![]()

Image © Pound Sterling Live

The Bank of England will today start to prepare markets for an "insurance" interest rate cut in August, but analysts say this is hardly a trend-turning event for the Pound.

Pound Sterling was boosted by a stronger-than-expected UK inflation print on Wednesday, but the gains faded as investors turned their attention to Thursday's Bank of England interest rate decision.

The Pound to Euro exchange rate rose as high as 1.1860 after the inflation figures were released but returned to 1.1840 as investors considered whether the Bank would take the opportunity to communicate an August interest rate cut is likely. The Pound to Dollar exchange rate holds most of its daily advance at 1.2730, courtesy of broader USD weakness.

Money market pricing shows investors only see about a 30% chance of an August cut, meaning there is ample scope for repricing to happen after the Bank's update. Such a development would initially weigh on the Pound.

Alexandros Xenofontos, an analyst at TS Lombard, says the Bank of England might want to take out an "insurance cut" in August, similar to what the ECB did earlier this month. If this is the case, it must do some groundwork.

This could come in the form of another member of the Monetary Policy Committee voting to cut interest rates (2.0% headline inflation provides some decent cover) and/or language changes in the statement.

"The potential for GBP to move today is likely to come from the voting split. Seven Monetary Policy Committee members voted to keep the Bank rate steady in May. We consider those members will again vote to keep the Bank rate steady as they wait for more evidence of a broadening of slower inflation," says Joseph Capurso, an analyst at Commonwealth Bank.

An 'insurance cut' would allow the Bank to offer some protection against any material increase in domestic unemployment, which it might feel is not a risk worth taking as headline inflation fell back to the 2.0% target in May.

Xenofontos says there is scant evidence that inflation risks are rising, and "the labour market is starting to look shaky". He says economic growth will also likely fade in the second half of the year following a strong start to 2024.

"All this keeps the Committee on track to deliver an "insurance" cut in August/September and then adopt a 'wait-and-see' stance while monetary settings are kept restrictive, albeit to a lesser degree – in line with our call (and not unlike what the ECB is communicating)," says Xenofontos.

Although the process of building towards an August interest rate cut would result in some initial GBP weakness, the extent looks limited. After all, there was little material damage to the Euro following the ECB's cut and we note developments in France have been more influential.

Ultimately, for the GBP outlook, it is the quantum of rate cuts that will count more than the start date. With this in mind, most economists agree the pace of rate cuts will likely be shallow beyond August.

"We doubt that the BoE rate decision will be a material risk for GBP given the lack of communication from the MPC since the election announcement. Consequently, we stick with our bullish call on GBP versus the funding," says Kamal Sharma, FX strategist at Bank of America.

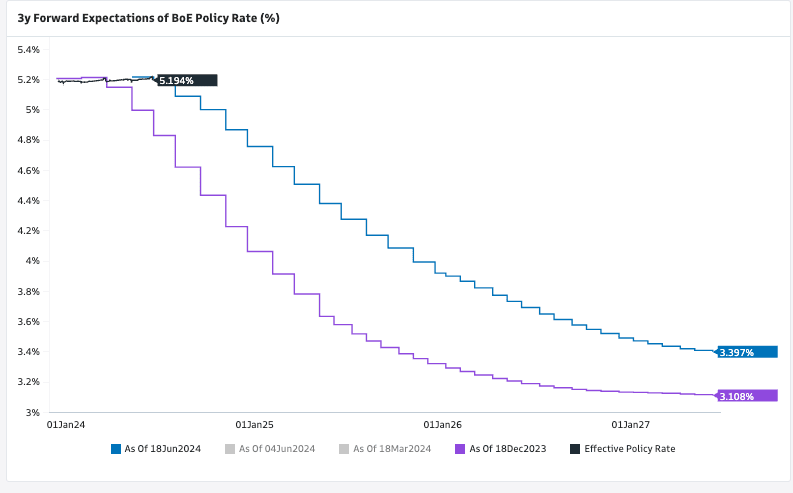

Above: It's the depth of the cuts to come that matter. The chart shows that since December, the number of rate cuts expected by the market has been reduced. Image courtesy of Goldman Sachs.

Risks to the Pound-Dollar outlook will ultimately hinge on the U.S. side of the equation. The next calendar event to watch is the U.S. PCE figures, due next week. For Pound-Euro, French election risks will dominate proceedings.

"The BoE’s June meeting is unlikely to move GBP much," says Yusuke Miyairi, an FX strategist at Nomura. He looks for further Pound Sterling advances against the Euro into the French and UK elections.

"We remain relatively bullish on GBP, with the domestic data not sufficiently weak for the BoE to commence its rate cutting cycle yet," says Miyairi.

Shahab Jalinoos, a strategist at UBS, says UK interest rates are unlikely to fall fast enough to bother Sterling:

"The UK’s likely persistent rate advantage is helpful for GBP at a time when UK data are improving as real incomes slowly start to rise."

He also points out that UK politics could prove supportive of the Pound: "If the 4 Jul general election results in a clean Labour win as polls suggests, there could even be a 'feel good' honeymoon phase that sees economic data stay robust too. In that context, the risk to our EURGBP 0.8400 target is firmly to the downside."

EUR/GBP gives a GBP/EUR forecast of 1.19.