Image © Foreign and Commonwealth Office, Reproduced Under CC Licensing

- Chancellor's 'enormous' 'giveaway' to boost growth in 2019

- Fiscal expansion could bode well for Sterling in 2019

- Expect two interest rate rises at Bank of England in 2019

- But near-term expect Sterling to remain weighed by Brexit

The British Pound and financial markets are underestimating the prospect of interest rate rises at the Bank of England in 2019 say analysts who reckon the recently announced U.K. budget will boost economic growth over coming months.

Sterling drifted lower yesterday, apparently ignoring the release of the U.K.’s 2018 budget, but we believe this response is telling and sets up the currency for a notable jump in coming months.

Pent up demand for the currency is likely to be released on any decent Brexit deal we believe.

Our takeaway from budget 2018 is that it bodes for a stronger Pound longer-term as the looser fiscal policy signalled by Chancellor Philip Hammond will ultimately command higher interest rates at the Bank of England.

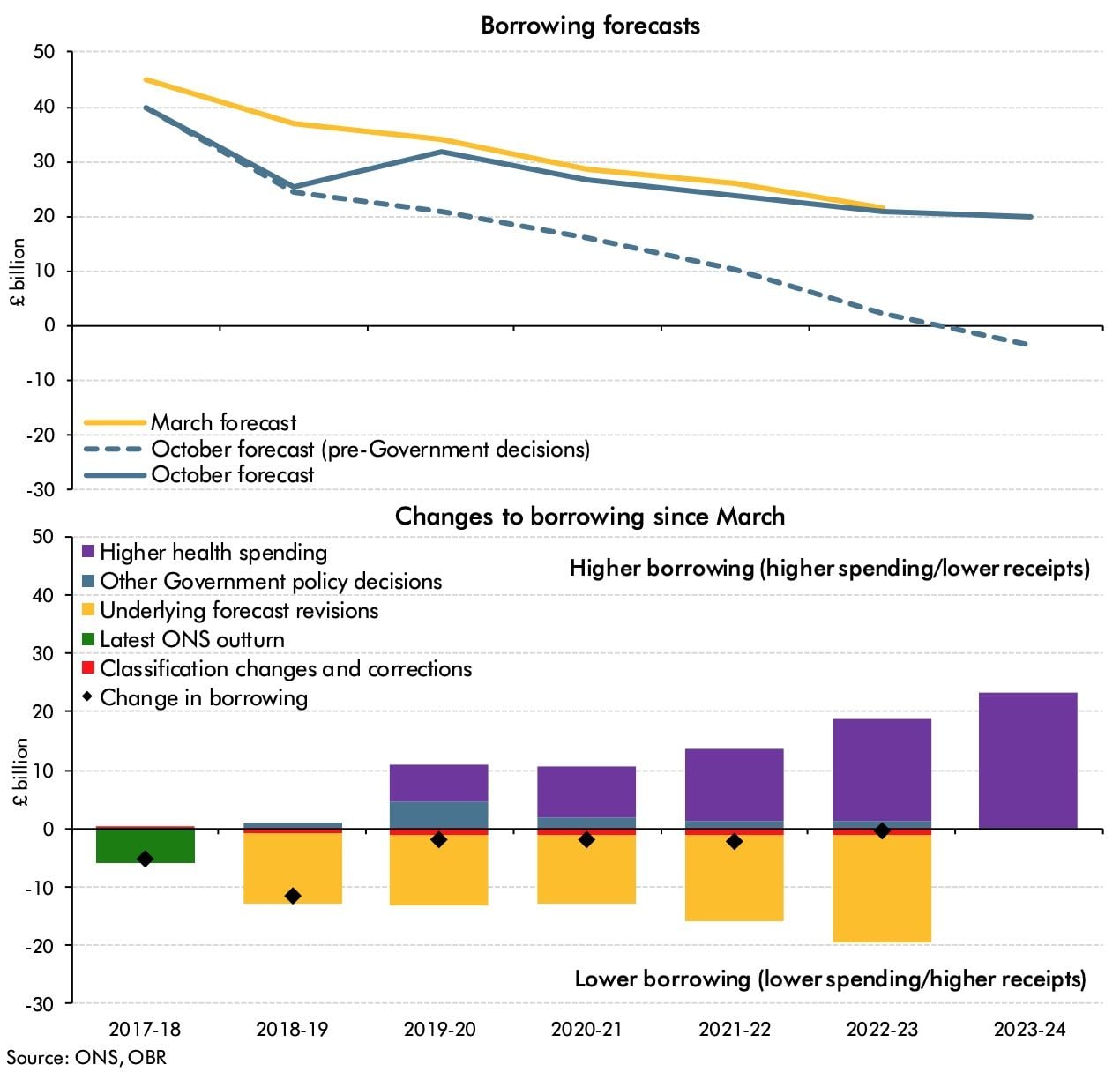

The U.K.’s cyclically‑adjusted budget deficit (budget deficit adjusted for the economic cycle) is projected to widen from 1.3% of GDP in 2018‑2019 to 1.6% of GDP in 2019‑2020.

This puts the U.K. fiscal impulse back into expansionary territory after years of fiscal caution as the country desperately sought to rein in the spending largesse that bloated the country's debt pile.

"This fiscal impulse will be a modest tailwind to U.K. economic activity over the next year," says Joseph Capurso with Commonwealth Bank Australia.

Any tailwind to U.K. economic activity should be interpreted as being positive for Sterling.

The Office for Budget Responsibility (OBR) assumes most of the £11.6B likely undershoot in borrowing this year is a result of a permanent improvement in the outlook for tax revenues.

