- GBP, RMB, CAD et al FX reserves rise in Q4

- As USD share of global receive basket ebbs

- But Q1 FX reserve data could look different

- Ukraine invasion prompted FX interventions

- Heavy selling of USD, EUR, JPY, GBP et al

Image © Pound Sterling Live

Pound Sterling was one of many smaller currencies to benefit from a further ebbing of the U.S. Dollar’s dominance in central bank foreign exchange reserves late last year, according to newly released International Monetary Fund (IMF) data, but the overall basket could look quite different next time around.

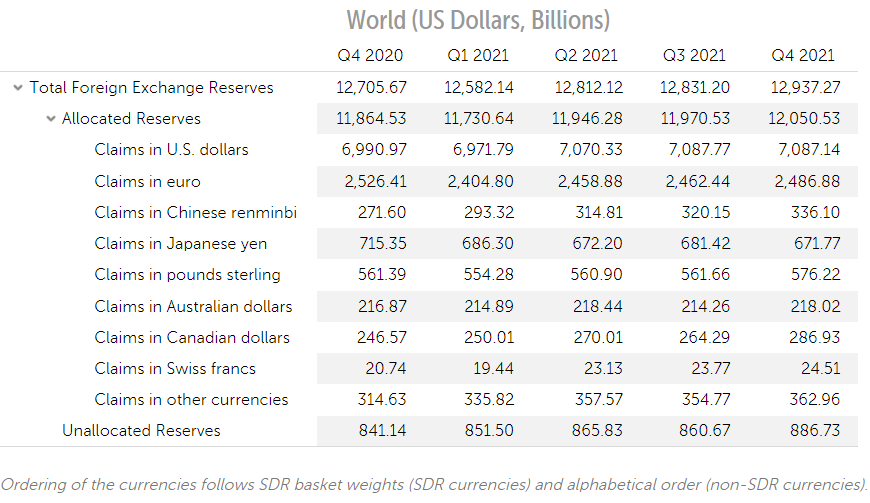

Central banks bought more currency reserves in the final quarter, lifting the total value of allocated reserves by around 0.7% to just more than $12.05 trillion in the IMF’s latest Composition of Foreign Exchange Reserves report.

Despite the growing basket, the U.S. Dollar’s share slipped to 58.81% from 59.21% in the prior three months, making for a new all-time low.

“The RMB and GBP rose 0.1ppt with even smaller currencies (CAD, AUD, CHF and others) adding 0.3ppt amongst themselves,” says Dominic Bunning, head of European FX research at HSBC.

“There is nothing in the data suggesting a seismic shift is occurring in reserve allocations, although obviously it covers a period before sanctions on the Russian central bank gave rise to increased commentary about the USD’s status,” Bunning also said on Thursday.

Above: Composition of Foreign Exchange Reserves. Source: IMF.

When measured in U.S. Dollar terms rather than as a proportion of the basket, the fastest growth was seen by the Canadian Dollar while holdings in Renminbi, Sterling, Swiss Franc and "other currencies" all picked up further too.

Last quarter’s pecking order would, however, have been influenced by changes in the value of each currency relative to the Dollar, in addition to the performance of government bond markets in each country so is not necessarily the most accurate reflection of shifting allocations.

“This is not to say reserve diversification does not matter (the USD may have been even stronger in its absence) – but only a faster pace will influence the overall FX trend,” says Adarsh Sinha, an FX strategist at BofA Global Research.

{wbamp-hide start} {wbamp-hide end}{wbamp-show start}{wbamp-show end}

While the U.S. Dollar’s share of global reserves ebbed last quarter and most other smaller currencies appeared to benefit from this, the entire basket could look quite different when the first quarter 2022 report is released in June.

Exactly how different the basket looks next quarter would depend on how much central bankers in Europe and elsewhere sold during late February and the opening week of March when the financial fallout from Russia’s invasion of Ukraine was at its most acute.

Given that the Dollar, Euro, Yen, Sterling and Renminbi account for the bulk of all reserves, it’s almost inevitable that any first quarter selling would have been concentrated in these currencies, and this could have led their respective shares of the basket to fall during that period.

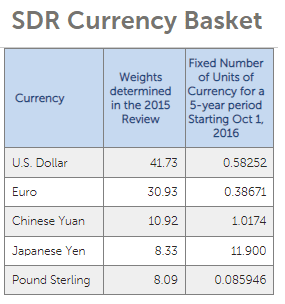

Above: Currencies and weightings within the IMF special drawing right, which is itself a reserve asset and an integral pillar underpinning the international financial system. Source: IMF.

“Over recent months Asia Pacific FX reserves have dropped, even discounting valuation effects, highlighting the growing pressure on Asian FX as markets price in higher US rates,” says Mitul Kotecha, chief EM Asia and Europe strategist at TD Securities.

“There are significant risks that the region's FX reserves decline proves more durable given the likely worsening in current account positions amid higher energy prices and reduced portfolio inflows,” Kotecha wrote in a Tuesday research briefing.

Data covering the first quarter will be released on the final day of the second quarter and could look different to Thursday's because Russia’s February 24 invasion of Ukraine left numerous central banks with little choice other than to sell reserves in order to support their own currencies.

The Narodowy Bank Polski even announced to the market that its $160BN war chest was used repeatedly in an effort to stabilise the Zloty and to also provide “huge support” to the Ukrainian central bank and currency.

Many have speculated that a G7 freeze on Central Bank of Russia assets, as part of its sanctions response, could have encouraged third party central banks to sell U.S. Dollars but this overlooks that almost all countries with major reserve currencies also participated in the sanctions and asset freeze.

“The USD’s gradually declining share of reserves may continue as a result of the world moving in the direction of a multipolar international financial and monetary system. But it will likely remain a slow process and right now there is no clear alternative as a direct replacement,” HSBC’s Bunning said Thursday.