Bank of America say that while there could be further declines in the GBP to EUR conversion a solid floor to the declines is clearly visible.

- British Pound to Euro exchange rate today (markets closed): 1.1551, weekly best: 1.1631

- The Euro to Pound Sterling rate today: 0.8660, weekly best: 0.8724

The big question for our readers at Pound Sterling Live remains, "where will the GBP's decline end?"

While the weeks following the Brexit vote were followed by a flurry of downgrades to the currency's forecasts held at the major institutions we are seeing a new trend emerge as we head through August.

And that is one that sees many of the institutions calling a bottom to the declines.

In trying to answer that question we have brought a number of fascinating predictions, including most recently from Barclays, where analysts say the bottom in Sterling’s decline may have been reached.

This is also the view put forward by Nordea Market's Aurelija Augulyte who has cited a list of reasons to believe the bottom is nigh.

Fresh insight into the likely trajectory of the GBP/EUR exchange rate has been provided by the team at Bank of America Merrill Lynch Global Research.

FX analysts have seen a similar question being asked by their clients: “how much further can GBP fall,” and, “what conditions would be needed for a meaningful recovery in GBP?”

Latest Pound/Euro Exchange Rates

| Live: 1.1717▲ + 0.12%12 Month Best:1.1828 |

*Your Bank's Retail Rate

| 1.1319 - 1.1365 |

**Independent Specialist | 1.1553 - 1.16 Find out why this is a better rate |

* Bank rates according to latest IMTI data.