According to the OBR, the cumulative borrowing forecast between 2018/19 and 2022/23 would have been revised down by £68.5B if the Chancellor had kept to the Spring Statement plans.

"This Budget will be remembered as the moment when the Government finally threw in the towel on plans to run sustainable public finances," says Samuel Tombs, Chief U.K. Economist with Pantheon Macroeconomics.

Analysis suggests Chancellor Philip Hammond's discretionary policy changes will boost cumulative borrowing between 2018/19 and 2022/23 by a hefty £55.3BN.

"The give-away was enormous by the standards of recent Budgets," says Tombs. fiscal policy now will boost GDP growth modestly next year."

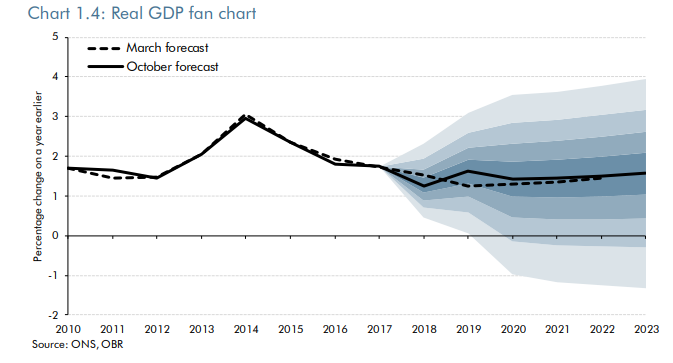

GDP growth for 2019 was upgraded by the Office for Budget Responsibility from 1.3% to 1.6%. 2020 growth was forecast at 1.4%, up from 1.3% while growth in 2021 remains unchanged at 1.4%.

Overall, total government expenditure is set to stabilise at 38% of GDP over the next five years, having fallen every year since its 2010 peak of 45%.

"As a result, it’s not hyperbole to talk of the 'end of austerity'," adds Tombs.

Advertisement

Bank-beating exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here

What's in it for the Pound?

The reaction by the British Pound to the budget was distinctly one of ambivalence.

The Pound-to-Dollar exchange rate edged lower to sub-1.28, taken away by a broader rally higher in the U.S. Dollar. The Pound-to-Euro exchange rate tracked sideways around the 1.1250 market which is actually a longer-term multi-month fulcrum for the exchange rate.

The sanguine response by Sterling mirrors expectations for Bank of England interest rate moves in 2019 and 2020. In short, markets have not shifted their expectations for a move at Threadneedle Street as a result of the budget.

We are therefore now in an interesting situation with regards to the Pound: the expansionary policy of the government could well stimulate inflation in 2019 which would force the Bank of England to respond and raise interest rates.

A side effect of higher interest rates is a stronger Pound as foreign capital flows into the U.K. to take advantage of the improved returns.

But, markets are still only barely pricing in one interest rate rise in 2019.

There is therefore a big risk that markets are currently underpricing Sterling relative to where it could end up in 2019.

According to Paul Hollingsworth at BNP Paribas, two interest rate hikes are in prospect in 2019, more than markets expect and if they are correct we see this as being notably constructive for Sterling as the market will inevitably have to bid the currency higher to reprice from barely one rate rise to two.

"At face value, the Chancellor’s Autumn Budget read more like a pre-election budget, than a pre-Brexit one, with a sizeable net giveaway planned next fiscal year which will provide considerable support to growth," says Hollingsworth.

BNP Paribas say the package of measures will deliver a discretionary fiscal stimulus equivalent to 0.3% of GDP in 2019-20, with hints of more to come should the UK secure a Brexit deal.

Panthon's Tombs says "the Chancellor's largesse will embolden the MPC to step up the pace of interest rate hikes next year."

Pantheon Macroeconomics expect the MPC to raise Bank Rate twice next year—in May and November — provided a no-deal Brexit is avoided.

Sterling to Remain Soft Near-Term According to Forecasts

While the budget and expected economic path of the U.K. economy bode well for Sterling in 2019, markets are clearly not keen to chase the currency higher incase Brexit negotiations collapse and a 'no deal' Brexit takes place in March 2019.

This outcome would see the Government immediately bin the current budget plans and announce an emergency budget.

No wonder markets are a little nervous to bid the Pound.

"GBP markets will want to see convincing evidence of a soft Brexit landing before chasing any upward growth revision. The UK economy isn't that bad and the tailwind of this + reduced Brexit uncertainty could be a powerful boost for GBP in 2019. Too early to price this story," says Viraj Patel, a foreign exchange strategist with ING Bank N.V.

Patel says any announced exit deal over the next few weeks could see markets all but fully price out the risks of a no-deal Brexit – thus fuelling further bullish GBP momentum.

ING target GBP/USD moving to 1.34-1.35 in the coming months with a potential overshoot to 1.37-1.38.

However, no big announcement by late November could see GBP/USD falling back to 1.27-1.28, which would take EUR/GBP to 0.90, which gives a GBP/EUR exchange rate of 1.11.

Consensus forecasts by the world's leading 50 investment banks suggests Sterling will end higher than current levels against the U.S. Dollar by the time 2018 draws to a close.

However, against the Euro the Sterling could still be a little overvalued. For these consensus forecasts, which include targets from Goldman Sachs, J.P. Morgan, HSBC and Barclays please see the Horizon Currency consensus reports. GBP/USD is accessed here, GBP/EUR is accessed here.

Advertisement

Bank-beating GBP exchange rates: Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here