File image of ECB President Christine Lagarde. Photo by Sanziana Perju / European Central Bank.

The euro loses value against the dollar as trading volumes pick up once more.

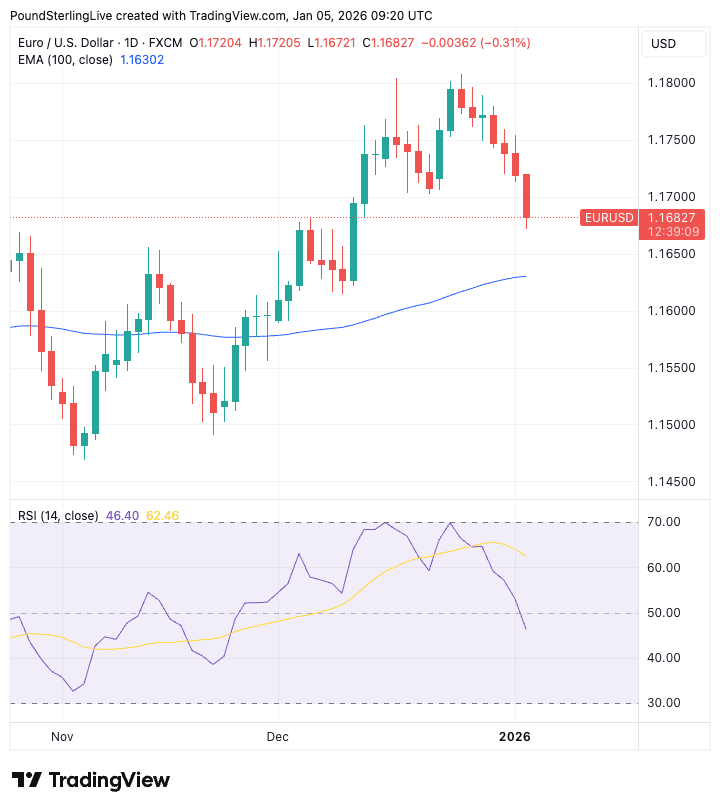

The euro to dollar exchange rate (EUR/USD) falls a third of a per cent at the start of the new week to 1.1679 in sympathy with a broader bid for the dollar.

The popular opinion amongst the talking heads is that the move owes itself to geopolitical tensions escalating following U.S. military operations in Venezuela at the weekend.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

President Donald Trump also signalled potential moves on Greenland and Colombia, suggesting the U.S. will be far more muscular on foreign policy than has been the case for some time.

The knee-jerk takeaway offered by analysts is that these tensions are bad for investors, prompting them to find the safety of USD cash.

However, that global stock markets are firm on Monday blows a hole in this theory, suggesting the dollar's bid has other factors behind it and that Trump's Venezuelan adventure is not quite the market-moving event that some excitable commentators might suggest.

We think that the dollar is paring oversold conditions that built up at the back-end of last year: we saw the currency reach oversold conditions against majors such as the euro and pound.

For instance, the Relative Strength Index (RSI) on the euro-dollar's daily chart reached overbought conditions on December 23 when it hit 70 (see lower panel in chart).

The mean-reverting nature of the RSI meant that downside pressures started mounting when this figure was reached, necessitating a drawdown in euro-dollar.

That drawdown is well underway now as the RSI dips below 50, confirming building downside momentum.

Our short-term forecast is for the pair to at least target the 100-day exponential moving average at 1.1630, where it will draw breath.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

While above the 100-day EMA the outlook remains constructive and consistent with a resumption of the euro's rise through the latter part of January and into February.

Helping the euro this week will be another firm CPI inflation reading from the Eurozone on Wednesday, where core CPI inflation will come in at 2.4% y/y according to a survey of economists.

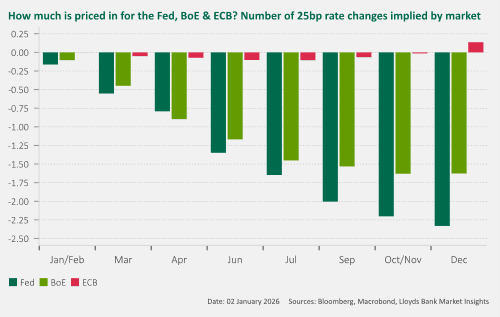

This is consistent with the European Central Bank maintaining interest rates at current levels for an extended period, which will offer the euro support against the dollar, where the Federal Reserve will withdraw support as it lowers its own base rate on a number of occasions this year.

Above: The ECB bestows a distinct interest rate advantage on the euro going into the new year. Image courtesy of Lloyds Bank.

"The ECB is in a good place to keep rates on hold at 2.00% for some time with the next move a hike. The swaps curve price-in steady rates over the next twelve months and a full 25bps rate increase to 2.25% in the next two years," says Elias Haddad, analyst at Brown Brothers Harriman.

Given the static nature of ECB policy and the dynamic nature of U.S. policy, the onus will fall on U.S. data to exert influence on the euro-dollar in the coming days.

📊 Monday brings the ISM manufacturing PMI release, which should shed light on how the sector fared in December. Here, another downbeat sub-50 reading is expected, consistent with the view that the economy continued to cool into year-end.

ISM's services PMI is due Wednesday, and here the news is expected to be more constructive with a reading of 52.3 expected, a level consistent with expansion.

However, the PMI's employment sub-index could be the more important reading on the day as it will offer fresh evidence of a slowing U.S. labour market, which would encourage traders to raise expectations for more rate cuts at the Federal Reserve.

This would, all else equal, weigh on the dollar.

Also on Wednesday are JOLTS job openings figures, another important indicator of U.S. labour market health, where a slowdown from 7.67M to 7.73M is expected for November.

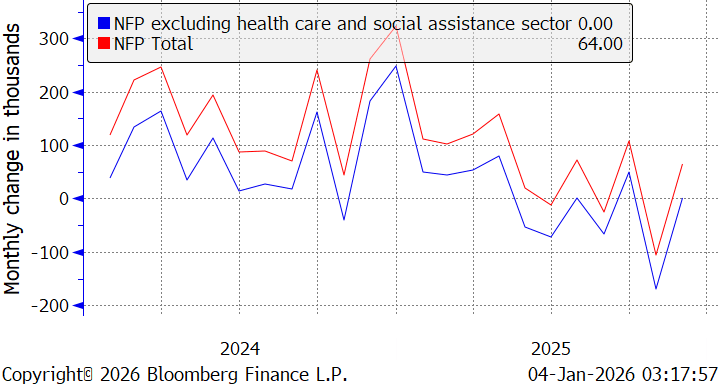

Above: The U.S. labour market is losing momentum, necessitating the need for lower interest rates. This weighs on the USD. Image courtesy of Brown Brothers Harriman.

The big event of the week comes Friday when the non-farm payroll employment report is released. Here, 57K jobs are expected to have been created in December, confirming a steady deceleration (as above chart shows).

Anything less and the dollar falls as Fed rate cut bets ramp up, anything higher and the dollar extends its January recovery.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.