- GBP/EUR supported near to & around 1.15 short-term

- Scope for recovery uncertain with multiple risks ahead

- New PM & policy agenda key for BoE & GBP outlook

- Crystallising energy supply risks loom for GBP & EUR

- Energy trouble heightening risks around ECB decision

Image © Adobe Images

The Pound to Euro exchange rate fell notably last week and whether it can find its feet again depends partly on if a returning Westminster Circus will be able to entice punters back during a week in which both Sterling and the single currency will also have a quagmire of other risks to navigate too.

Sterling entered the new week near to June lows but could benefit as soon as Monday if weekend remarks from the presumptive nominee for the post of Prime Minister lead to a revival of market appetite for the British currency.

This is after Foreign Secretary Liz Truss appeared to assure the monetary policy independence of the Bank of England (BoE) in an interview with the BBC, which potentially alleviates a significant market concern that many analysts and economists have cited for the Pound’s losses in recent weeks.

“It would be beneficial if the review helps avoid some of the mistakes of the past and assists the Monetary Policy Committee in orderly monetary normalisation,” writes Neil Williams, chief economist for the Official Monetary and Financial Institutions Forum (OMFIF).

“More sinister, not least for the pound and long-dated gilts, would be follow through on some of her other backers’ instincts,” Williams wrote in Thursday remarks about a planned review of the BoE’s remit.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of June recovery indicating possible areas of technical support and including selected moving-averages. Click image for more detailed inspection.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of June recovery indicating possible areas of technical support and including selected moving-averages. Click image for more detailed inspection.

The Conservative Party nomination for Prime Minister will be announced on Monday and there will inevitably be much focus on the possible implications for all policy areas but with analyst opinion divided, only time could tell how the cards will come down for the Pound.

However, the risk is of market scepticism or protest if campaign pledges of “immediate action” on the ‘cost of living crisis’ deepen the budget deficit while doing nothing to address an underlying energy price problem that results from more than just Russia’s invasion of Ukraine.

UK energy prices have risen to where they are because of inadequate supply and nonexistent storage capacity, a situation that exists partly due to the government’s slovenly planning system bureaucracy but possibly also due to its policies relating to climate change and carbon emissions.

“The jump in energy prices in August means we now expect CPI inflation to peak just above 16% in April 2023. Wage and inflation expectations have risen too, so we now see 50bp rate hikes in September and November,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

"We now anticipate a 1.2% year-over-year decline in GDP in 2023, driven by a recession in the first two quarters of the year, though we’ll tighten up our numbers when we know how Ms. Truss plans to proceed," Tombs and colleagues wrote in a Monday research briefing.

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of June recovery indicating possible areas of technical support and including selected moving-averages. Click image for more detailed inspection.

Above: Pound to Euro rate shown at weekly intervals with Fibonacci retracements of June recovery indicating possible areas of technical support and including selected moving-averages. Click image for more detailed inspection.

Whatever the new Prime Minister’s policies, there will be implications for Bank of England (BoE) interest rate policy and it’s possible that Sterling markets will be able to infer something about those when Monetary Policy Committee member Catherine Mann speaks on Monday.

She will participate in the 53rd Annual Conference of the Money Macro and Finance Society at the University of Kent and text of her speech is set to be released at 16:30 although Governor Andrew Bailey and others are also scheduled to appear in the House of Commons at 10:00 on Wednesday.

Government fiscal policy and central bank monetary policy have done few obvious favours for the Pound to Euro exchange rate in recent months.

“That could soon change given the upcoming change in government, as well as evidence that higher inflation expectations could be becoming more entrenched, which might prompt a more forceful response from the BoE,” says Michael Cahill, a G10 FX strategist at Goldman Sachs.

“Our baseline assumption is therefore that the most rapid phase of Sterling underperformance is now behind us, and look for some retracement in EUR/GBP. However, this implicitly assumes that a change in the policy approach is coming; if the upcoming announcements fail to impress, then we would look for the recent trend to continue,” Cahill said in a Friday research note.

Source: Goldman Sachs Marquee.

Source: Goldman Sachs Marquee.

While the week ahead is likely to be a formative one in terms of the outlook for the UK economy and Sterling it's no less significant for the single currency, which could make for choppy or even volatile trading in the Pound to Euro rate.

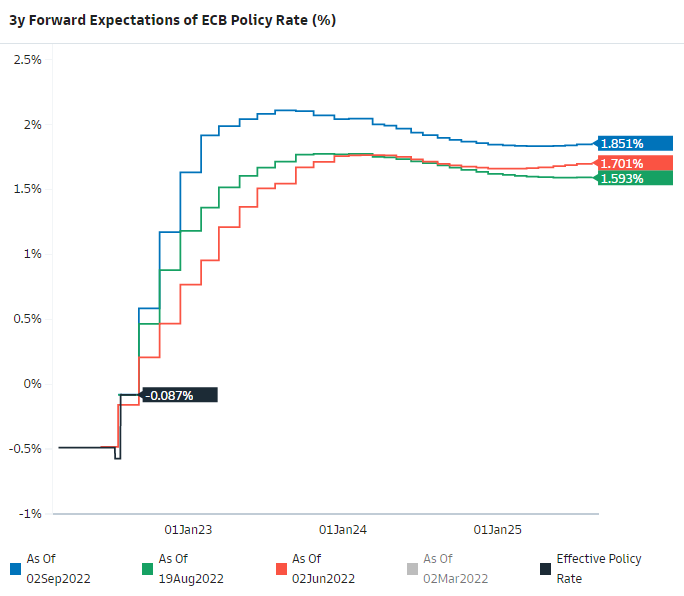

This is because of both the latest developments in energy markets as well as Thursday’s policy decision from the European Central Bank (ECB), which is widely expected to announce Europe’s largest interest rate rise to date but would be doing so now against a fundamentally changed economic backdrop.

Markets priced-in a high probability of a 0.75% increase in ECB interest rates after Eurostat said last Wednesday that inflation reached a record of 9.1% in August, although since then Russian state energy suppliers have suspended indefinitely their deliveries of gas through one important pipeline.

“Determining the appropriate amplitude of rate increases (50bpor 75bp) is complicated by Gazprom’s decision to indefinitely suspend gas flows via the Nord Stream pipeline to Germany. The ECB’s governing council is not indicating any consensus over rate rises,” says Brian Martin, head of G3 economic research at ANZ.

"It is a fine line, but our bias is that the ECB should prioritise its inflation mandate and try and prevent underlying inflation from broadening. A sustained rise in core inflation presents an endogenous threat to growth. Economically, the flow of gas is a supply issue over which the ECB has no control," Martin and colleagues said on Monday.