Pound Sterling trades weeker at the start of the new week being seen in the red against the majority of major currencies.

However, our short-term technical analysis concerning the outlook for the Pound to Euro exchange rate is positive based on recent momentum so we would say there is still the prospect of a bounce.

Ahead of the new week we noted that a series of 'higher highs' and 'higher lows' are unfolding on the four-hour chart; this is typically indicative of the beginning of a new uptrend:

The peaks and troughs are established and support a continuation higher.

Note that the four-hour chart covers the short-term so we are looking at potential direction covering a matter of days and readers should be aware that the longer-term picture suggests Pound Sterling remains under notable pressure.

So when we suggest strength is likely it must be kept in context that this strength is likely to represent a rise within a much larger downmove. Yet, such moments of strength are important for those with international payments.

A break above the current highs would normally be enough to confirm a continuation of the trend but the occurrence of the S1 monthly pivot at 1.1543 is likely to act as a formidable obstacle to further upside.

Monthly pivots are based on the previous month’s range and act as levels of support and resistance where experienced traders often fade the dominant trend.

For confirmation the exchange rate has ‘vaulted clear’ of the S1 pivot, therefore, we would be looking for a break above 1.1570 with our initial target set at 1.1650.

The MACD indicator has moved above the zero-line further supporting a bullish technical outlook for the pair.

Brexit Gets Real

A potential reason for Sterling's soft start to the new week is the UK government's announcement on Monday March 20 that it will trigger Article 50 on 29 March.

This will start a two-year process for the UK to negotiate its future relationship with the EU.

European Council President Donald Tusk meanwhile announced that he will present the draft Brexit guidelines to the EU member states within 48 hours of the UK triggering Article 50.

However, a detailed stance will probably take longer to formulate and real negotiations may not start until June.

"Recent statements on both the UK and EU side suggest both camps are taking a tough line, which is logical at the start of any negotiation process," notes Nick Kounis at ABN Amro in Amsterdam.

Prime Minister May has said the UK will not be part of the single market or customs union as she seems to want to start from a blank page so she does not need to negotiate under the current rules.

At the same time the EU has said they do not want the UK to ‘cherry pick’ the benefits of memberships, while getting rid of the responsibilities.

In particular, the EU insists that full access to the EU market is only possible with full freedom of labour.

"Our base case is that some balance between free trade, free movement and payments into the EU budget will be eventually agreed, though the outcome is obviously highly uncertain," says Kounis.

Sterling Rally Built on Sand?

The Pound rallied following the Bank of England’s (BOE) last meeting because the market had not expected such widespread optimism amongst officials.

BOE’s Kirsten Forbes, for example, voted for a rate hike and other officials voiced similar thought’s judging from the minutes.

“Other members noted that it would take relatively little further upside news on the prospects for activity or inflation for them to consider that a more immediate reduction in policy support might be warranted,” said the meeting minutes.

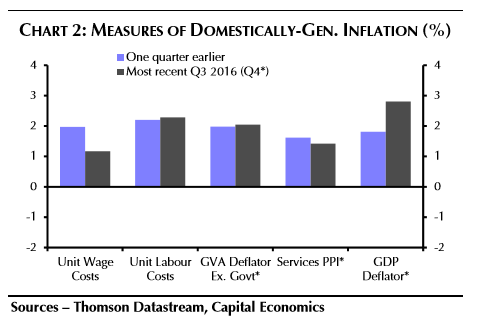

But the BOE’s optimism does not reflect recent data, which has actually shown a slight deterioration over the preceding quarter warns to advisory service Capital Economics.

They note how the Purchasing Manager survey data, for example, is showing a GDP growth of only around 0.4% in Q1 against BOE forecasts of 0.6%.

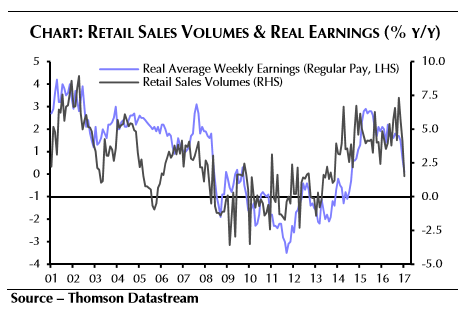

Retail sales have also slowed.

“Early hard evidence such as the surprise dip in retail sales volumes in January, adds to the view that the near-term risks to the MPC’s activity forecasts may be skewed to the downside,” says economist Paul Hollingsworth at Capital Economics.

The imminent triggering of article 50 could also cause uncertainty which is likely to impact on economic growth.

Sterling’s current rally may therefore be built on sand.

Ahead: Inflation Data will be Key

As far as upcoming data releases go, the main release for the Pound is the February CPI due for release on Tuesday, March 21 at 9.30 GMT.

Market expectations for a rise to 1.8% are a little low according to both Capital Economics and TD Securities, who estimate a higher 2.1% and 2.2% rise year-on-year in Feb.

The main contributory factors are likely to be rising food inflation due to the weak Pound and the lagged effect of the rebound in oil prices.

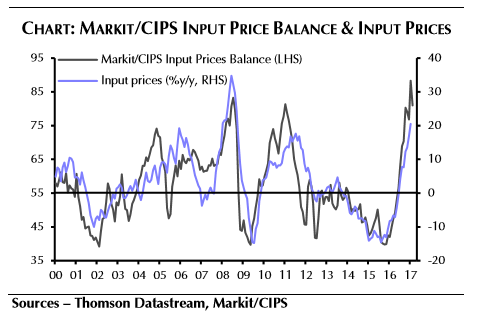

Producer Prices in the UK, out at the same time are expected to show continued extremely high yearly gains in ‘Input prices’ due to the rise in imported component prices because of the weak Pound.

