✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.

Image © Adobe Images

A key driver of U.S. Dollar weakness remains intact: hedging against USD weakness.

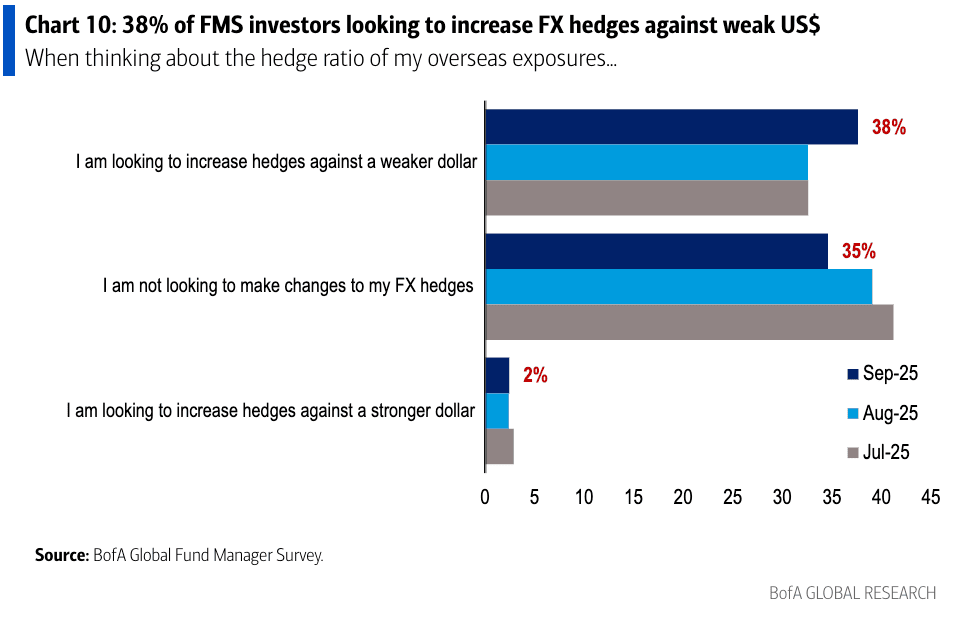

According to a much-watched survey of fund managers from Bank of America, 38% of respondents reported they are looking to increase hedges against a weaker dollar.

This is up from 33% in August and the highest level since Jun 2025.

The findings confirm investors are selling dollars as they engage in trades that provide a hedge against further USD weakness.

Why hedge? A falling dollar means lower returns for foreign investors holding U.S. equities, as the value of repatriated funds declines due to currency movement.

When the dollar was in a multi-year bull run this wasn't a problem; in fact being unhedged increased your returns as the USD value rises against your home currency.

This all changed this year when the U.S. dollar slumped in the face of U.S. President Donald Trump's new agenda on trade and his desire to meddle in U.S. institutions.

The need to hedge against a lower dollar fuels that decline as investors take out the trades that profit on USD weakness to cover for currency-adjusted losses on their portfolios. In short, this hedging behaviour fuels USD weakness and adds impetus to the selloff.

Bank of America's findings tell us investors look to increase hedges, which suggests this source of USD weakness has space to run.

Another interesting takeaway from the survey is that 26% of respondents view a 2nd wave of inflation as the biggest tail risk, followed by 24% saying "Fed loses independence & US dollar debasement" is the biggest tail risk.

Trump's efforts to mould the Fed in his image are well underway, while the Fed is about to cut rates tomorrow, as inflation looks anchored well above 2.0%. This is what the foundations of a debasement are built on.

One problem for euro bulls, however, is that the rotation into European assets appears to have stalled.

The survey finds "the view of EU exceptionalism has been dented, with the EU equity overweight slipping further and the gap to the continued US equity underweight falling to the lowest level since February."

If a rotation into European equities underpinned outright euro support in H1, its demise could imply slower going for euro-dollar in H2.

✳️ Secure today's exchange rate for a future payment. You may also book an order to trigger your purchase when your ideal rate is achieved. Learn more.