The euro has powered higher in early December, however the longer-term trend lower against the British pound should prevail into the new year.

Expect the euro exchange rate's journey lower to continue; however the extend of declines will vary according to which currency the euro is up against.

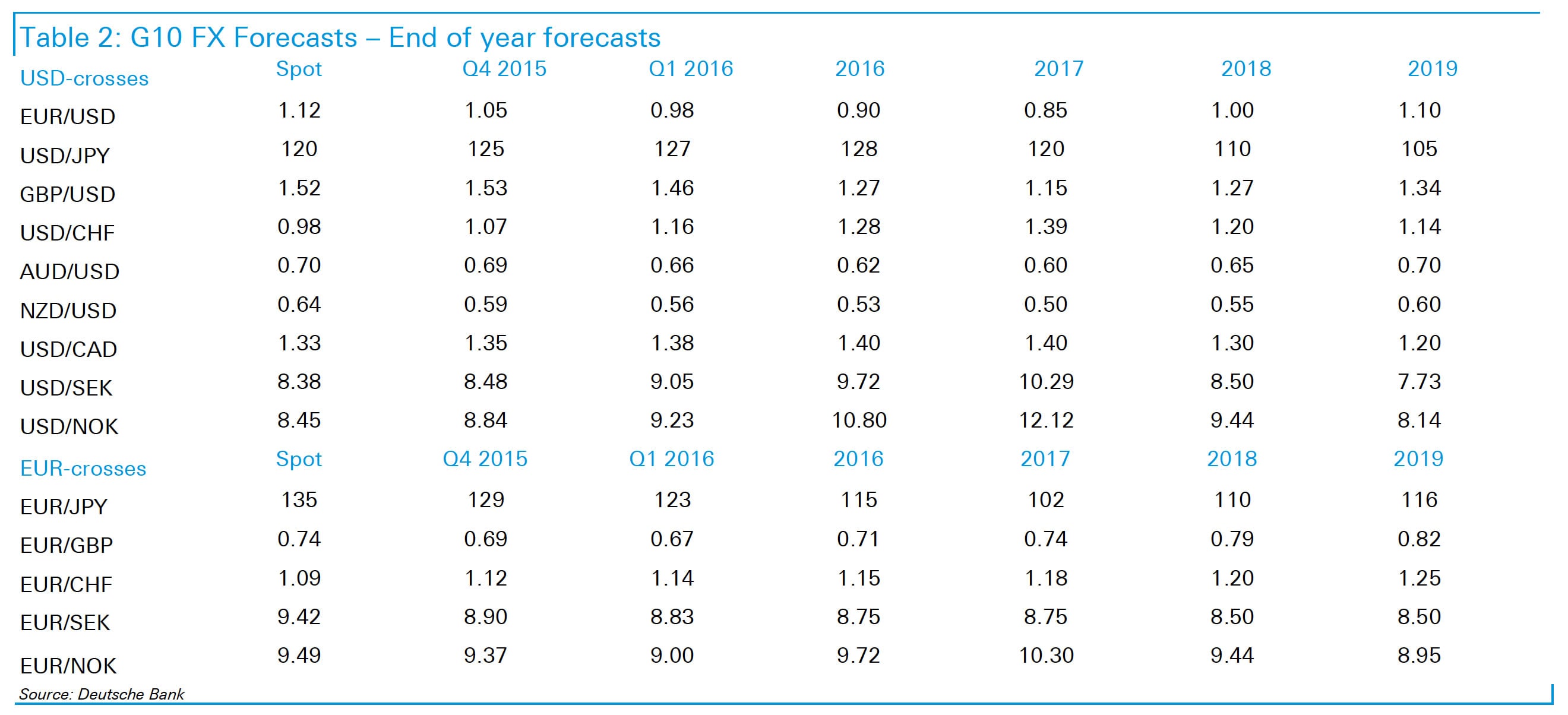

One of the most eye-opening euro forecasts to have landed on our desks recently is that concerning the projections on EURUSD at Deutsche Bank.

