The Office for Budget Responsibility surprised markets on budget day by downgrading forecasts for UK productivity - a subtle move with big implications for pound sterling.

- UK budget holds nasty surprise for GBP

- Bank of England keeps rates steady, cites Brexit risks for unanimous vote to do so

- But, GBP/USD could move higher to 1.46 as it clears 50 day moving average as US Fed gives the USD a kicking

The outlook for the British pound soured on details within the UK budget for 2016 that showed the UK's Office for Budget Responsibility (OBR) had cut forecasts for UK workforce productivity.

This did not make the headlines, but for GBP, it is incredibly significant and suggests the outlook for the UK currency will remain challenging going forward.

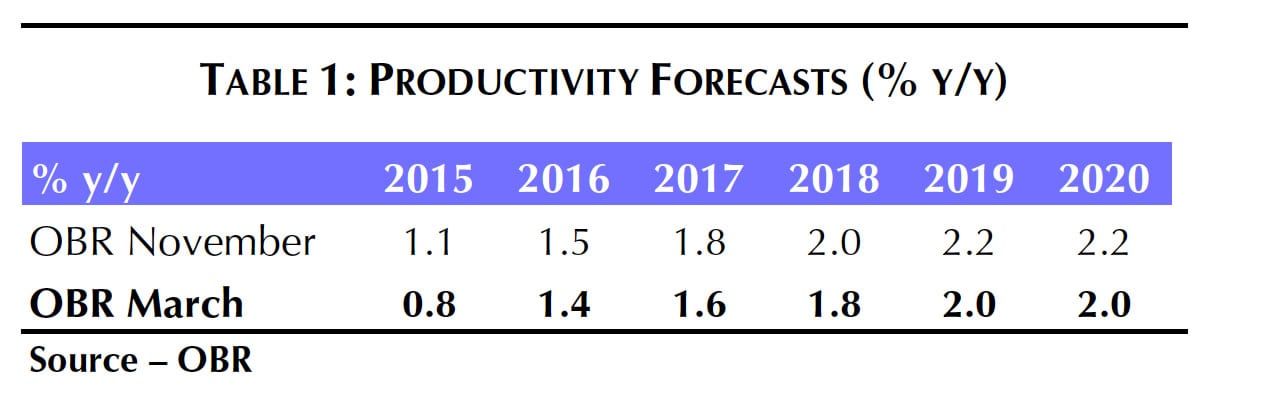

“It was unsurprising that the OBR revised down its growth forecast for this year (from 2.4% to 2.0%), given the recent signs of a slight slowdown,” says Capital Economics’ Roger Bootle, ”what was more unexpected was the way it revised down its productivity growth projections through the forecast.”

Talking about productivity is, essentially, a discussion on pay rises - if workers are receiving pay rises they are being rewarded for their increased productivity.

The side effect of pay growth is higher inflation which is in turn responded to by the Bank of England who raise interest rates to cap inflation.

The side effect of higher interest rates is a stronger pound which benefits from investment inflows as global investors look to take advantage of higher yielding UK investments.

So expectations for weaker productivity = expectations for less inflation = lower interest rates for longer = a weaker pound.

As we can see, the OBR expects productivity to grow going forward, however downgrades to the forecast have been made:

Less than four months since November’s Autumn Statement, the weaker news on output per hour since then has prompted the OBR to deem the previous signs of a pick-up a "false dawn".

We believe this downgrade to be unambiguously negative for the GBP.

Indeed, at the time of writing the pound to euro exchange rate is trading at it’s lowest levels since the end of February at 1.2724.

The British pound to dollar exchange rate traded to a two week low at 1.4100 before recovering on news that the US Federal Reserve may only raise interest rates on a maximum of two occassions in 2016.

Latest Pound/Euro Exchange Rates

| Live: 1.1673▼ -0.02%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1276 - 1.1323 |

**Independent Specialist | 1.151 - 1.1556 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

Why Does Productivity Matter for the Pound?

Since the onset of the 2007–08 financial crisis, labour productivity in the United Kingdom has been exceptionally weak.

“Measures of productivity can be used to inform estimates of an economy’s ability to grow without generating excessive inflationary pressure, which makes understanding recent movements important for the conduct of monetary policy,” says a note on the matter published by The Bank of England’s Monetary Analysis Directorate.