** RationalFX dealing desk quotation.

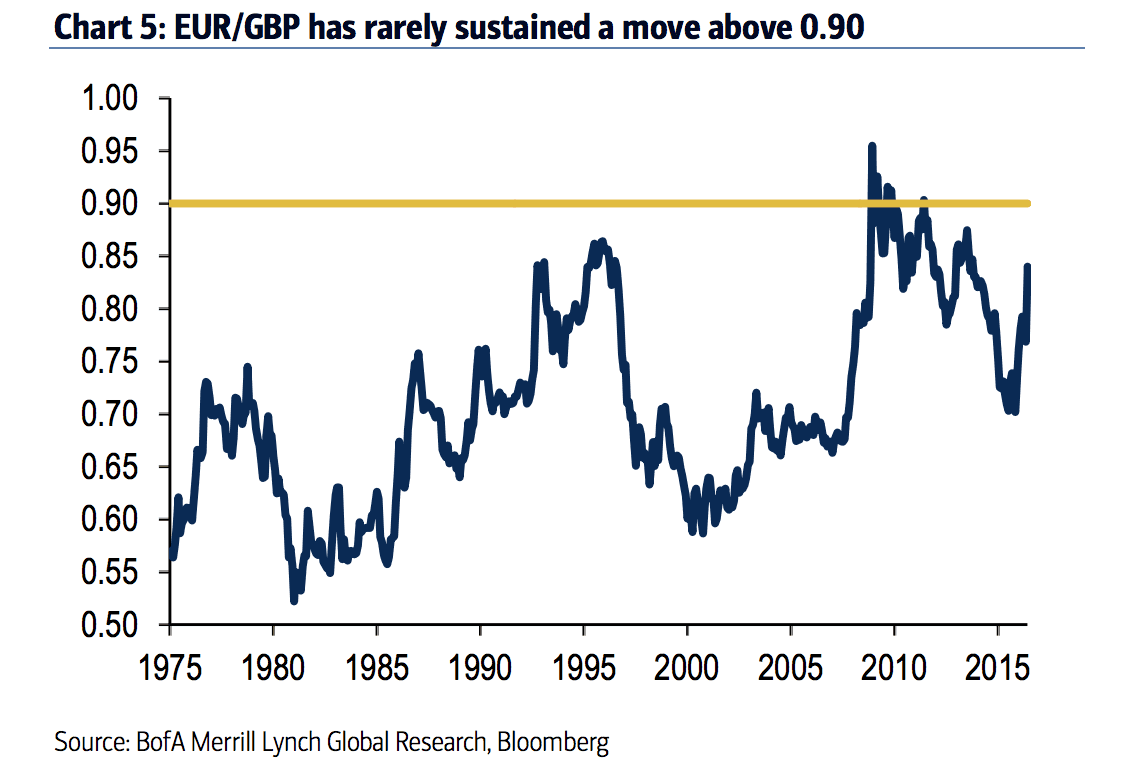

In addressing the outlook for the GBP/EUR exchange rate, Bank of America have firstly compared the current bout of GBP weakness with that suffered in the 2008 financial crisis where the high in EUR/GBP was 0.98.

This is a low in GBP/EUR of 1.0204.

“Through previous idiosyncratic UK crises, EUR/GBP has never sustained a break above 0.90 and we doubt it will do so again this time around,” says Kamal Sharma, FX Strategist at Bank of America.

0.90 equates to 1.11 in GBP/EUR terms (a level that Morgan Stanley have set their GBP/EUR downside forecast at).

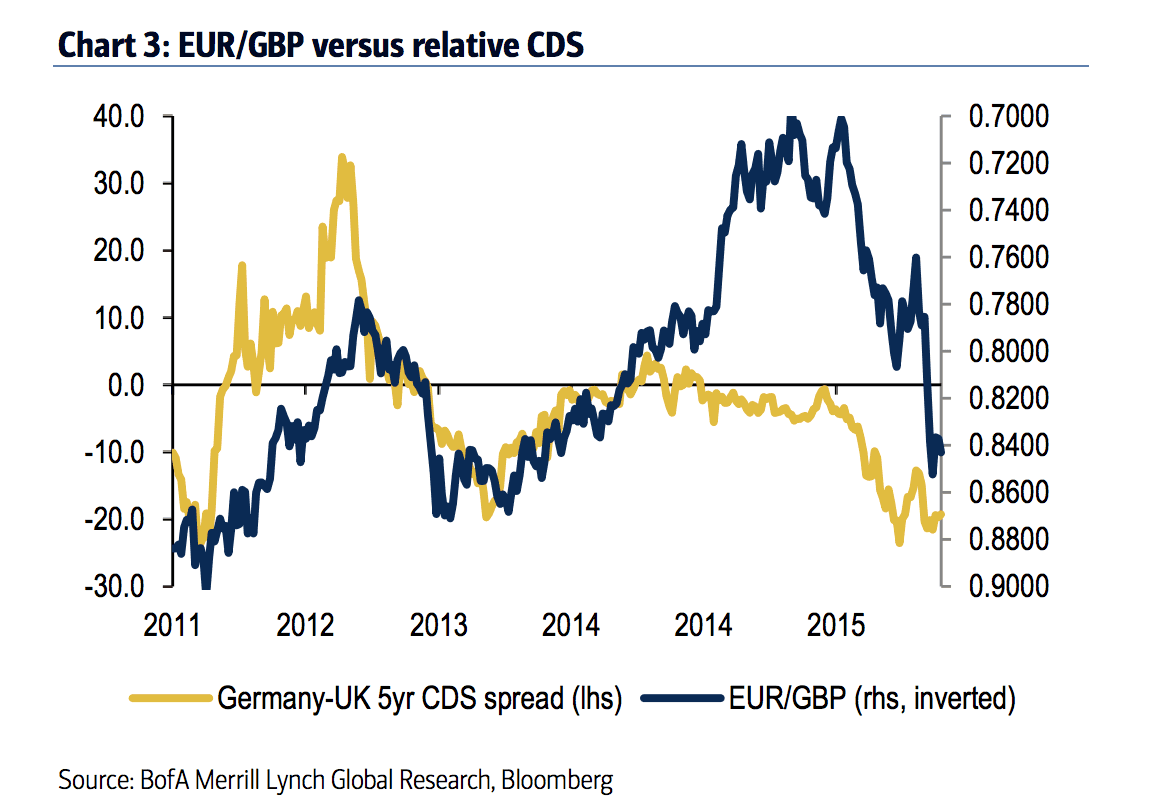

Sharma makes an important distinction between the nature of the 2008 crisis and the current Brexit vote shock.