The bank is out-of-consensus on their call for the euro dollar’s move lower over 2016 seeing it close the year at 0.90. Still, it is higher than expectations held at ABN Amro who take the crown for being outliers in our compilation series.

Nevertheless, there are two distinct camps emerging - those like Deutsche and ABN Amro who are aggressively bearish on euro dollar and those, like HSBC and Intesa Sanpaolo who are more bullish on the conversion in the year-ahead.

Deutsche Bank: EURGBP Avoids Fate of EURUSD

This brings us to the euro to pound sterling forecasts held at Deutsche Bank - the euro is projected to fare better against its European cousin in 2016 that is expected against the dollar.

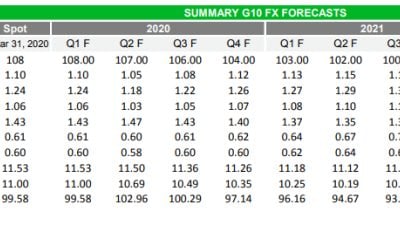

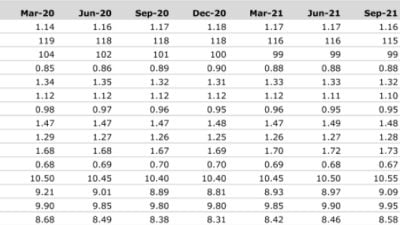

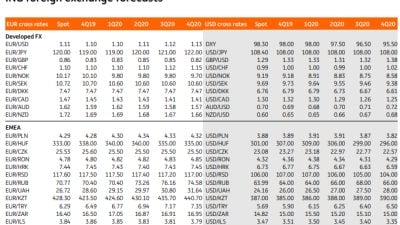

Forecasts see the EURGBP falling to a cyclical low of 0.67 in the first quarter ahead of a recovery to 0.71 by year-end.

In GBP to EUR terms, this equates to a best of 1.49 for sterling against the euro and a year-end close back at longer-term support of 1.40.

“We don’t believe that it’s time to turn bearish sterling yet. The risk remains that the Bank of England defies markets by tightening sooner than currently anticipated, capital inflows both portfolio and M&A continue to be healthy and participation in the long GBP trade has lightened up,” says a note on the UK currency from Deutsche Bank.

Latest Pound/Euro Exchange Rates

| Live: 1.1603▲ + 0.02%12 Month Best:1.1754 |

*Your Bank's Retail Rate

| 1.1208 - 1.1255 |

**Independent Specialist | 1.1441 - 1.1487 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

From next year, however, analysts join a host of other institutional forecasters in assuming the sterling cycle is likely to reach maturity.

“Valuations are quite stretched, with the cross the most expensive against the dollar among all the majors,” say Deutsche Bank.

Indeed, the GBP to USD conversion is seen as low as 1.15 in 2017.

