-RBI to hike rates further in 2018, helping to lift the Rupee.

-Domestic data and global factors may also support Rupee.

-But oil-driven increase in inflation is tax reforms cloud outlook.

© Hemant, Adobe Stock

The Reserve Bank of India (RBI) could be shifting its monetary policy in a way that is likely to provide support for the Rupee over the coming months.

Last Thursday the RBI raised its interest rate by 0.25% to 6.25%, helping to lift the Rupee. The move was prompted by a surprise increase in inflation during April, from 4.3% to 4.6%, which took consumer price growth further away from 4% midpoint of the RBI's target range.

Some analysts see this as the start of a 'tightening cycle', which is central bank parlance for a period of sustained interest rate increases geared at cobatting rising inflation by cooling the economy.

"We think today’s hike marks the start of a modest tightening cycle," adds Shilan Shah, a senior India economist at Capital Economics.

Shah has been saying for some time that the RBI will raise rates soon and, despite last week's hike, forecasts the central bank will raise its interest rate by a further 50 basis points (0.50%) to 6.75% over the next six months.

This is an above consensus call and is noteworthy because a solid majority 40 economists polled by Bloomberg had expected the RBI interest rate to remain at 6.25% until the end of 2019.

Any further rate rises, or hints of them being in the cards, would be likely to support the Rupee by attracting greater inflows of foreign capital, as rising returns are a powerful lure for investors.

Asian lender Maybank, meanwhile, forecasts the Indian Rupee to appreciate from its current spot rate of 67.45 vs the Dollar (USD/INR) to 66.00 by the end of the second quarter 2018, before eventually falling to 63.00 by March 2019.

"Even though RBI did not commit to a tightening cycle, global environment and domestic conditions could still be positive for the rupee," says Saktiandi Supaat, an analyst at Maybank.

India's economy grew at its fastest pace for nearly 2 years during the first quarter of 2018, with GDP rising at an annualised pace of 7.7%, which is part of the reason inflation has also risen so much.

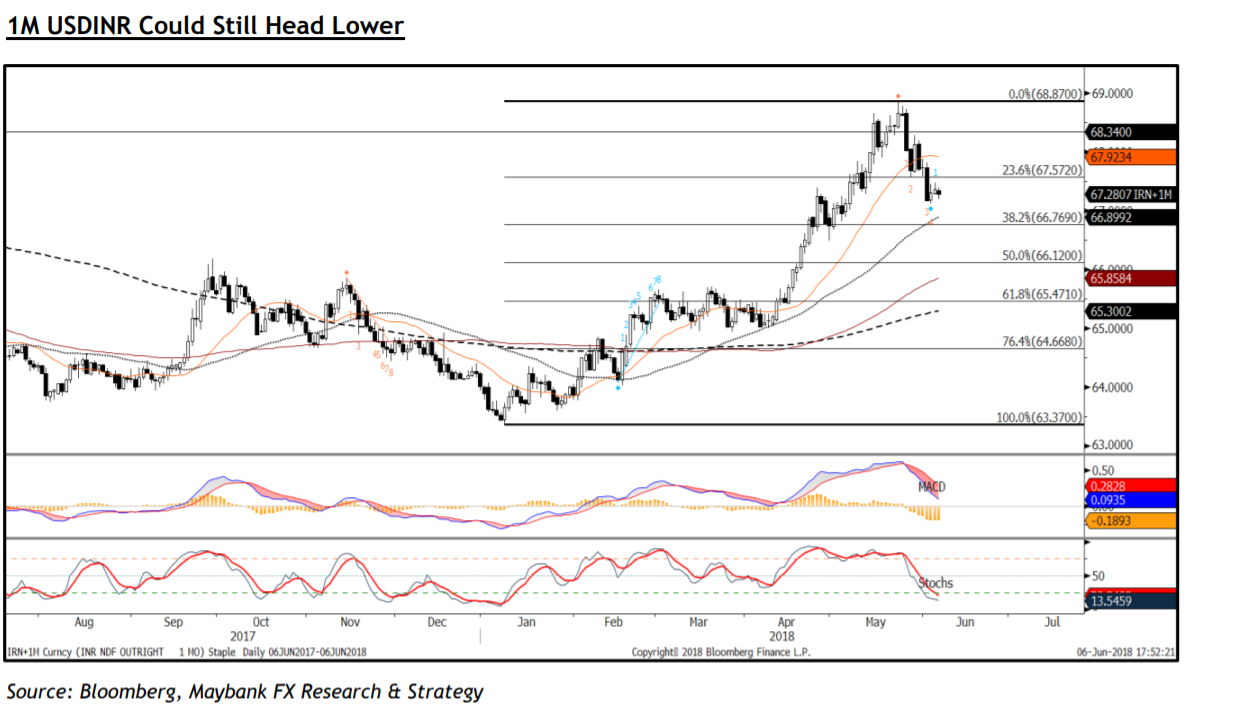

Above: Maybank graph showing USD/INR currency pair and technical analysis.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

Researchers at Emirates NBD say the Rupee's appreciation is likely to be more modest over the coming months, with USD/INR falling from the current spot rate of 67.45 to 66.5 by the end of June, and 67.0 in first quarter of 2019.