In 2008, the sharp GBP depreciation was triggered by a significant threat to the UK banking sector which was countered by an aggressive Bank of England policy response (rate cuts and QE).

Rate differentials consequently moved markedly against GBP and in favour of EUR.

“We think this is unlikely to happen this time around and though we expect the Bank of England to once again deliver with renewed accommodation, our expectation for further ECB easing in the months ahead should limit the upside in EUR/GBP," says Sharma.

If we look at the rate differentials between UK and German bonds - an historically accurate driver of EUR/GBP - we note there is not much downside on offer:

Indeed, 0.88 would appear to be a good level of fair value based on the above. This is 1.1363 for those watching the GBP into EUR rate.

Therefore, if the ECB were to ease policy again (cut rates, boost quantitative easing) the Germany-UK 5yr spread could potentially move higher again, thus taking the Euro lower against the Pound.

Bank of America also remain concerned by the risks of political spill-over in Europe as the drumbeat of populism grows louder ahead of Austrian Presidential elections and the Italian Referendum later this year.

Therefore, while the Euro remains stable at present, it could be due a bout of volatility going forward.

Substantial Bad News Now Required to Push GBP Lower

Bank of America’s latest proprietary flows data suggest that investors are currently holding a record short in GBP relative to the one year look-back.

A 'short' is a position taken by traders whereby they profit on any declines seen in the currency in question.

Recent data from the CFTC also shows a similarly large GBP short in absolute terms with positioning equivalent to the size of shorts in 2013 (dovish Bank of England) and 2010 (UK general election).

Bank of America's recent Global Rates & FX Sentiment Survey, has meanwhile shown the asset management community has dramatically adjusted positioning in both rates and FX.

FX exposure in particular is currently the most underweight since the 1992 ERM crisis.

"The near-term positional constraints and the evidence from our sentiment metrics appear to be playing out in recent GBP price action with the failure of the GBP TWI to break through the 2011 and 2013 lows," say Bank of America.

This would suggest that positioning and sentiment are pricing in a large amount of bad news and that it would take a "substantial deterioration in news flow" to further weaken the pound in the immediate near-term suggest analysts.

The recent resillience of post-referendum UK economic data would suggest the bad news would likely not be economic in nature; if anything economists will be revising up their forecasts which were slashed in the wake of the EU vote.

We would therefore have to assume the greatest risks are political, and this would assume a poor outcome to EU negotiations.

We do know the PM May remains determined to draw out the negotiations for as long as possible.

However, whether an impatiend Europe will allow her to take her time remains to be seen.

Saying Sterling will Strengthen is Premature: Lloyds’

The Pound’s effective trade-weighted rate edged up by around 1.4% over the past week – from what was the weakest effective rate since the financial crisis.

Following the strong showing in the UK retail sales data many commentators reflected that the referendum result has not had the negative impact on the economy that many had been assuming.

We warned that a pro-Remain financial commentators and analysts were potentially guilty of tilting their forecasts too low.

Perhaps they are right, and vindication will come in subsequent data releases?

Pushing the latest warning are the economics team at Lloyds Bank who say,” this optimism seems rather premature.”

“Until additional ‘hard’ data allow the prospective growth deceleration to be gauged, the outlook remains highly uncertain, not least judging by the unusually wide dispersion of economists’ forecasts for UK growth,” says a note from the bank.

It will only be in September when we get the next set of economic statistics that can help determine whether Lloyds’ pessimism is correct.

The only notable data on the calendar for GBP in the week ahead is the second estimate of UK GDP for the second quarter.

This is not likely to be a market mover as 1) it is essentially old news and 2) it covers the pre-referendum period.