Markets have been accused of over-estimating the true value of the euro dollar exchange rate by under-estimating the currency impacts surrounding a Greek exit from the Eurozone.

"The euro to dollar exchange rate conversion (EURUSD) is trading at 1.1405 at the time of publication - it should be lower."

We hear from two leading institutional analysts as to why the euro dollar rate should perhaps be trading lower based on Greece-inspired risks.

The prevailing belief on the markets is that the Euro Zone is in a much better position to withstand a possible Greek departure than it was during the previous threat of a Greek exit back in 2012, when markets feared that a Greek debt default would trigger a wider European financial crisis.

The thinking is that since 2012, many measures have been implemented to strengthen the resilience of the Euro Zone.

These include the creation of a €500 billion rescue fund, the European Central Bank’s (ECB’s) mass purchase of government bonds under its quantitative easing program and economic reforms undertaken by certain Euro Zone countries. European banks have also slashed their exposure to Greece in recent years.

The firebreaks to financial contagion are believed to be in place allowing traders to focus on broader drivers of the exchange rate.

Euro Exchange Rates Should be Lower

The euro to dollar exchange rate conversion (EURUSD) is trading at 1.1405 at the time of publication - it should perhaps be lower suggest two analysts we follow who have looked at market positioning and the geopolitical implications inherent in a Greek exit.

“EUR continues to trade with a firm bias. EUR’s status as a funding currency and an already short market arguably keep the single currency stronger than one would assume in the face of elevated peripheral sovereign risks. But likely weaker prelim June PMIs next week and close proximity of major resistance levels at 1.1390 and 1.1470 suggest the up move is likely to stall very soon,” says Richard Franulovich at Westpac in New York.

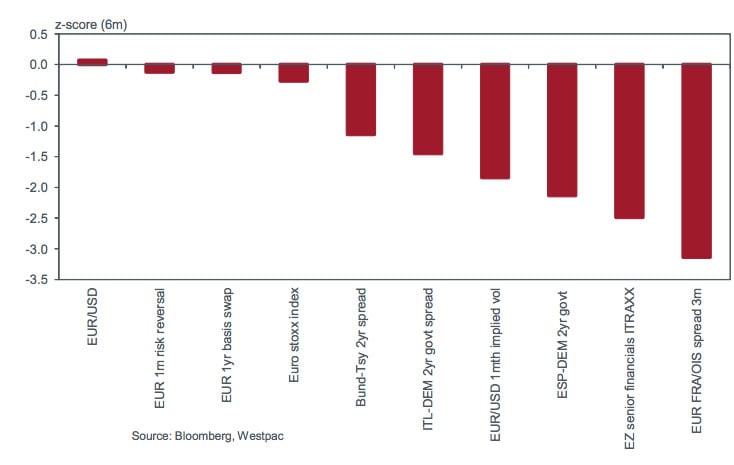

Franulovich suggests markets are mis-pricing the risks of a Greek exit from the Eurozone based on below chart which shows the level of various Eurozone market instruments, measured as a 6mth z-score.

The 3mth EUR FRA/OIS spread, the European senior financials ITRAXX CDS index and the Spanish-bund 2yr sovereign bond spread are all trading at least two SDs from their 6mth trends.

At the other extreme EUR is trading close to +0.1 z-scores from its 6mth trend.

Franulovich explains why this translates into a what should be a lower euro:

“The Euro Stoxx index, the EUR 1yr basis swap and 1mth 25 delta EUR/USD risk reversals look similarly 'complacent' in pricing terms.

“Arguably a simple average of the z-scores across all the instruments represents a reasonable gauge for how much Greek tail risk EUR/USD should be discounting. That would put EUR/USD at 1.06-1.07.

“EUR’s use as a funding currency and a short market have precluded EUR from falling far in response to Greek stress but history suggests it’s just a matter of time.”

A Greek Exit Would Simply be a Disaster for Eurozone (And the Exchange Rate)

Markets are showing a fatigue to Greece and are apparently unconvinced that a Greek financial crisis stemming from Eurozone exit will spread to other Eurozone states.

Despite the building of the already mentioned financial firewalls, “we maintain that the Euro Zone remains economically and politically vulnerable to a potential Greek exit for several reasons,” says Angelo Katsoras from National Bank Financial, a subsidiary of National Bank of Canada.

These reasons forwarded by Katsoras include:

- A Greek exit would signal that Euro Zone membership is not irreversible. The moment another country encountered significant economic difficulties speculation would automatically arise over its status in the Euro Zone.

- The reversible nature of membership would also reduce the value of the promise by the ECB to do “whatever it takes” to maintain the viability of the Euro Zone in any future crisis.

- Loyalty to the Euro Zone by other troubled member states cannot be maintained over the long term via the threat of expulsion as the imposition of austerity would lead to popular discontent.

- The collapse of Greece would mean that Europe would have to worry about yet another quasi-failed state on its periphery. Further, Greece would have no incentive to prevent the wave of refugees arriving on its shores from Africa and the Middle

- A bankrupt Greece would still require financial assistance from the international community in order to avoid a complete slide into financial chaos. This is because the drachma would not immediately be accepted as a form of payment by other countries for such items as food, medicine and energy.

- Taxpayer losses on Greek debts would make it much more difficult to get needed political support for any future bailouts.

Despite the unease the above observations present with regards to current valuations of the euro we must be aware that in the near-term the euro holds the upper hand and could well push the euro dollar exchange rate to its 2015 best as markets ascribe more importance to interest rate policy at the US Federal Reserve.

Those watching the market should however be wary that should geopolitical events surrounding Greece spiral and grab attention away from the US Fed then hefty falls could well be in store.