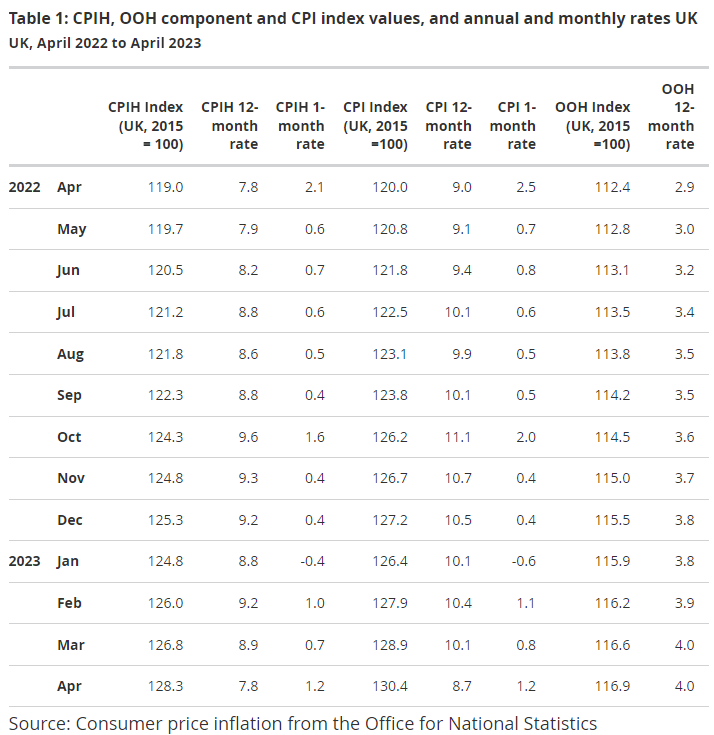

"The easing in the annual inflation rate in April 2023 mainly reflected price changes in the housing and household services division" - Office for National Statistics.

Image © Adobe Images

Pound Sterling exchange rates fell widely in midweek trade after UK inflation fell less than many forecasters expected for the recent month with possible implications for the Bank of England (BoE) interest rate outlook, though analysts and economists have a wide range of views on the outlook.

Inflation fell less than expected by the consensus among economists and forecasters at the Bank of England (BoE) when data for the month of April was released by the Office for National Statistics (ONS) on Wednesday.

Overall inflation fell from 10.1% to 8.7% for the year to month-end to come in above the BoE's forecast while core inflation rose from 6.2% to 6.8% once food, energy, and regulated price items like alcohol and tobacco are set aside.

"The easing in the annual inflation rate in April 2023 mainly reflected price changes in the housing and household services division, particularly for gas and electricity," the Office for National Statistics said.

"This was offset partially by upward effects coming from recreation and culture, alcoholic beverages and tobacco, communication, and transport," it added.

One possible result of the overshot relative to the BoE's forecast is that it could invite a stronger monetary policy response entailing a higher Bank Rate, an enhancement of the current quantitative tightening programme, or both.

The BoE raised Bank Rate from 4.25% to 4.5% this month and indicated it would likely raise it further to 4.75% before all is said and done.

But government bond yields climbed sharply on Wednesday to imply that Bank Rate could be lifted to 5% or more later this year.

Below is a selection of views from analysts, economists and others setting out what they think the data is likely to mean for interest rates and Pound Sterling.

Brad Bechtel, global head of FX, Jefferies

"The blow out inflation numbers from the UK are catching the market off guard in the morning session in London."

"The GBP initially rallied as everyone assumed it meant higher terminal [rate] for the BoE as well, and it very well might with futures now pricing 5.5% terminal, but it also highlights the fact that growth will have a hard time holding up if the BoE is forced to continue hiking."

"GBP/USD rallied initially up to 1.2470 the high and then reversed hard back to 1.2370 now. We open NY at the lows and are likely to continue lower with our forecast near term holding steady at 1.2282 the 100-day moving average. We will reassess there and perhaps look for a bigger move lower."

Bipan Rai, North American head of FX strategy, CIBC Capital Market

"Stronger than expected inflation numbers out of the UK this morning imply that the BoE is likely to raise rates again next month. Indeed, we’re now leaning towards an additional 25bps hike – even with the May CPI numbers coming out a day before that decision."

"We’re still non-committal on the August decision for now. GBP/USD is softer to start things off – in-line with the general tone in the USD. We expect price action to test weak support at the 1.2340 area at some point today and we’ll be monitoring price behaviour to see if it holds."

