- GBP/EUR stifled & suppressed by economic headwinds

- BoE’s forecasts & rate outlook leave GBP/EUR stranded

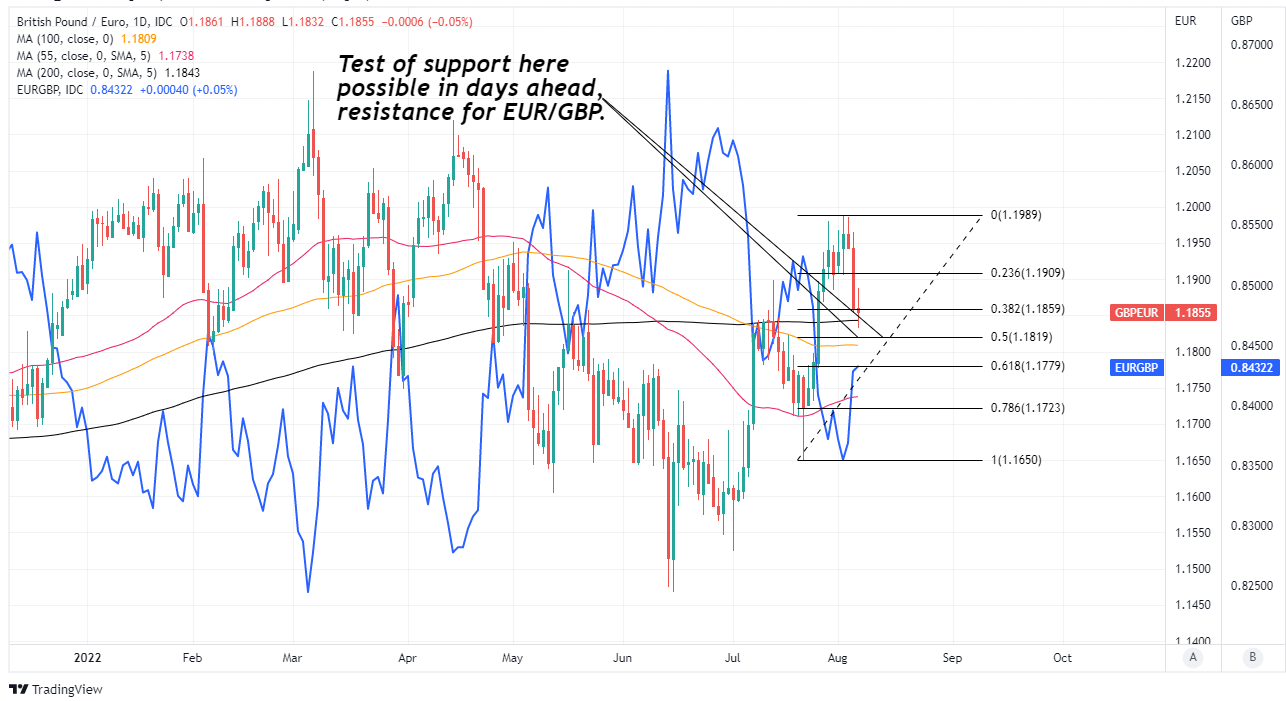

- Cluster of technical support levels beckons near 1.1800

- GBP/EUR consolidation possible as UK GDP data eyed

Image © Adobe Stock

The Pound to Euro exchange rate was stifled last week when the Bank of England (BoE) spooked the market with steep downgrades to its economic forecasts, forcing Sterling onto the back foot and leaving it at risk of slipping into a cluster of technical support levels around 1.18 in the days ahead.

Sterling had made another beeline for the 1.20 level early on last week as the Euro was given a wide berth after Russian gas supplies to Europe were reportedly cut further and as water levels on the Rhine riverway in Germany receded further, threatening another important source of energy supply.

But the Pound to Euro rate was brought back down to earth in abrupt fashion after the Bank of England lifted Bank Rate for a sixth time, taking it up to 1.75%, but warned of an imminent recession that it expects to last for more than a year.

“For the currency, it’s not a great outcome. Nevertheless, the market narrative to be short Sterling is very mature and positioned. It’s hard to see the new incremental negative driver,” says Paul Robson, European head of G10 FX strategy at Natwest Markets.

“A potentially underappreciated theme is that BoE projections are more realistic than either the Fed or ECB. The ECB could be showing very similar forecasts in a few months,” Robson and colleagues said on Friday before suggesting that clients buy into any further dips in GBP/EUR.

Above: Pound to Euro rate shown at daily intervals with selected moving-averages and Fibonacci retracements of July rebound indicating possible areas of short-term technical support for Sterling. Click image for closer inspection.

Above: Pound to Euro rate shown at daily intervals with selected moving-averages and Fibonacci retracements of July rebound indicating possible areas of short-term technical support for Sterling. Click image for closer inspection.

The BoE announced its largest interest rate rise since 1995 while citing concerns that domestic firms would continue to lift their own prices in response to inflation imported through energy and internationally traded goods prices.

But it also appeared to kitchen-sink its economic forecasts when projecting that the anticipated economic downturn will run as deep and last for longer than the recessions seen in both the early 1990s and the early 1980s.

“In our view, the weak UK growth outlook has been weighing on the performance of the pound all year. This has meant that the pound has not seen much benefit from the Bank having started its rate hike cycle sooner than many of its G10 peers,” says Jane Foley, head of FX strategy at Rabobank.

“Despite our negative GBP outlook, a lot of bad news is already in the price. By contrast we see risk that the market has not yet fully priced in the headwinds that are facing the Eurozone economy,” Foley said last week when reiterating a forecast for GBP/EUR to trade near 1.19 over the next three-months.

The recession forecast is a byproduct of household energy bills that are expected to rise in October to £3,500 per year or more, which will erode or otherwise eradicate households’ disposable incomes and in turn imperil the many other parts of the economy that are reliant on discretionary spending.

Above: Pound to Euro rate shown at weekly intervals with selected moving-averages and Fibonacci retracements of September 2020 rebound indicating possible medium-term technical supports for Sterling. Click image for closer inspection.

“The point of maximum recession risk will be in Q4 and Q1, when households will be reeling from a huge rise in energy bills. But with extra government support likely to be announced shortly after the new PM takes office, and households still holding considerable savings, a recession is not inevitable,” says Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

The BoE’s forecasts and its indication that it could continue to lift interest rates in the months ahead do little to encourage market enthusiasm or appetite for Sterling, although the outlook for the European economies and the single currency remain equally bleak.

This is something of an offset and cushion for the Pound to Euro exchange rate, which may also benefit from multiple nearby levels of technical support on the charts during any moments of weakness in the days ahead.

The week ahead calendar is devoid of major appointments for both Sterling and the Euro ahead of this Friday’s release of UK GDP data for June and the second quarter, both of which are expected to reveal economic contractions, although it’s not clear what implications these would have for Sterling.

“The consensus for a 1.2% month-to-month decline in GDP in June, driven by the extra public holiday for the Platinum Jubilee, looks too sanguine. We expect Friday's report to reveal that GDP dropped by about 1.6%,” Tombs warns.