Image © European Commission Audiovisual Services

The Euro will fall against the Dollar as the European Central Bank (ECB) engages a faster and deeper interest rate cutting cycle to plug a yawning output gap in the Eurozone, according to Morgan Stanley.

"EUR has room to correct lower on a faster and deeper cutting cycle," says David S. Adams, a strategist at Morgan Stanley, in a view that counters the consensus belief that the Euro is destined higher against the Dollar over 2024 and 2025.

The call comes at a time of relative calm in FX, with the Euro to Dollar exchange rate trading in a relatively tight range in the 1.07-1.09 region amidst a drop in global FX volatility.

Many analysts agree that this results from market expectations for the major central banks to cut interest rates at around the same time, starting in June. This means there is little differentiation in short-term interest rate expectations to drive meaningful trends in exchange rates.

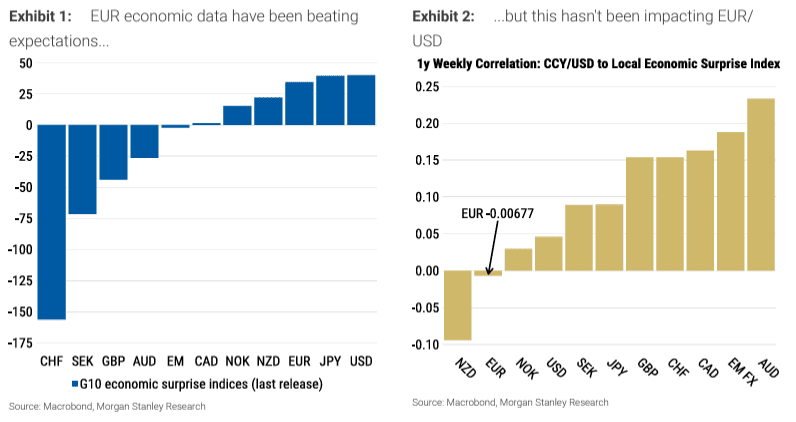

This reminds us that interest rate expectations remain a key driver of FX, and the problem for those wanting volatility is that rate expectations for global central banks have simply been tracking the U.S. Federal Reserve in 2024, resulting in limited movements.

Strategists at Morgan Stanley say the market will continue to price a strong relationship between the timing of the first cut across central banks, which can keep the Euro-Dollar exchange rate steady in the first half of 2023.

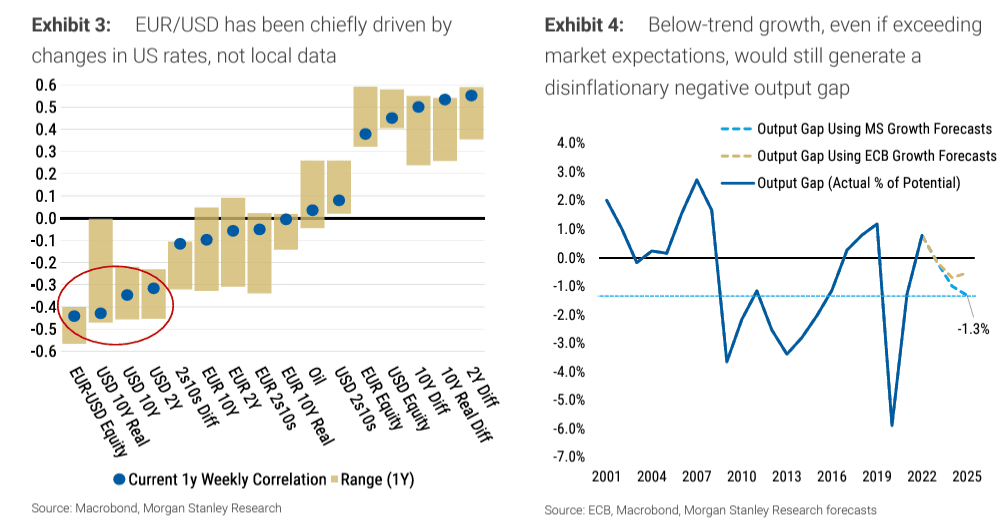

But, once rate cuts begin, the prospect of meaningful movement in FX markets grows, and here the Euro looks vulnerable as the Eurozone is growing well below its potential, meaning ECB interest rates will need to be reset lower.

"A negative output gap implies reduced demand-driven inflation and creates risks that the market will price in not just a terminal rate at neutral but perhaps even below. Such a rapid cutting cycle suggests a lower EUR/USD spot, higher volatility and lower EUR carry, all of which render EUR a more attractive funding currency," says Adams.

Image courtesy of Morgan Stanley.

Adams says he hears the argument that Eurozone growth surprises are likely to pick up from a low base, prompting a potential rise in the Euro. However, he argues that "by focusing on data surprises, investors are missing the point: the level of data, specifically growth, matters".

"Persistently weak growth could generate a negative output gap which would amplify disinflation and raise the probability that the ECB would have to cut rates not just to neutral but even below," he explains.

As a result, he recommends staying short EUR/USD via options: "EUR/USD downside remains an attractive, positive carry hedge for a variety of macro scenarios, including a more dovish pricing for the ECB's cutting path. We continue to recommend buying 1-year EUR/USD puts at 1.07."

Image courtesy of Morgan Stanley.

Why Morgan Stanley Sees An Output Gap Problem

Using the potential growth forecasts from the European Commission, Morgan Stanley estimates what the output gap could look like using realised 2023 growth figures and both its own economists' growth forecasts and the ECB's forecasts from the December meeting.

The Commission estimates that potential growth in the euro area is roughly 1.3-1.4% y/y.

The near recessionary growth rates in 2023 turned the output gap from positive to negative in 2023. Continued below-trend growth rates in 2024 and 2025 lead, based on Morgan Stanley's economics team's numbers, the output gap to reach -1.3% of GDP by end-2025.

"This would be a negative output gap close to levels last seen in the aftermath of the eurozone debt crisis from 2010-15 if we exclude the Covid period. Even using the ECB's arguably optimistic growth forecasts, we still estimate a modestly negative output gap of -0.5% of GDP," says Adams.

Central banks often use a potential output measurement to gauge inflation and typically define it as the level of output consistent with no pressure for prices to rise or fall.

Where output is above potential, inflationary conditions persist, but if actual output falls below potential output over time, prices will begin to fall to reflect weak demand.

In this instance, the ECB will have to cut interest rates to close the negative output gap generated by the Eurozone's economy.