© Christian Müller, Adobe Stock

- EUR support fades even after inflation surprises on upside.

- 'Base effects' and oil price movements lift EUR CPI in Nov.

- But does not change outlook for prices, ECB policy or EUR.

- Comes ahead of important German SPD leadership vote.

- Candidates in SPD ballot could sink German Gov coalition.

- Also comes ahead of U.S. response to French digital tax.

- EUR tests below 1.10, risks sustained break says MUFG.

The Euro retreated toward its range-lows Friday even after November flash inflation figures surprised on the upside, because the data doesn't change a downbeat European Central Bank (ECB) interest rate outlook and the single currency faces German political risk as well as a U.S. tariff threat next week.

Eurozone inflation was 1% in November, up from 0.7% previously and far ahead of the 0.8% consensus expectation. Core inflation, which is seen by policymakers as a more reliable measure of domestically generated price trends, rose from 1.1% to 1.3% when markets were looking for only 1.2%.

The core number ignores prices of energy items that are influenced mostly by movements on international markets, as well as goods that have regulated prices like alcohol and tobacco. Movements in core inflation generally tend to garner more of a market response than changes in the headline number.

“The EZ CPI data are coming in “hot" just as Lagarde prepares to oversee her first official meeting as ECB president next month. Arguably, this is the highest core print in this cycle excluding Easter distortions,” says Claus Vistesen, chief Eurozone economist at Pantheon Macroeconomics. “We suspect the core rate will dip a bit in the next few months, but a gradual increase is consistent with the trend in the labour market and wage growth, indicating that core inflation will rise to just under 1.5% towards the end of next year.”

Markets care about inflation statistics because central banks are obliged to use interest rate policy to keep price growth contained within preset parameters. The ECB's target is to ensure the consumer price index averages “close to, but below 2%” over the medium-term, but inflation is sensitive to growth which means the pulse of the economy is important to the outlook.

Europe’s economy has been further wounded this year by the ongoing U.S.-China trade war, entrenched uncertainty over the final Brexit outcome and problems in the domestic automotive sector among other things. Growth forecasts suggest, across the board, a moribund year ahead for the Eurozone and the ECB has already cut one of its interest rates further below zero and restarted its quantitative easing program in the hope of lifting growth and inflation over the coming years.

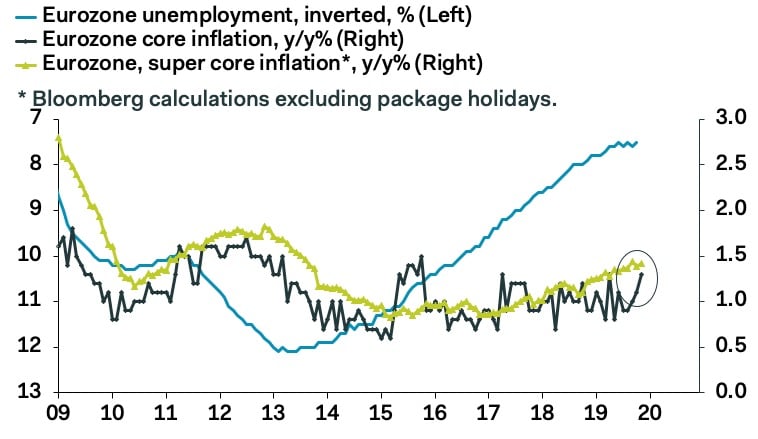

“The chart shows that the EZ core is suddenly zooming higher, though at this point it is difficult to say whether it is the beginning of a break-out or just normal volatility around a stable trend of around 1%. The super-core rate is slowly trending higher, in line with falling unemployment, but it is still far away from the ECB’s target,” says Pantheon’s Vistesen.

Above: Pantheon Macroeconomics graph showing inverted Eurozone unemployment rate alongside core inflation.

Separately, the Eurozone unemployment rate was revealed on Friday to have declined to 7.5% in October, from an upwardly-revised 7.6% in September. However, the jobless figure is still more than twice the 3.6% prevailing in the U.S. and is almost double the 3.8% rate of the Brexiting UK economy.

In short, the Eurozone labour markets and economies remain too weak to produce the price pressures necessary for the ECB to be able to stop leaning on negative interest rate and quantitative easing policies. Those low interest rates have made the Euro cheap to borrow and a prime candidate for short-selling, with investors often now using it to ‘fund’ bets on higher yielding currencies in both the developed as well as emerging worlds.