The Bank's Monetary Analysis Directorate notes that despite some modest improvements in 2013, whole-economy output per hour remains around 16% below the level implied by its pre-crisis trend.

Even taking into account possible measurement issues and secular changes in some sectors, this shortfall is large — and often referred to as the ‘productivity puzzle’.

The Bank has said in the past it believes a desire by involuntary part-time workers, such as those on zero-hour contracts, to work more hours is keeping productivity, and therefore inflation, low.

The pound rose through 2014 on the assumption that the productivity slack in the economy was being tightened and the Bank of England would therefore soon have to raise interest rates.

The Bank of England’s subsequent decision to keep interest rates at record lows will in part be due to a stubborn lack of productivity in the economy, which according to budget day developments, is now actually deteriorating.

Only when productivity picks up would a rate rise at the Bank of England be likely which would in turn provide sterling with a boost.

OBR Takes Away Autumn Statement Giveaway

So unlike in November at the time of the mid-term budget review, when the OBR gave the Chancellor a forecast windfall, the latest projections provide a big hit to the public finances.

“Indeed, the Chancellor learnt a harsh lesson that (as we had warned) what the OBR giveth, it can taketh away just as easily. The large downgrades to the nominal GDP forecasts flowed through to much lower underlying receipts, with only a partial offset from lower debt interest costs,” says Capital Economics’ Bootle.

Latest Wage Figures Suggest It's Not All That Bad

It's easy to get lost in a sea of negativity when looking at sterling in the current environment and it therefore remains important to air counter-consensus views when possible.

It therefore must be pointed out that ahead of the budget UK wage data were impressive.

UK average weekly earnings growth rose slightly more than expected to 2.1% year-on-year in the three months to January, rebounding from a 10-month low of 1.9% yoy in the three months to December confirming an improvement in productivity.

"Wage growth is likely to pick up gradually with inflation, supported by the low level of unemployment – thereby correcting some of the gap between wage weakness and low unemployment," says Vernazza.

Nevertheless, the economist concedes the data is unlikely to change the wait-and-see position of the BoE. "Wage growth remains weak and the economy is slowing. It is certainly in no mood to talk up the prospect of a rise in interest rates at its meeting this week," says Vernazza.

Outlook for the British Pound Soft, Bank of England Cites Brexit, Inflation for Keeping Rates Unchanged

Beyond the downgraded productivity forecasts, softer aggregate demand and reduced price pressures will likely keep the Bank of England on the sidelines.

“Ongoing austerity measures affirmed by Chancellor Osborne today keep intact our belief that the fundamental backdrop for the British pound is negative,” says Christopher Vecchio, Currency Analyst at DailyFX.

Vecchio says the stars are seemingly aligned against the Pound: geopolitically, Brexit is a plausible outcome now; monetarily, the BOE has consistently pushed back its rate hike timeline; economically, the current account deficit persists; and fiscally, austerity remains the prime directive.

"None of these factors have changed, keeping the British Pound vulnerable through the May elections and June referendum. More importantly, if what Chancellor Osborne is saying is true – that “storm clouds are gathering” – then today’s budget seems to do little to address the potential risks,” says Vecchio.

On Thursday the Bank opted to keep interest rates unchanged with a unanimous vote to do so.

The Bank noted core inflation remains subdued, a consequence of the past appreciation of sterling, weak global inflation and restrained domestic cost growth.

Furthermore, the Bank notes increased uncertainty surrounding the forthcoming referendum on UK membership of the European Union.

"That uncertainty is likely to have been a significant driver of the decline in sterling. It may also delay some spending decisions and depress growth of aggregate demand in the near term," read the minutes.

March Rally Kick-Started by Fed Decision

The GBP to USD has moved higher on Thursday despite the negativity surrounding sterling.

At the time of writing GBP/USD is at 1.4363 - around above where it started the week, which was at 1.4378.

Importantly, the gains registered over the past 24 hours take the exchange rate above its 50 day moving average, which is a positive development as it signals a good deal of market orders to sell sterling will have been cleaned out.

If a break of the psychological resistance at 1.44 can be achieved, and held, ahead of the weekend we could well see the March recovery extend to the major resistance zone located at the 100 day moving average at 1.46.

Expect an army of sell orders to test any strength at this level.