of technical analysis at Commerzbank and colleague of Praefcke's.

Above: Pound-to-Dollar rate shown at weekly intervals.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement