![]()

Image © Adobe Images

The Euro could be set to bounce against the Dollar and rise over the coming weeks, however, those wanting a strong Euro should be agile as the rally is expected to be short-term in nature.

This is according to an analysis from Danske Bank issued as the third quarter draws to an end and market participants ponder if the Dollar's robust rebound has the legs to extend into year-end.

The message from Danske Bank analyst Kirstine Kundby Nielsen is that the Euro can stage a rebound as investors welcome a peak pessimism moment with regard to China's economy and the Eurozone's manufacturing sector.

"We maintain our strategic case for a lower EUR/USD based on relative terms of trade, real rates and relative unit labour costs However, in the near term, we see some potential for topside risk to the cross on the back of peak policy rates, an improving manufacturing sector backdrop relative to the service sector, and/or easing China pessimism," says Nielsen.

The call comes as the Euro to Dollar exchange rate (EURUSD) extends a losing streak that has seen it lose approximately 5.80% of its value since it peaked at 1.1275 on July 18.

A marked slowdown in the Eurozone economy - particularly the manufacturing sector - as well as disappointing Chinese data releases have all conspired against the Euro.

At the same time, the U.S. economy has printed a string of above-consensus economic data releases that come alongside falling inflation, suggesting the Fed might be able to get inflation back to target without creating a serious downturn.

But for the Euro selloff to extend, news out of the Eurozone and China must turn progressively worse, or data out of the U.S. must progressively improve.

Is this possible? Danske Bank's strategists think peak pessimism on both China and Eurozone can prove supportive.

Indeed, data out Monday showed Germany's Ifo business climate index held steady in September at the previous month's level despite expectations of further deterioration.

The business climate indicator fell from 85.8 to 85.7, better than the expected 85.1. Chinese PMIs have meanwhile shown a bottoming in activity with other surveys and official data also pointing to improvement and bolstering the outlook.

"Peak policy rates, an improving manufacturing sector relative to the service sector, and/or easing China pessimism could add some support to EUR/USD in the near-term," says Nielsen.

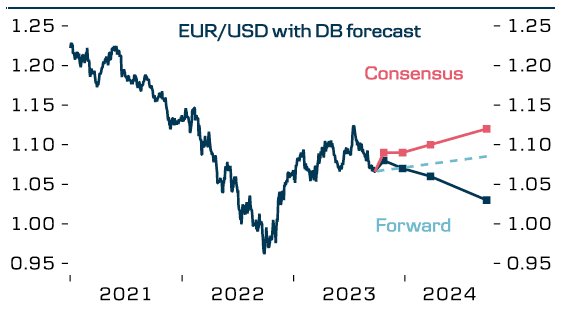

Above image courtesy of Danske Bank.

Danske Bank's base case assumption is that both the Federal Reserve and European Central Bank have completed their respective rate hiking cycles and that focus will now turn to the question of rate cuts.

Given relative assumptions about the state of the U.S. and Eurozone economies and how the rate cut cycle can proceed, Danske Bank maintains a forecast for a lower Euro-Dollar "based on relative terms of trade, real rates (growth prospects) and relative unit labour costs."

The bank targets 1.03 on a 12-month timeframe, but sees a return to 1.08 over one month in line with expectations for a near-term rebund.

After three months the target forecast is set at 1.07, ahead of a fall to 1.08 in six months and finally that one-year target of 1.03.