Such an outcome "should be positive for sterling" - Monex.

Image © Adobe Images

The Bank of England should keep interest rates unchanged for longer than the European Central Bank on account of divergent economic data, leading to a renewed rise in the Pound to Euro exchange rate.

This is according to a new analysis from international payments provider Monex, following the release of November PMI survey data , which showed the UK economy returned to slight growth in November.

By contrast, S&P Global - who produce the PMI reports - revealed the Eurozone economy likely contracted further, signalling the bloc was experiencing a mild recession.

"November’s flash PMIs once again support our view that the UK economy is merely in a state of stagnation as opposed to outright contraction, like that seen in the eurozone," says Simon Harvey, Head of FX Analysis at Monex.

Harvey says the Pound can rally against the Euro as a result.

The UK's composite PMI rose to 50.1 from 48.7, beating a consensus estimate of 48.7 and signalling slight growth. The Eurozone's PMI rose to 47.1 from 46.5, beating consensus at 46.9, but the reading is nevertheless consistent with economic contraction.

Following the data release, Pound-Euro rate rose to a high of 1.1516, although gains were pared during the course of the day to take the exchange rate back to below 1.15, placing it back in the middle of a range that is now one month old.

But Monex says the divergence in economic prospects between the Eurozone and UK will mean the Bank of England will hold rates for longer than the ECB, potentially boosting the Pound against the Euro.

"In conjunction with structural supply issues which should keep short-term UK rates higher for longer relative to the eurozone, we expect the UK’s better relative growth prospects to support renewed upside in GBPEUR," says Harvey.

Image courtesy of Monex. Track GBPEUR with your own custom rate alerts. Set Up Here.

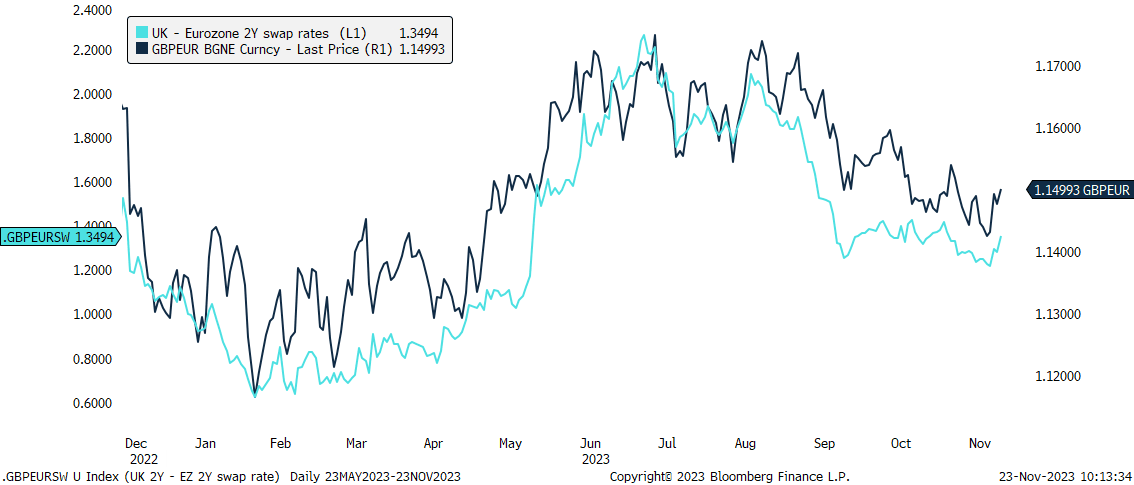

The above chart shows the difference between UK and Eurozone two-year bond yields has steadily fallen since August as markets lowered odds of further rate hikes at the Bank of England and raised expectations for rate cuts in 2024. This divergence has proven a solid indicator of Pound-Euro direction.

This divergence can reverse if bets for Bank of England rate cuts retreat, something members of the Bank of England's Monetary Policy Committee have been keen to encourage over recent weeks.

Of note, the PMI survey showed wage pressures at UK firms ticked slightly in November, breaking a spell of decline and putting pressure on the prices firms charge, lending weight to the Bank's messaging.

Furthermore, the UK's PMI reported a more resilient employment situation, whereas the Eurozone's pointed to job losses.

All this suggests UK inflation could prove stickier, thus justifying higher-for-longer rates at the Bank of England.

"Services employment marginally rose in November, ending a two-month period of reported job shedding by firms that weren't reflected in the original payrolls figures. As such, it is likely that November’s employment data is likely to show increased job gains," says Harvey.

He explains this further supports his view that growth is likely to remain stable at low levels and rates restrictive to prevent this reaccelerating inflation.

It also confirms his view that the Bank of England is unlikely to cut rates until the second half of 2024, which would prompt a repricing in money markets where a first hike was seen as early as May at one point last week.

Such an outcome "should be positive for sterling, especially against the euro, in the medium-term conditional the UK economy avoids recession," says Harvey.