Image © European Central Bank, reproduced under CC licensing

- IMF's Christine Lagarde to be next ECB President

- Seen as a 'continuity' appointment likely to weigh on EUR

- But, could be EUR positive if she can prompt broader reforms

Foreign exchange analysts are today mulling over the potential implications of future Eurozone monetary policy - and direction of the Euro - in the wake of the surprise news Christine Lagarde will likely replace Mario Draghi as European Central Bank President on November 01.

Lagarde - who is currently Managing Director at the IMF - was by no means favourite to replace Draghi owing to a lack of experience in central banking and she carries no formal training in economics or finance.

However, her appointment reflects 1) an apparent desire to balance the top jobs in the Eurozone between Germany and France, and 2) a perceived need to bring into the ECB someone who wields considerably more political influence than her predecessor. After all, she will be taking over the ECB just as its monetary ammunition runs dry, leaving a requirement for governments to start implementing the reforms required to sustain the Eurozone economy.

What does Lagarde's appointment mean for future direction in the Euro?

Initial reaction by the Euro exchange rate complex has been muted, but we believe the longer-term implications will be substantial.

On the surface, Lagarde is a continuity candidate in that she will likely maintain the direction of travel set by the outgoing Draghi team: namely ever-looser monetary policy to support a moribund Eurozone growth cycle.

The by-product of this exceptional stimulus is an undervalued Euro; therefore Lagarde's appointment is likely to prolong a multi-year period of underperformance by the Eurozone's single-currency.

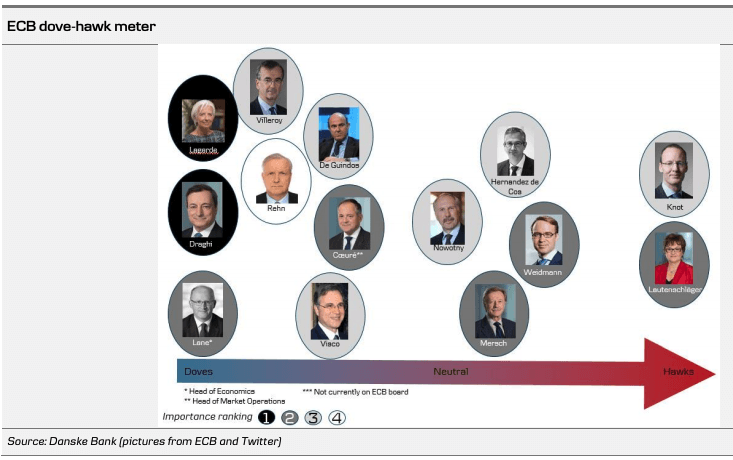

"The implication of her nomination can best be seen by looking at who her main competitor was for the post: Bundesbank President and uber-hawk Jens Weidmann. Clearly the authorities have gone for the dove, as her tenure at the IMF has shown. Net, this is negative for the Euro," says Marshall Gittler, an analyst with ACLS Global.

"The initial market reaction was a weaker EUR on the expectation that Lagarde will likely adhere to more dovish monetary policy. Judging by her more recent comments, that’s a defensible knee-jerk reaction," says Bipan Rai, North America Head of FX Strategy at CIBC. "Lagarde has been supportive of prior controversial ECB me asures such as asset purchases, and as recently as last month, called for more ‘patience’ from the Fed and the ECB."

"Christine Lagarde is certainly not Jens Weidmann and in that context will be seen as someone far more sympathetic to unorthodox monetary policy measures to boost economic growth," says Derek Halpenny, European Head of Global Market Research at MUFG in London.

Weidmann has long been the favourite to replace Draghi, and has over the years expressed his unease with the ultra-loose policy set by Draghi, instead advocating for higher interest rates, particularly as German savers continue to suffer under the current low interest rate regime.

But with the Eurozone economy failing to generate inflation and meaningful growth, it appears European leaders balked at the prospect of a so-called hawk taking the reins.

"We have reason to believe that she supports the ECB line, as she has been conveying the usual openness to the unconventional monetary policy of the IMF at several occasions. She supported Draghi and the ECB’s decision to launch QE in January 2015 and also called for other policy actions to play their role. She has also praised Draghi for his ‘whatever it takes’ commitment in 2012. That is a continuation of the ECB’s narrative," says Piet P.H. Christiansen, an analyst at Danske Bank.

"Christine Lagarde, head of the IMF, was nominated as the next president of the ECB. Under her leadership, the IMF was regularly advocating for further stimulus to aid the Eurozone recovery, so we would be inclined to believe that she would be willing to continue cutting rates, and even deliver more QE if need be in order to support growth and inflation," says a client briefing note from investment bank TD Securities.

For TD Securities, it is Lagarde's network and senior standing amongst the world's political class are expected to be an asset when it comes to pushing European leaders to implement the kind of policies required to boost the Eurozone.

Draghi himself has long said the heavy lifting cannot be left to the ECB alone, and that fiscal policy changes at government level must also be implemented.

But, change is often unpopular with the electorate and governments have understandably dragged their heals, aided by a hugely supportive ECB.

Perhaps under Lagarde the call for reform will finally find traction?

"In case of a recession in the Eurozone, her strong political connections at the highest level will be useful in advocating for further fiscal stimulus, given the limits to further monetary easing," says TD Securities.

Good for the Euro

MUFG's Halpenny acknowledges the consensus view that Lagarde's 'continuity' credentials make for a suppressed Euro, but warns "there are a number of reasons for caution here."

"President Draghi in June mentioned the need for governments to play a greater role in boosting economic growth, implying that the ECB can’t do it alone and that fiscal stimulus is now also required. Christine Lagarde at the ECB may prove more successful in orchestrating that in unison with EZ governments than other central bankers. That interpretation could provide support for the euro if early communications from Lagarde indicated this focus in policy direction," says Halpenny.

Indeed, we agree that markets would take it to be a Euro positive were notable reforms to be implemented by Eurozone governments: this would ultimately take the impetus of the ECB to keep interest rates low and could herald the start of a rate-raising cycle.

This would be an all-out positive for the Euro. "The popular view is that this is bearish EUR," says CIBC's Rai. "We don’t think the appointment of Lagarde means that an uber-dove is in place. We see a pragmatic, consensus builder that will rely heavily on the ECB staff for recommendations on measures."

Therefore, much rests with Lagarde's success in promoting broader reforms.

"Christine Lagarde’s role at the ECB could become even more influential especially if Lagarde could get some early success by persuading euro-zone governments to move toward some form of coordinated fiscal policy response to augment the ECB monetary easing on its way," says Halpenny.

"She has the political knowhow and gravitas to build bridges across the political landscape, collaborate with policy makers in various institutions, to the right policy mix. In other words, her experience and collaboration with other institutions may speak to her advantage and be exactly what Europe needs at this stage," says Danske Bank's Christiansen.

Danske Bank say despite the appointment there is little reason to believe the ECB will shift course and that Draghi's parting gift to Europe will therefore be another interest rate cut of 0.20% in September.

The September meeting could also see quantitative easing restarted, with Danske Bank anticipating €45-60bn to ultimately be pumped into the economy.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement