Image © Adobe Images

A short-term rebound is likely if political anxieties take a backseat now that Starmer has gone.

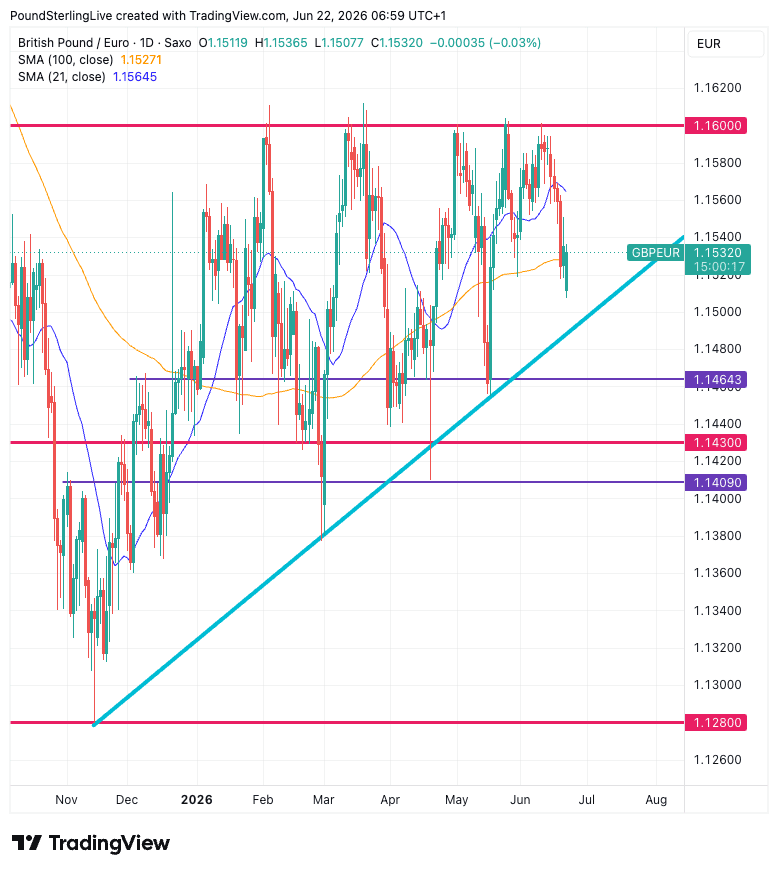

A recent failure by the pound-to-euro rate to sustain gains above 1.1580 suggests bullish momentum has faded in the near term, although the broader uptrend remains intact for now.

Last week saw the pair slide half a per cent in sympathy with a broader GBP decline that leaves it the third-biggest loser in G10 when screened over a one-week timeframe.

The key battle for the exchange rate this week will see buyers trying to defend the 100-day moving average at 1.1527, and a successful defence would keep the broader range intact and favour renewed attempts on 1.1600 later in the summer.

However, a break below 1.1527 would increase the likelihood of a move towards trendline support near 1.1500 and potentially the major support level at 1.1464.

The moving averages are sending mixed signals: the 21-day moving average has rolled over and now sits above spot at 1.1565, indicating short-term momentum has turned negative.

However, the 100-day moving average continues to rise beneath the market near 1.1527 and remains above the rising post-November trendline, indicating a medium-term structure that's still constructive despite the recent setback.

It will be difficult to hold the pound in a positive light this week, given that the country has lost yet another Prime Minister, with Keir Starmer resigning his position mid-morning.

We now face a period of waiting as it won't be until September when Andy Burnham is set to take over the leadership role.

As we note in today's leader, that means weeks of uncertainty that will almost certainly weigh on the Pound.

However, near-term, there are no immediate risks on the political front, given Burnham won't want to scare the market with any policy insights. In fact, by all accounts, he will spend the next few weeks coming up with some new policies. So we'd expect any GBP weakness associated with the new PM to be loaded towards the weeks leading up to his coronation.

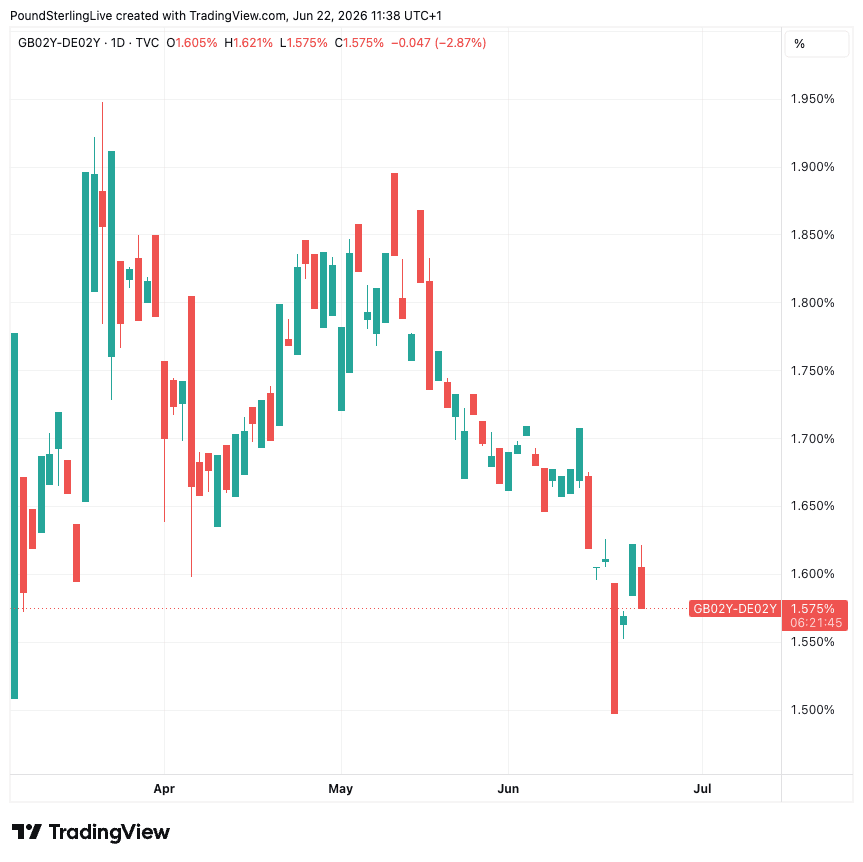

The fading of immediate political concerns should leave the pound free to reconnect with yield differentials, which are, for the most part, supportive of the pound.

The UK-German two-year spread dropped notably last week thanks to a soft inflation print and the Bank of England's decision to keep rates unchanged.

It is likely that the drop was more a function of falling global oil prices as the U.S. and Iran move toward a peace deal. That signals global inflationary pressures should settle, and for the UK, which has suffered an inflation premium for some time now, that's particularly welcoming.

That pullback in inflation expectations is reflected in lower short-term yields, which translates into a softer pound.

If the recent adjustment ends, the pound can find itself better supported. Indeed, oil prices have been contained near $80 a barrel since late last week, which could offer some stability for UK bond yields, and that would in turn support sterling.

Negotiations between the U.S. and Iran are underway in Switzerland, and caution about any setbacks should keep the market in check.

Datawise, only EU and UK PMI data for June is on offer, and any surprises either side of the expectation line could trigger volatility.

The eurozone composite PMI is expected to read at 49.1, up from 48.5.

Britain's print is forecast to read at 50.6, up from 49.7.