Capital expect Input prices to rise by 21.7% year-on-year.

Manufacturers are not passing the higher costs on, however, as output prices are only rising at a fraction of the level, of 3.5% currently, rising to 3.8% according to Capital.

“Meanwhile, the survey evidence suggests firms have been taking a hit to their margins. Indeed, the output prices balance of the Markit/CIPS survey has not risen by nearly as much as the input price balance. As such, we expect output prices to have increased only a little further, from 3.5% to 3.8%.,” said Holingsworth.

On Tuesday, March 21 at 9.30 Public Borrowing data is released and should show a small 1.0bn rise in February.

Nevertheless, borrowing remains below previous forecasts – down 22% on the previous year allowing the public finances some breathing room.

Given the government’s U-turn on increasing National Insurance contributions from the self-employed and lower-than-expected borrowing, the government does now have a buffer it can use to stimulate the economy in case of a Brexit-related slowdown, factors Sterling’s current rebound may be based on.

The final big news release for the Pound is Retail Sales at 9.30 on Thursday, March 23.

“February’s retail sales figures are likely to suggest that consumer spending is on track for a disappointing first quarter,” said Capital’s Hollingsworth.

He further notes this appears to be as a result of a correlated fall in real earnings growth.

The consensus market estimate is for sales to have risen by 0.4% month-on-month and 2.6% year-on-year, whilst Capital are slightly more optimistic seeing 0.5% and 2.7% rises respectively.

Notwithstanding this slightly brighter forecast the remain pessimistic about the outlook for Retail Sales in Q1.

Outlook for the Euro

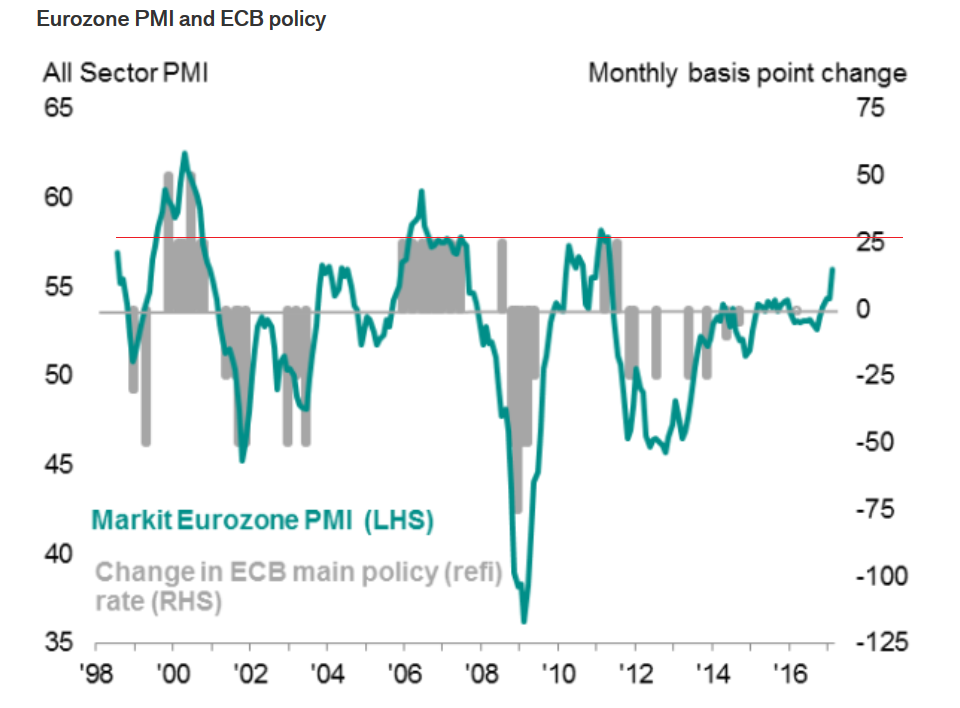

The week ahead for the Euro will be dominated by survey data, including Manufacturing and Services purchasing manager surveys or PMIs as they are known, which will be released at 9.00 GMT on Friday, March 24.

Recent surveys have shown such a marked improvement in responses that the indices are now almost at a level where historically the Euoprean Central Bank (ECB) tightened monetary policy by either raising interest rates or winding down direct stimulus efforts via QE, according to survey managers Markit.

This explains the comments from the head of the Austrian central bank Ewald Nowotny last week in which he suggested the ECB’s deposit rate should be raised.

Market professionals should keep an eye out for other ECB officials’ comments this week as they may move markets if they too call for a rise in rates.

Also, data showing pick-up of the European Central Bank’s Targeted Long-term Refinancing Operations (TLTRO’s), which provide discounted 4-year loans to banks could impact on the Euro in the week ahead.

Especially if they show strong demand as this may have a, “dampening effect on the Euro area’s interest rate landscape,” according to Raiffeisen Research’s Veronika Lammer.

Real yields – some would say a more accurate predictor of currencies - are already very low in the Euro-area, so a dampening of rates from excess bank liquidity is not going to help.

Allotment results will be published at 10.30 GMT on Thursday, March 23.

French Election

Political risk has subsided somewhat since the failure of the anti-euro PVV party to win in the Netherlands but analysts will still be keeping an eye on results from polls for the French Presidential election on Sunday, April 23.

At present centrist candidate Macron is tied with far-right candidate Le Pen for the first-round of voting.

Should they both go to the second round then there is a strong likelihood that Macron will win.

However, as we note here there is still a chance for Le Pen to win - and if this does happen then the Euro will come under immense pressure.