- EUR/USD drawing dip buyers near & below 1.05

- But could struggle to get above 1.06 in short-term

- As energy woes complicate ECB’s policy outlook

- European data, USD trend, ECB speeches eyed

Above: Lady Justice statue, Frankfurt © Adobe Images

The Euro to Dollar exchange rate has held above the recently reclaimed 1.05 level but with the European economic outlook seemingly darkening it could now struggle to advance much beyond 1.06 without a further retreat by the U.S. Dollar, which appeared to falter in its step last week.

Europe’s single currency has drawn bids from the market whenever near or below 1.05 but its buoyancy above that level has been aided significantly by a softening Dollar and widespread gains for stocks and bonds that many analysts have attributed to investor concerns about the global economy.

This was after Federal Reserve Chairman Jerome Powell reiterated in Congress last week that it will be difficult for the Fed to bring down U.S. inflation without disrupting the labour market or harming the economy, which prompted a downward revision to market expectations for U.S. interest rates.

“The positive story seems to be that Fed Chair Powell's admission last week of the risk of recession means that global monetary tightening may not be as sharp as expected - and that's good news for equities,” says Chris Turner, global head of markets and regional head of research for UK & CEE at ING.

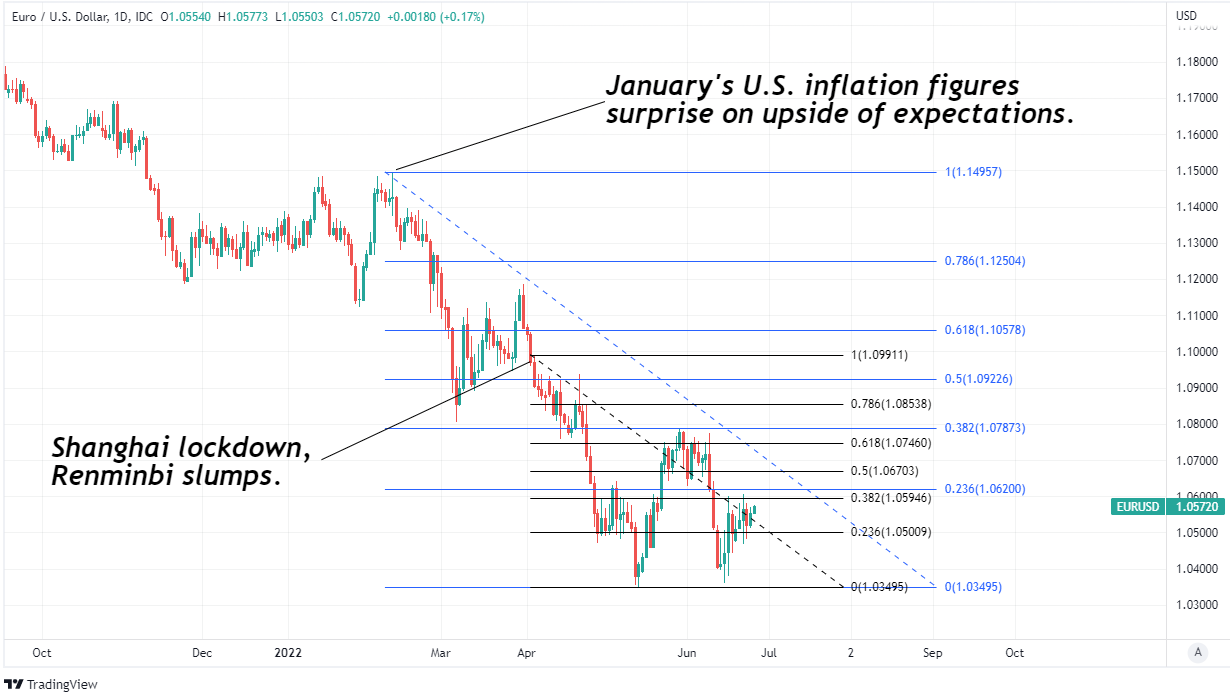

Above: Euro to Dollar rate shown at daily intervals with Fibonacci retracements of February and April falls indicating short-term areas of technical resistance for Euro. Click image for closer inspection.

