- No Reason to Support the Euro at Present say Commerzbank

- ECB's Praet confirms softer data is not going unnoticed

- Outlook suggests short-term pains, longer-term gains for the Euro

ECB chief economist Peter Praet © European Central Bank

Doubts about the Euro's ability to fend off the Dollar are growing, and expectations for a softer single-currency could just allow an under-fire British Pound a reprieve, in the short-term at least.

We are seeing signs that one of the engines of the Euro's 2017 appreciation - the European Central Bank - might not be able to offer the currency any substantial support over coming weeks, and short-term pressures might therefore remain elevated. And, a more hesitant ECB is of course the by-product of indications that the Eurozone might have seen its economic growth peak.

The European Central Bank's chief economist Peter Praet, during the keynote speech at the OECD Chief Economist Talks in Paris, was noted as saying that the recent data points to moderation of Eurozone economy and inflation developments remain subdued.

"Ample degree of monetary stimulus remains necessary," says Praet, adding "we must be patient, persistent and prudent in our monetary policy."

This doesn't sound like a central banker gearing markets for a tightening in monetary policy, rather it sounds like the ECB's gargantuan balance sheet will continue expanding.

A key foundation of the Euro exchange rate's rally through 2017 was the expectation that the ECB would step back from its aggressive monetary stimulus programme in 2018, with a view to raising rates in 2019 as inflation rises to 2.0% thanks to a growing economy.

All signs are however that this withdrawal of stimulus might be delayed as inflation is not heading in the right direction; and we can therefore expect the Euro to retrace some of its gains with the Dollar and Pound potentially benefiting.

Inflation numbers for April disappointed with core inflation reading at 0.7%, below forecasts for 0.9%. Headline inflation reads at 1.2% in April, down from 1.3% in March.

"The ECB's argument of 'solid growth and thus medium term price increases' is crumbling slightly" says Antje Praefcke at Commerzbank, "the Q1 GDP data for the euro zone illustrated that growth momentum is easing slightly. And today’s inflation data for April is unlikely to constitute a valid argument supporting the Euro bulls either."

And, there are wider reasons for the Commerzbank strategist to maintain a cool position on the Euro:

"The disagreements surrounding the EU budget on the other hand make it clear to us that there are still major differences within the EU, and that the europhoria following the election of President Emmanuel Macron was exaggerated. In other words: I see no convincing reasons supporting the euro at present," says Praefcke.

However, other analysts think the ECB will see through this temporary inflation dip and focus on the trend in the underlying inflation pressures and whether core inflation rebounds above 1.0% in May.

So we are seeing here a picture of potential near-term weakness and longer-term strength for the Euro.

"We believe the prospect of higher policy rates in Europe argues for a stronger EUR medium-term, though short-term consolidation could continue until a clear catalyst emerges," says a note from the foreign exchange strategy team at Standard Chartered.

Standard Chartered point out that the Euro has other things going for it, other than ECB policy. "Over the past year, the significant improvement in Euro area current account surplus, coupled with reduced capital outflows, has been EUR positive," say Standard Chartered.

But, going forward, Standard Chartered believe the most prominent EUR supportive catalyst is likely to be ECB communication regarding a potential interest rate hike, which they believe is likely to take place earlier than current market expectations of around Q2 2019.

"Although recent Euro area economic data has been less inspiring, we believe only a marked deterioration from here would force the ECB to revisit its intent to taper quantitative easing," say Standard Chartered.

At the time of writing the Pound-to-Euro exchange rate is quoted at 1.1330, the Euro-to-Pound rate at 0.8827, the Euro-to-Dollar rate at 1.1983.

Concerning the outlook for Sterling, we can report that there are still some bulls out there, despite the recent rundown in the currency owing to softer-than-forecast data.

“The data surprises in the U.K. are at the lows and for this to continue you’d have to expect a severe economic slowdown,” says Jordan Rochester, an analyst with Nomura in London, adding stronger data was needed in coming months to confirm his view that the Bank of England is on course for an August interest-rate hike. For the Pound, “the best is yet to come.”

Nomura have made a strategic recommendation to buy the Pound against the Dollar.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.

Peak Eurozone Growth Might Have Passed

The most up-to-date data coming out of the Eurozone confirms a growing narrative - that the growth spurt of 2016-2017 might be fading.

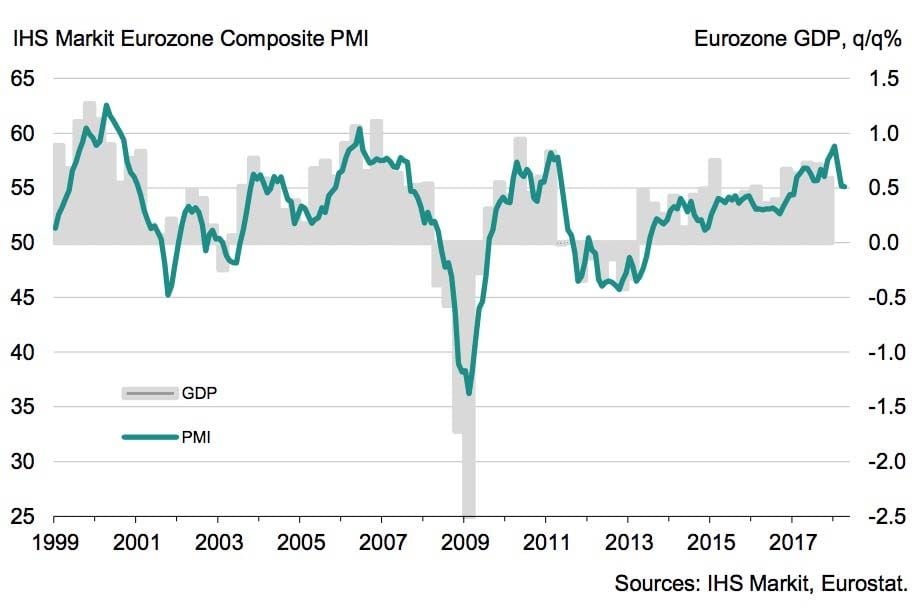

IHS Markit's Composite PMI for the Eurozone fell to 55.1 in April from 55.2 in March, coming in below the forecast and initial estimate of 55.2.

Above: Eurozone growth rates are starting to fade

According to an analysis of the data by Pantheon Macroeconomics, the details contained in the IHS Markit PMI report were underwhelming with the main downside surprises came from Italy and Germany.

The Italian composite PMI slid to a 14-month low of 52.9, from 53.5 in March, due to weakness in manufacturing and because services failed to rebound from its March decline.

In Germany, the composite fell more than initially estimated, to 54.6 from 55.1, because of a downward adjustment to the services PMI.

Elsewhere, the Spanish PMI fell only marginally, by 0.4 points to 55.8, while the French composite index was confirmed at 56.9 in line with the first estimate.

"The details suggest that growth remains robust, but that momentum is falling due to slower growth in new orders. That said, employment and work backlogs are still rising. Input and output prices are still rising, but less so than at the end of last year," say Pantheon Macroeconomics. "The chart shows that the EZ PMIs have declined significantly in recent months, but the swoon isn’t extraordinary in the context of the overall trend since 2012."

"The headline indices also still signal robust GDP growth. That said, markets care more about the direction than the level, and further weakness in coming months would fuel speculation that the ECB will backtrack on its plan to end QE later this year, let alone begin to raise rates next year," add Pantheon Macroeconomics.

Advertisement

Get up to 5% more foreign exchange by using a specialist provider to get closer to the real market rate and avoid the gaping spreads charged by your bank when providing currency. Learn more here.