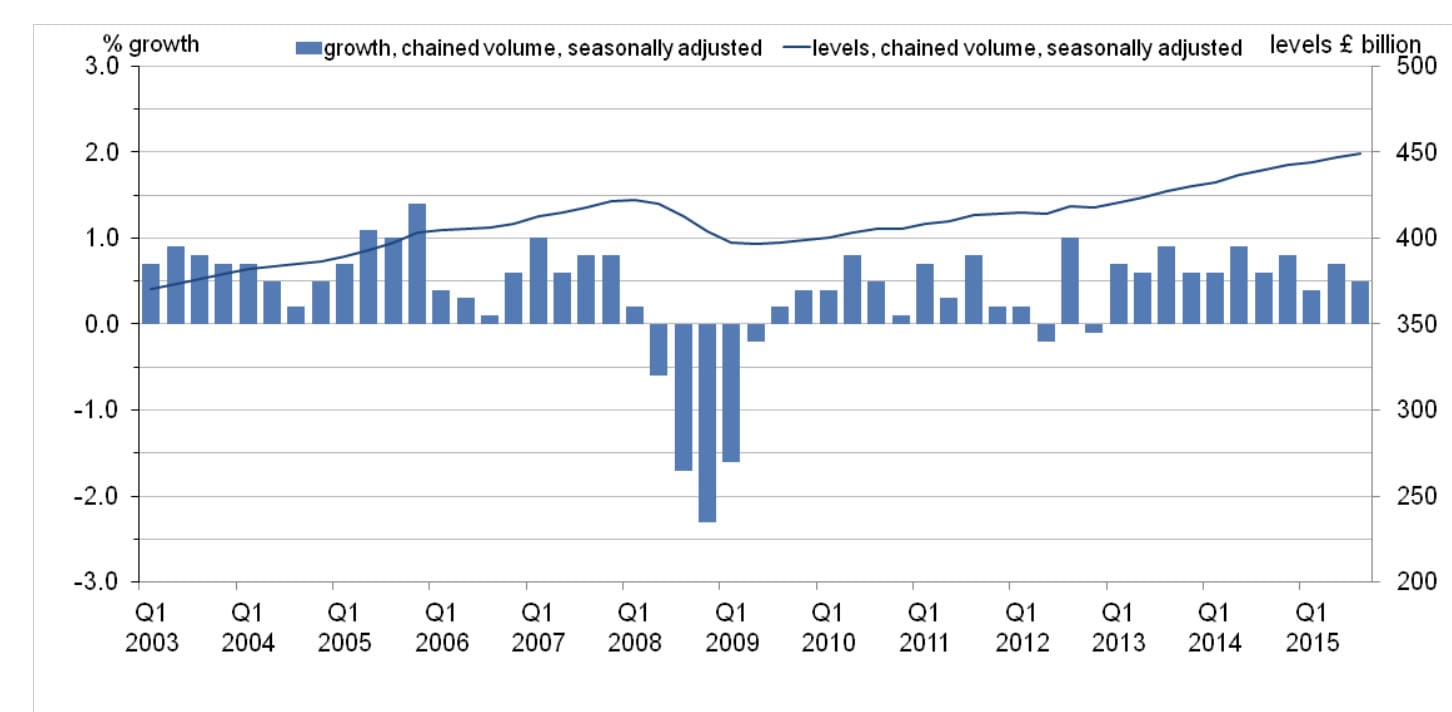

UK growth continues above potential but has slowed, noticeably from its peak in Q4 last year.

Deutsche Bank say they are also concerned by the UK’s reliance on consumption as a growth driver which raises questions about sustainability.

Furthermore, savings rates are near all time lows raising questions over whether or not the UK consumer has learnt anything from the financial crisis.

There is the added issue of fiscal tightening (i.e spending cuts) which will keep a lid on growth.

Despite what appeared to be a give-away budget, George Osborne will still oversee substantial saving cuts in 2016.

This brings us on to the dreaded Brexit issue which should be the key source of volatility and potential downside in the year-ahead.

“Political risks are set to re-emerge yet again, with an in-out EU referendum expected next autumn, while the recent election of a far left leader of the opposition Labour party could pose unexpected challenges,” say Deutsche Bank.

This could all make financing a very wide current account deficit difficult.

“We therefore see EUR/GBP grinding higher from early next year, which combined with a steep forecast fall in EUR/USD, will see a meaningful decline in GBP/USD,” say Deutsche Bank.

Notably, the parity forecast by end-year has come under pressure not least because spot is over 10% away with less than 4 months left of the year.

Analysts have accordingly revised our year-end forecast to 1.05, reflective of a view that the EUR will weaken against the USD either i) because the risk environment will be constructive enough to allow for a first Fed rate hike; or less likely because ii) any environment that does not allow the Fed to tighten is also one that will force the ECB to augment their existing QE program.

"Neither scenario is close to being priced in, and in the meantime EUR/USD has overshot recent interest rate spreads, suggesting that the EUR’s starting point is ‘rich’ to begin with," say Deutsche Bank.

In capital flow terms, the European outflow story continues unabated and continues to be the main driver of currency conversions.

"Euro-area portfolio flow data up to July show the sixth consecutive month of large fixed income outflows, this time driven by foreign liquidations of Euro-area bonds. Declining EM reserves combined with the bund VaR shock of Q2 are likely helping the trend and the former is expected to be an ongoing feature in the months ahead," say Deutsche Bank.