✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

Image © Adobe Images

The euro to dollar exchange rate (EUR/USD) looks set to test 1.14 in the coming days.

The euro looks prone to further weakness against the dollar in the short-term timeframe, and any rebounds will likely be met with renewed selling interest.

As the chart shows, gains are capped by a downward sloping trendline and we won't rule out any small relief rally that brings the market back towards that trendline, in keeping with the pattern of play since mid-September:

Note that the RSI in the lower panel is a subdued 35 which is consistent with a well entrenched downside momentum. Last week saw the exchange rate break below the 100-day exponential moving average (EMA), signalling increasingly entrenched downside momentum.

The downside target we are watching is 1.14, which is a horizontal line of interest that has attracted market action since April, serving as both resistance and support since then.

Most recently, the level arrested the late-July euro-dollar selloff, from which a sharp rebound commenced.

It's interesting to see that 1.14 is also where the 200-day EMA comes in, meaning it truly is a level of interest. If it can be held, then the broader multi-month consolidative phase stays alive and a rebound ensues.

However, a breakdown through here could be the confirmation of the death of the rally that started at 1.04 in late 2024 and peaked at 1.1918 on September 17.

Looking at the week ahead, the onus falls on the dollar to provide the interest.

Last week's European Central Bank decision (ECB) was a non-event, with the central bank resting on its laurels having pushed inflation back to its 2.0% target and seeing little reason to offer guidance that might excite markets.

With the ECB having effectively achieved a rare central bank 'job done', it falls to other central banks to get their economies in order. The U.S. Federal Reserve cut interest rates last week and said it could do so again before year-end, although it won't convincingly commit to such a move.

That non-commital helped the dollar rally in the wake of the Fed's decision, and we're still living with that momentum.

The week ahead would normally be an important one in terms of data as the first Friday of the new month is traditionally set aside for the all-important U.S. jobs report.

But because U.S. politicians appear happy to let the current partial shutdown of U.S. government agencies continue, we won't be receiving any official statistics this week.

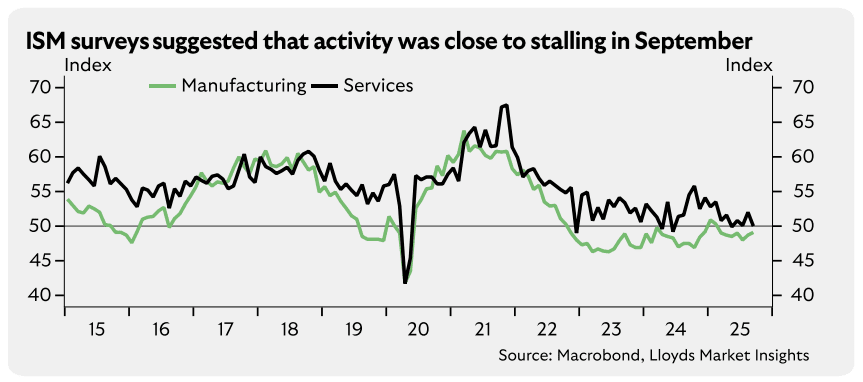

This means private sector reports must assume the mantle. With this in mind, we await the U.S. ISM's PMI surveys of the U.S. economy's private sector in October.

The surveys were indicating the economy was close to stalling in September, and further confirmation of this will likely bolster the odds of further Fed rate cuts, which would hurt the dollar.

However, any signs of a pickup would likely keep the Fed on the sidelines and bolster the dollar.

The manufacturing PMI is due Tuesday (consensus expects 49.2) and the services PMI due on Thursday (the consensus expects 51.0).

"Within the report, particular attention will be paid to employment indicators, which could signal further labour market weakness, and price components, which remain elevated and will be closely watched for signs of moderation," says a preview note from Lloyds Bank.

Any moderation in the data can help EUR/USD arrest its selloff and potentially etch out the contours of a rebound.