Above: Euro to Dollar rate shown at daily intervals with Fibonacci retracements of February and April falls indicating short-term areas of technical resistance for Euro. Click image for closer inspection.

“Current price action is in keeping with our baseline scenario of EUR/USD trading in a range through the summer months before making a modest turn higher at year-end should, as we believe, the market shift towards pricing the start of a Fed easing cycle in late 2023. For the time being, however, the Fed will continue to sound hawkish and EUR/USD may struggle to hold gains over the 1.0625/40 area this week,” Turner and colleagues said on Monday.

For the Euro the revision to expectations for Fed policy and Dollar’s declines offset an even larger fall in expectations for European Central Bank interest rates following last Thursday’s S&P Global PMI surveys, which warned of a darkening outlook for core industries of Europe’s economy.

The decline in Europe’s PMI surveys has reversed much of their recovery from the winter’s ‘lockdown’ induced losses and came at a point when the continent’s largest economy, Germany, is facing increased risks associated with falling gas supplies from Russia.

“The final stage of Germany’s plan would involve rationing gas supplies which would have a much more direct impact on economic activity. With Nord Stream flows set to be further impacted by a regular annual maintenance shutdown, moving to Stage 3 seems more likely than not,” says Derek Halpenny, head of research, global markets EMEA and international securities at MUFG.

Above: Euro to Dollar rate shown at daily intervals with Fibonacci retracements of February and April falls indicating short-term areas of technical resistance for Euro. Click image for closer inspection.

Above: Euro to Dollar rate shown at daily intervals with Fibonacci retracements of February and April falls indicating short-term areas of technical resistance for Euro. Click image for closer inspection.

“That could have implications for the outlook for ECB monetary tightening. Currently, close to 160bps of tightening is priced for this year. This is excessive but so is the 185bps priced in the US. Ultimately, it seems more likely than not that the Fed will have paused before year-end but a specific energy shock through natural gas prices spiking could unfold sooner and could be the catalyst for a new leg lower in EUR/USD,” Halpenny adds.

The big risk for the Euro is that the economic hit associated with high energy prices and possible disruptions of supplies begins to be viewed at the European Central Bank (ECB) as a medium-term source of disinflation and so also a reason for a slower or more cautious approach to the normalisation of its monetary policy that has been priced-in over recent months.

This is one scenario the market will likely have in mind on Monday and Wednesday when President Christine Lagarde delivers opening remarks and later participates in a panel discussion at the ECB’s Forum on Central Banking in Sintra, Portugal, while many in the market will also be listening for any clues about the likely design of a tool the bank intends to use to prevent Southern European bond markets from coming undone as its interest rates rise.

“More recently, the increasingly hawkish ECB policy stance has offered some respite and arrested the (seemingly terminal) decline of EUR/USD. That being said, FX investors also worry about the limits of the ECB support for the EUR given that the bank’s hawkishness increased the risk of fragmentation in the EGB [European Government Bond] market,” says Valentin Marinov, head of G10 FX strategy at Credit Agricole CIB.

Above: Euro to Dollar rate shown at weekly intervals with Fibonacci retracements of 2017 recovery indicating medium-term areas of technical support for Euro. Click image for closer inspection.

“More evidence that the ECB is committed to containing the Eurozone inflation while shielding the EGB market, can boost the EUR’s safe-haven appeal and prop up EUR/USD at a time when growing recession fears remain the main FX market driver,” Marinov said on Monday.

Monday and Wednesday appearances by President Lagarde are the highlight of the week for the Euro but Spanish and German inflation date out on Tuesday will also be important and so too will this Thursday’s German retail sales figures and Friday’s overall Eurozone inflation data.

Thursday’s retail sales data will offer important insight into how the consumer side of Europe’s largest economy is faring amid the commodity price shock but equally important will be whether the Eurozone inflation rate continued its recent ascent in June.

Germany’s retail sales already fell by -5.4% in April while Europe’s inflation rate rose from 7.5% to 8.1% in May and from 3.5% to 3.8% when energy and food items were excluded from the basket under the microscope.

“Another upside surprise would place more pressure on the ECB to tighten policy even as growth slows,” says MUFG’s Halpenny.