Image © Adobe Images

- GBP/EUR is breaking down again and showing signs of renewed weakness

- Momentum now oversold but not enough to signal reversal

- Pound could recover if market's have fully digested a Johnson win

- Watch Bank of England on Thursday

- Euro to be impacted by June PMIs, Sintra central banking conference

It's a busy week ahead for the Sterling and Euro and therefore volatility could be elevated: Sterling has the Bank of England and Boris Johnson to consider while the ECB's Sintra conference could see the Euro hit with a surprise. Technicals however advocate for further losses in GBP/EUR.

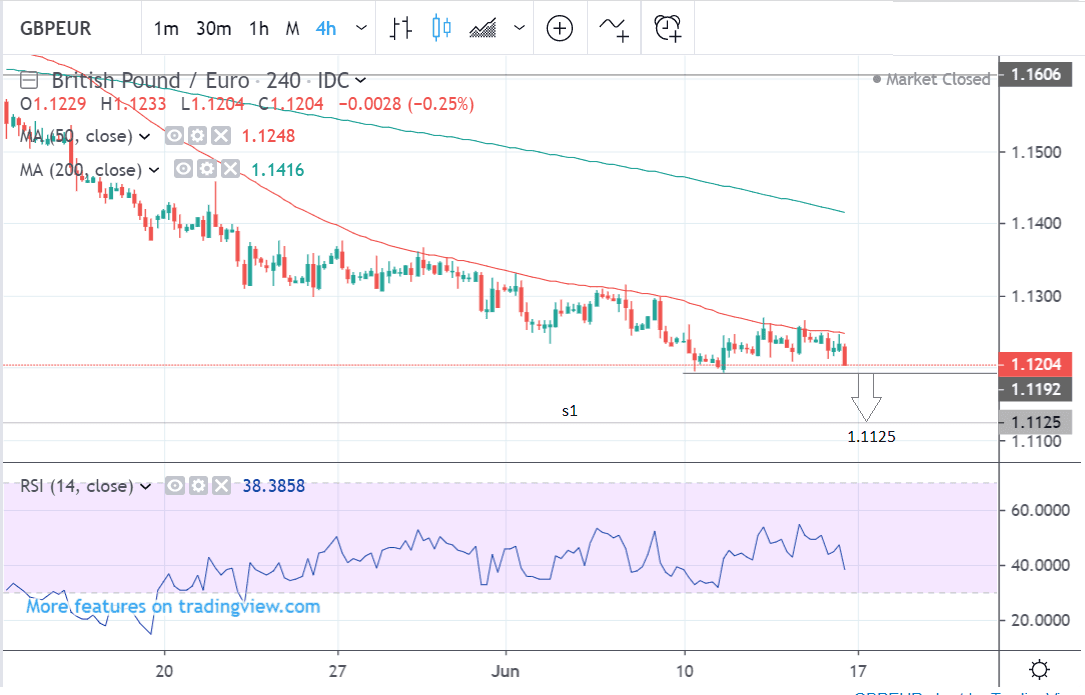

Pound Sterling is trading at around at 1.1204 against the Euro at the start of the new week, a quarter of a cent lower than the previous week’s close. Studies of the charts suggest the exchange rate is set to continue its downtrend in the days ahead.

The 4-hour chart - which we use to ascertain the short-term trend - shows the pair plateauing after a fairly steep downtrend. Yet given the old adage that “the trend is your friend”, it is eventually expected to renew its downtrend.

A break below the 1.1192 lows would provide confirmation of a continuation down to a target at 1.1125 in the short-term.

1.1125 is where the monthly pivot is situated, a level used by traders to gauge the strength of the trend. Pivots are also levels of support and resistance in themselves. It is a medium-strength support level which is likely to provide a floor for prices.

The RSI momentum indicator is starting to fall again which corroborates the short-term bearish outlook.

