Written by Raffi Boyadjian, Lead Investment Analyst at XM.com. An original version of this article can be read here.

The selloff in bond markets is showing no sign of easing as investors are dumping government securities in favour of cash amid expectations that interest rates in the US may yet rise further.

Despite the tightening cycle nearing its end, the hawkish drumbeat from the Fed has only gotten louder, unnerving investors who were betting on rate cuts as early as in the spring of 2024.

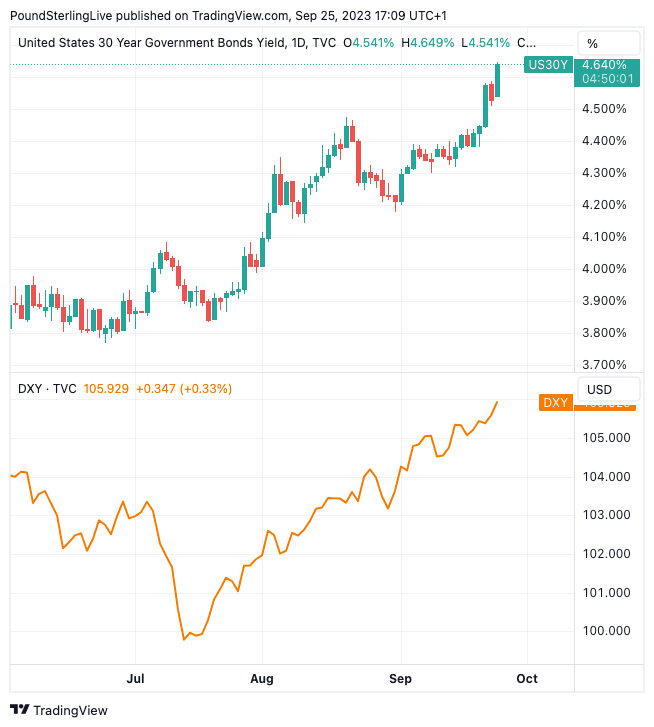

The yield on 10-year Treasury notes broke above 4.50% on Monday for the first time since November 2007 and continues to climb to fresh highs today.

The 30-year yield, meanwhile, has surged to 12½-year highs as long-term rates adjust to the Fed’s “higher for longer” mantra.

Above: U.S. 30-year bond yields pulling the Dollar index higher alongside.

Minneapolis Fed President Neel Kashkari hinted on Monday that “rates probably have to go a little bit higher” if the US economy stays fundamentally resilient, while Chicago Fed chief Austan Goolsbee reiterated that rates will have to stay high for longer than what markers had anticipated.

The odds of one final 25-basis-point hike now stand at 50%, up from 40% prior to last week’s FOMC decision. However, there’s been no notable scaling back of rate cut expectations over the past week, suggesting that there’s room for further repricing should inflation remain stubbornly high.

There’s no stopping the dollar

The next update on the inflation front will be Friday’s core PCE price index, which had edged up in July. If the Fed’s favourite price gauge falls to 3.9% in August as forecast, the rally in bond yields might pause for breath, halting the US dollar’s advance.

In the meantime, though, there’s no stopping the greenback as the dollar index is back above 106.0, reaching the highest since late November. What’s striking is that long-term bond yields have jumped across the board, with the exception of UK gilt yields, yet only the dollar stands tall.

The worsening economic data in Europe, China’s never-ending property crisis and the surprise rally in oil prices has dampened the prospects for most other major currencies.

Even if the likes of the ECB and Bank of England are not about to cut rates anytime soon, the US economic outlook is far stronger at the moment. Moreover, a gloomy picture globally tends to draw safe haven bids for the dollar, thus there could be more gains in store in the near-to-medium term.

This can only be bad news for the euro and pound, which have slipped below the key levels of $1.06 and $1.22, respectively, over the past day.

Yen dangerously close to intervention level

The yen is also under increasing strain as the Bank of Japan has set the bar high for warranting an exit from ultra-accommodative policy.

There had been some hopes that the BoJ would soon begin laying the groundwork for an eventual exit but Governor Ueda’s dovish remarks in recent days suggest the timing remains a long way off.

That has left the yen extremely vulnerable in a landscape where there is renewed dollar upside. The greenback briefly spiked above 149 yen earlier today before easing back.

The last time the yen approached the 150 level a year ago, Japanese officials had stepped up their verbal warnings before going ahead and intervening in the FX market to shore up the currency. But verbal intervention has been unusually scarce this time around, which may be an indication that the threshold has shifted somewhat.

Update: Yen Recovers on Suzuki's Intervention Threats