Image © Adobe Images

This week's Kiwi growth data disappointed and serves as a reminder of NZD's domestic challenges.

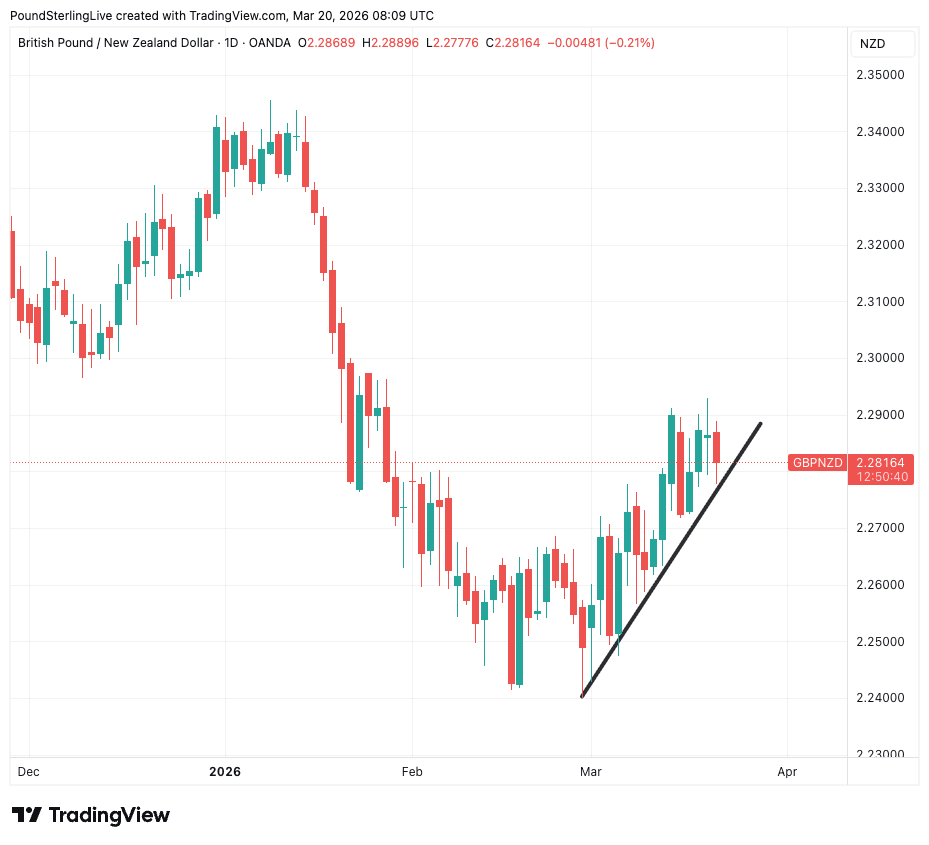

The pound-New Zealand dollar rate looks set to record a down week, but the overall trend still remains higher in the short term as the March recovery, aided by the war in the Middle East, lifts UK interest rate expectations more rapidly than elsewhere in the G10 space.

The Bank of England's Thursday policy decision showed concerns that the war will raise the UK's inflation profile, and markets now expect two rate hikes in the coming year, whereas just three weeks ago there was an expectation for two cuts.

That shift in expectations means the UK's interest rate differential with New Zealand has moved in favour of the GBP over the NZD in recent weeks.

The Kiwi started the year with a bounce in its step, but has been pressured by risk aversion stemming from Middle East tensions, with the currency sensitive to both global risk appetite and the oil price shock filtering through to domestic inflation expectations.

Domestically, the currency's outlook was dented by this week's news that the domestic economy expanded by just 0.2% in the final quarter of the year.

That means growth fell short of both analyst forecasts of 0.4% and the RBNZ's own projection of 0.5%.

GBP/NZD is recovering from the falls of January and February.

Annual GDP growth came in at 1.3%, below the 1.7% estimate. Of the past seven quarters, the economy has shrunk or registered no growth in four.

The most recent release dents hopes that the economy was finding some exit velocity from its slump, and that draws question marks over the Reserve Bank of New Zealand's ability to raise interest rates.

Homeowners and businesses will be pleased to hear that, but from a currency perspective, higher rates tend to provide support, and the implications are that the Kiwi might not have its central bank behind it.

Yet, the war in the Middle East means the RBNZ, like other global central banks, might have to hike anyway.

Markets have moved to price in a 25 basis point OCR rate hike in September 2026, with more than a 70% probability assigned to a further increase in December, a significant shift given the RBNZ's current hold at 2.25%.

GBP/NZD

This contrasts with the RBNZ's own published projections, which do not fully incorporate a year-end hike, reflecting the central bank's caution given the still-fragile domestic growth backdrop.

Westpac now expects inflation to remain near the top of the RBNZ's 1-3% target band for most of 2026, cooling to only 2.6% by year-end.

ANZ and BNZ are projecting inflation of around 2.8% by Q4 2026.

Although the RBNZ might raise rates, the fact that other central banks will also be doing so in response to the war means the NZD treads water in the coming weeks.