Sid Bhushan, economist, Goldman Sachs

"Today’s strong UK inflation print was broad-based across goods and services but partly reflects contract resetting, for example for telecommunication services."

"BoE Governor Bailey will have a chance to respond to the data when he speaks at a WSJ event on ‘Inflation and the Economy’ at 2pm London time today, where he will address how much further rates may need to rise, and how that may affect growth and financial stability risks."

Abbas Khan, economist, Barclays

"Despite the expected drop in headline inflation on energy base-effects, CPI, core CPI and RPI printed well above expectations. In CPI, services inflation accelerated a little more than we expected, but the big upside surprise was in core goods."

"This print increases risks that the BoE will hike Bank Rate after June."

James Smith, developed markets economist, ING

"What matters for the Bank of England is services inflation, and that edged up to 6.9% from 6.6% previously – higher than expected. Much of this seems to be down to firms making more widespread changes to prices that are typically reset on an annual basis."

"Some of this was expected, for example, telecoms prices typically change this time each year. But there were some surprises, including rents which rose by 1.4% on the month, which was the highest month-on-month increase in more than a decade."

"There are good reasons to think services inflation is at its peak, and we think the fall in gas prices should alleviate one major source of cost pressures in the sector. Nevertheless, this latest data raise the chance of another rate hike next month."

"It's not a foregone conclusion, not least because we still have another set of data before the meeting, and remember the jobs/wages data has been moving in the right direction, as have broader survey measures of price-setting behaviour."

Charles Hepworth, investment director, GAM Investments

"This puts further pressure on the Bank of England to remain skewed to a monetary tightening stance. Further, a 5% base rate level in the months ahead looks more than likely after this inflation number."

Douglas Grant, CEO, Manx Financial Group PLC

“Back to single digit inflation for the first time this year and having narrowly avoided a recession, the UK economy could be showing signs of resilience. However, interest rate hikes and the latest flatlining GDP data continue to bring challenges that businesses are struggling to outmanoeuvre."

"Indeed, coupled with the global banking sector showing signs of weakness, SMEs must take this as a reminder to review their existing lending structures and ensure they can keep ahead of the storm."

"While many SMEs were proactive by locking their debt into fixed rate structures, it is now too late for other businesses that have borne the brunt of spiralling costs without a financial safety net. The government should intervene to mitigate the impacts on SMEs, which are the backbone of the UK economy."

Rosie Hooper, chartered financial planner, Quilter

"While inflation has finally fallen below double-digits to 8.7%, this is still high and way above the 2% target. People's buying power continues to be squeezed, meaning it might be more difficult to keep up with regular living expenses and still have money left over for mortgage payments or paying off other debts."

"High inflation erodes the value of savings over time in real terms, while higher interest rates help to grow your savings at a greater rate. However, if for example inflation is around 10% but your bank is only paying a savings interest rate of 5%, then you are essentially losing half of your money. This can make it more difficult to meet financial goals, such as buying a home or saving for retirement."

"To combat the effects of inflation, individuals may need to save more or invest their money in financial vehicles that provide a higher return. Although the stock market has had a difficult period, historically, investing has provided inflation-beating returns over the long term."

Richard Carter, head of fixed interest research, Quilter Cheviot

"While this fall in inflation shows things are beginning to move in the right direction, we cannot ignore the fact that there is an incredibly long way to go. Inflation at 8.7% is still eye-wateringly high with prices rising steeply, and we are unlikely to see such significant eases as this in the coming months."

“While the Bank of England has made no promises that it is nearing the end of its hiking cycle as far as interest rates are concerned, it will be relieved to see inflation has finally budged. For as long as wage growth continues to increase, the Bank will keep the option of further interest rate rises firmly on the table – and particularly if core inflation remains persistently high.”

Charles White Thomson, CEO, Saxo UK

"The status quo in the UK is increasingly painful and uninspiring - this should not be about celebrating falling inflation or the avoidance of a technical recession. The UK continues to underperform its key counterparties and have underserved the majority and their aspirations."

"We are now in an economic danger zone, pincered between public enemy number one/ inflation, a 19% increase in food and non-alcoholic beverages which reaffirms the cost of living crisis, and a consumer saddled with outsized debt that was once cheap."

"The conundrum facing the UK is more than just beating public enemy number one, or inflation, it is about defeating the high tax and low growth loop and the lovers of the status quo or managed decline."