“We more likely face a traditional grind lower as this negative yielding asset acts as the mirror to enthusiasm for the comparatively high yielding USD. The ECB’s chief economist recently expressed a willingness to cut rates further if necessary and also indicated that the ECB is about to launch a review of its policy framework given the failure to get inflation back close to target. With fiscal policy not stepping up, the pressure on monetary policy will remain acute and so the rhetoric is likely to remain resolutely dovish,” says David Bloom, head of FX research at HSBC. “The pace of EUR decline may be subdued in part because few fresh policy initiatives are likely after the cocktail of measures announced in September. In addition, while economic activity is not recovering, at least things are getting worse less quickly than before.”

The brighter pastures of North America are a big problem for the EUR/USD rate and with the U.S. economy again showing its resilience this week, the single currency is set to remain under pressure from a wide interest rate differential as markets give up hope of seeing the Federal Reserve (Fed) cut U.S. borrowing costs any further than it already has done.

Above: Euro-to-Dollar rate shown at 4-hour intervals.

“Foreigners are long of longer-dated euro-denominated assets, mostly (but not all) hedged on a shorter term basis. By contrast, for European (or Japanese) investors, the flat US curve means that, say, hedging a 10year treasury with a 1-year FX forward eats up all the yield advantage of buying Treasuries in the first place,” says Kit Juckes, chief FX strategist at Societe Generale. “The dollar remains underpinned, the euro languishes, and the market's focus remains on US/Chinese trade talks, the slowing Chinese economy, political uncertainty in Latin American (linked to slower Chinese growth at some point), the next Riksbank meeting and UK elections."

Investors had traditionally sold Dollars simultaneously alongside their U.S. bond purchases, to protect themselves against weakness in the greenback, but the Fed’s 1.75% interest rate now discourages them from doing that and is lending support to the greenback. Meanwhile, investors are selling Euros when buying continental assets in order to protect themselves against further declines. That 'hedging' practice is itself helping to keep the Euro under pressure.

“One potential trigger which could encourage further euro selling at the start of next week is more investor concern over political instability in Germany,” says Lee Hardman, a currency analyst at MUFG. “The SPD are currently polling neck and neck with the right-wing AfD party on around 14-15%....They continue to lose support remaining part of the coalition government, but they would lose power and risk losing seats if they withdraw from the government and it eventually results in an early election.”

Friday’s inflation figures come as markets await the outcome of the Social Democratic Party (SDP) leadership election in Germany, which will be important in determining whether Chancellor Angela Merkel’s coalition can continue to govern. The Klara Geywitz and Olaf Scholz leadership duo prefer the status quo of the current coalition while the Saskia Esken and Norbert Walter-Borjans duo want radical reform of current arrangements.

Above: Euro-to-Dollar rate shown at daily intervals.

Victory for the latter might see markets fear fresh political instability in Europe’s largest economy, which narrowly dodged a technical recession last quarter. Such an outcome might not be welcomed by the Euro next week, which will also bring a U.S. response to France’s controversial digital services tax (DST).

The Office of the U.S. Trade Representative said this week it will publish on Tuesday, its assessment of the French DST alongside notice of any retaliatory actions to be taken. The White House has previously threatened to impose trade tariffs on imports of goods from Europe in response to the French levy, which the U.S. suggests is in defiance of agreements on dual taxation. It's just the latest in a long line of U.S.-EU trade differences, although an all-out tit-for-tat tariff fight has so-far been avoided.

“The euro continues to trade heavy with EUR/USD testing support at the 1.1000-level for the second time this month. The current low level of volatility and improvement in global investor risk sentiment has created a less favourable environment for low yielding funding currencies such as the euro. One-week implied EUR/USD volatility has fallen to a new record low. Our carry attractiveness index is sending a clear signal that EUR/USD could break below the 1.1000-level,” MUFG's Hardman says.

The Euro spiked briefly in response to Friday's inflation figures but succumbed to fresh selling pressures soon after and has since dipped below the key 1.10 support level.

Time to move your money? The Global Reach Best Exchange Rate Guarantee offers you competitive rates and maximises your currency transfer. Global Reach can offer great rates, tailored transfers, and market insight to help you choose the best times for you to trade. Speaking to a currency specialist helps you to capitalise on positive market shifts and make the most of your money. Find out more here.

* Advertisement