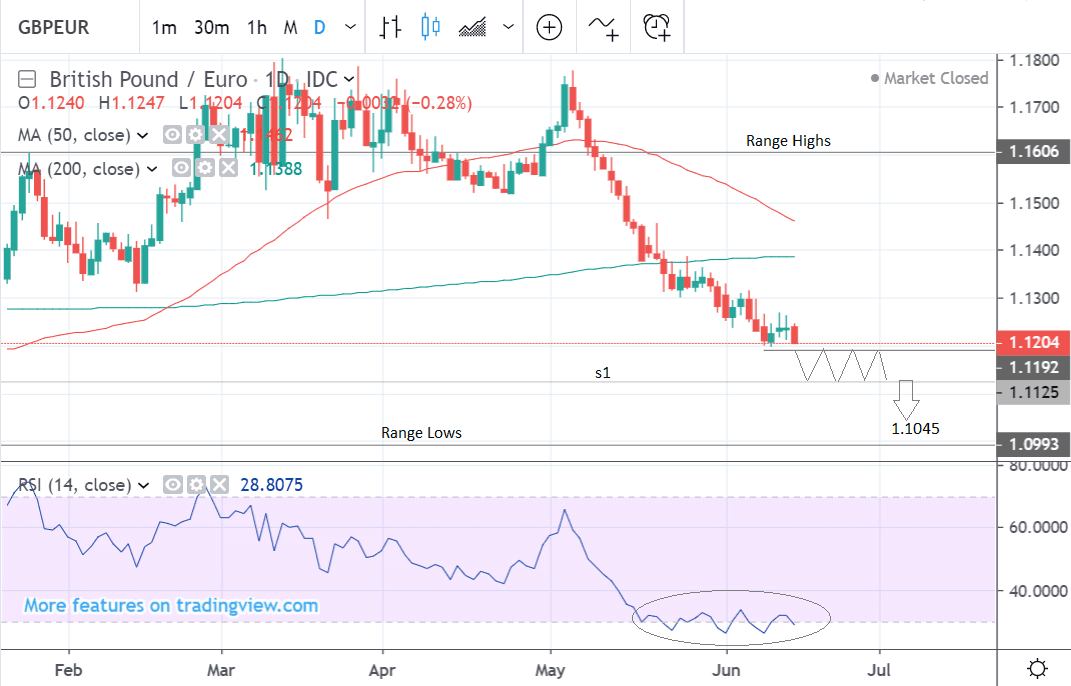

The daily chart tells a similar story - the pair is in an established downtrend which is likely to extend to a target at 1.1045 over the next 1-4 weeks.

The difference with the daily chart, however, is that the RSI momentum indicator is in the oversold zone, which is below 30, and this means the downtrend could be at risk of stalling over the medium-term.

It is highly likely that although it will go lower, the downtrend will now be broken up by periods of intervening, sideways consolidation.

Nevertheless, we still see it as likely to continue down to an initial target at 1.1125 first, and then after some range-bound trading, eventually to a second target at 1.1045.

We use the daily chart to give us an indication of the medium-term outlook which includes the next week to a month ahead.

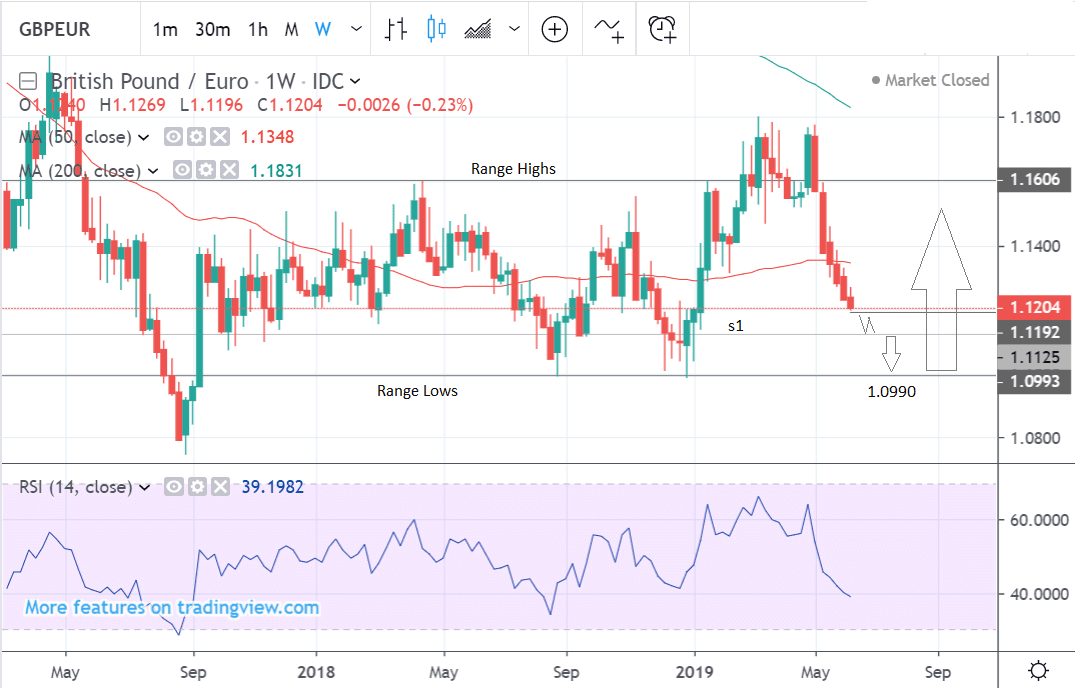

The weekly chart shows how the pair has fallen for five straight weeks in row. It also shows the longer-term sideways trend stretching back over years.

In the long-term, the pair will probably touch down at the 1.0990 range lows before bouncing and continuing to unfold within the parameters of its sideways trend.

We use the weekly chart to give us an idea of the longer-term outlook, which includes the next few months.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

The Pound: Boris 'in the Price'

Brexit politics is still likely to have the greatest impact on Sterling, with the Bank of England (BOE) rate meeting, CPI and retail sales data also likely factors driving the exchange rate.

The race to become the next Conservative leader and Prime Minister will continue next week with the vote to decide who goes through to the next round late on Tuesday, June 18. This time the seven remaining contestants will need at least 32 votes to get through to the next round.