Aditya Pugalia, research director at Emirates NDB says he does not expect the RBI to commit to a "tightening cycle" and that the bank's monetary policy will be dictated by economic data.

"Interestingly, the RBI also maintained a neutral stance which indicates that this is not a start of a tighter monetary policy cycle but rather a pre-emptive strike," the strategist writes, in a recent briefing. "The neutral stance implies the RBI remains data dependent and has the option of staying put should further upside risks to inflation not materialize."

Overall Pugalia and the Emirates team say they see a slight bias toward higher rates due to inflationary pressures from rising food prices. Food inflation may rise over coming quarters because of pressure on the government to increase minimum price subsidies it pays farmers, as it made provision for this in its budget.

"We assign a low probability to that possibility given the pressure on the government to stimulate rural economy and believe that the RBI would hike at least one more time in FY 2019," Pugalia writes.

However, and on the downside, some global factors may remain a headwind for the Rupee. Particularly developments around oil prices, which have risen by 15% since the start of the year.

India has to import most of its oil and so higher prices mean the country has to sell more Rupees to buy the fuel imports that it needs. Oil accounts for around 30% of India's imports.

India also has a twin deficit, like the US, and it's often the case that currency analysts see this as an indicator of weakness up ahead. Twin deficits mean a country has a balance of payments deficit with the rest of the world and a budget deficit.

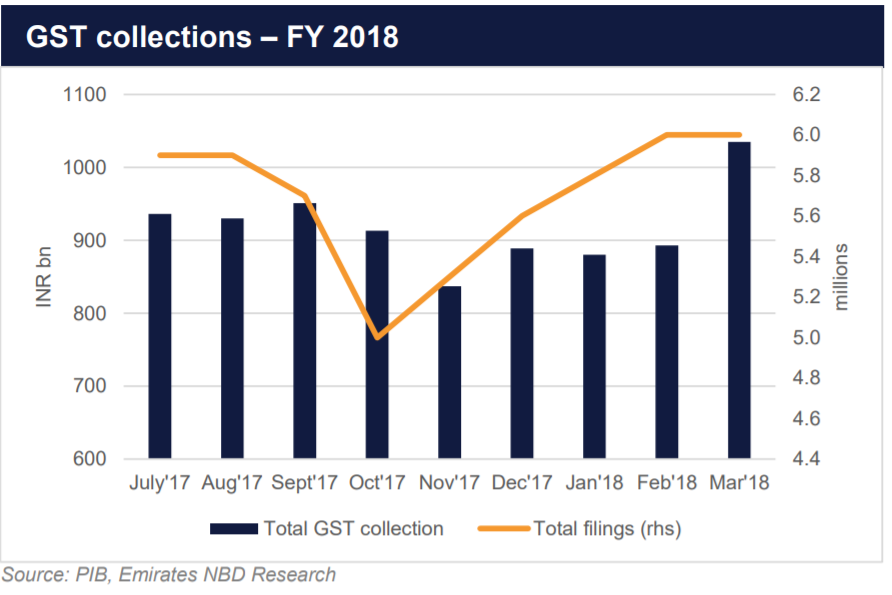

The government's budget deficit is unlikely to improve unless the government's new sales tax initiative does as it is supposed to and generates more revenue for the treasury.

Above: Emirates NBD Research graph showing treasury tax-take.

Finally, the Rupee continues to be at risk from falling inflows of foreign capital, normally institutional investors purchasing Indian bonds and shares, which has traditionally supported the currency. Recently, international investors have fallen out of love with Indian securities.

"India has not been immune to pressures faced by broader emerging markets," says Puglia. "Foreign institutional investors (FIIs) were net sellers for a second consecutive month in May to the tune of USD 1.2bn. In the first two months of Q1 FY 2020, FIIs have sold stocks worth USD 2.1bn. The trend was similar in debt markets with fourth consecutive month of outflows."

Yet the outlook is not terrible given the Indian stock market continues to perform relatively well when Indian financial services companies are removed from the equation.

Due to high levels of non-performing loans on their books, Indian banks have become less profitable and their stocks have performed poorly in recent times. For the rest of the stock market, however, profits rose by 9.0% on average in the previous year.

"Relative to consensus expectations, 65% of companies reported earnings in-line and/or ahead of forecasts. The strength in earnings was driven by stocks from materials, energy and consumer discretionary sectors," says Puglia.

Indian equity markets have a relatively low correlation with global markets, which can make them an attractive to portfolio managers looking for something to diversify their portfolios with.

In addition, the government has eased the rules on the maximum investment cap for foreign investors wishing to own Indian debt, which may increase investment in Indian bonds by foreigners during the months ahead.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here