More rounds of voting are expected on Wednesday and Thursday at which MPs will finally whittle the contest down to just two remaining candidates.

These will then be put to a vote amongst the wider Conservative party membership.

The first round of voting amongst conservative MPs resulted in a clear win for Boris Johnson, who gained 114 votes - significantly more than his nearest rival Jeremy Hunt, who came second with 43. Michael Gove was third with 37.

It is widely expected that Boris Johnson will win the wider vote amongst Conservative members. It seems highly likely, therefore, he will be the next Prime Minister.

Markets are more-or-less accustomed to this outcome by now, and we therefore wonder if this outcome is already 'in the price' of Sterling: i.e. it is not a Johnson win that will move Sterling, instead we believe it is what he says about his intentions on Brexit that will most likely matter going forward.

We know Johnson favours a renegotiated deal with the EU, and a 'no deal' Brexit is not his preferred outcome on October 31.

However, if the EU are unwilling to renegotiate he has indicated that he will pursue a 'no deal' Brexit.

Therefore a Johnson win is not necessarily bad for Sterling, instead the key issue going forward will be how the EU reacts to his advances for a renegotiation, and his subsequent response.

As such, be wary of a potential recovery in Sterling over coming days as there is a chance market's pare back on their expectations for a 'no deal' Brexit.

"BoJo is likely the new PM in UK once the dust settles after all the balloting over the next few weeks. The thing that we look forward to the most, is when BoJo takes May’s deal to the commons again, just with a new name. We would by the way prefer to buy GBP, once Boris is confirmed as the PM – buy the rumour, sell the fact (in EUR/GBP)," says Andreas Steno Larsen, an analyst with Nordea Markets.

Bank of England Meeting Could Prove Supportive

Another key driver of the Pound is the Bank of England (BOE) policy meeting on Thursday, June 20 at 12.45 BST. Although it is not accompanied by a press conference the minutes published after the meeting may contain important information which could drive Sterling.

The BOE has adopted a hawkish stance of late - hawkish meaning in favour of higher interest rates - owing to the country's solid Labour market. Higher interest rates would be positive for Sterling as they attract higher net inflows of foreign capital.

“Despite the growth worries, however, and the rising risks of a no-deal Brexit, the BoE is sticking to its central projection that some tightening in monetary policy will be needed over the next 2-3 years,” says Raffi Boyadijian, an economist at XM.com. “With no press conference or quarterly forecasts scheduled for the June meeting, the BoE is widely anticipated to repeat the same message in its statement.”

There are two risks: 1) that the Bank strikes a more cautious tone due to slowing global growth, largely resulting from U.S.-China trade tensions. This could send Sterling lower. However, we note the UK is less exposed to global trade dynamics than other economies, such as the Eurozone. Therefore, this risk might not come to pass.

Or, 2) the Bank strikes a more optimistic tone owing to the ongoing strength of the labour market that continues to generate increasing wages. This in turn threatens higher rates of inflation in the future. If the Bank notes this, the Pound could find support, or go higher.

CPI and Retail Sales

As mentioned, inflation is a key concern for the Bank of England, and by extension Sterling. The outcome of Wednesday's inflation numbers could therefore be important.

UK inflation data is expected to show a slower 0.3% and 2.0% rise on a monthly and yearly basis in May, from 0.6% and 2.1% in April, when data is released on Wednesday at 9.30 BST.

A higher-than-expected result might impact mildly on the Pound as it increases the chances of the BOE raising interest rates.

Retail sales are forecast to show a -0.5% and 2.7% change on a monthly and yearly basis in May, compared to the previous 0.0% and 5.2% changes respectively, in April, as the economy continues cooling.

A lower-than-expected result might impact negatively on the Pound as it would suggest the slowdown was more acute. Lower sales suggest a slowdown in GDP since consumers are the main driver of the economy.

The Euro: All Eyes on Sintra

The main driver of the Euro is likely to be PMI data with commentary from European Central Bank (ECB) president Mario Draghi and officials also potentially moving the currency.

The composite Eurozone PMI in June, which is a highly regarded gauge of activity in the main sectors of the economy, is likely to show no-change from the previous month’s 51.8, when it is released at 9.00 BST on Friday, June 21, according to consensus estimates.

The PMI is widely seen as a leading indicator for the economy and growth. If it comes out lower-than-expected it will weigh on the Euro and vice-versa if higher.

Individual manufacturing PMI is forecast to show a recovery to 48.0 from 47.7 when it is released at the same time as the composite.

The services PMI is expected to show a rise to 53.0 from 52.1 when it is released, also at the same time.

Expectations for monetary assistance from the ECB will only build if this week's PMI data are disappointing: this would be a negative for the Euro exchange rate complex.

Commentary from ECB’s Draghi could meanwhile impact the Euro when he speaks publicly at 18.00 on Monday, 15.00 on Tuesday and 15.00 on Wednesday.

"Markets will pay attention to President Draghi’s speech at Sintra next week; but already negative rates and uncertainty about future leadership complicate the ECB’s situation," says Christian Keller, an economist with Barclays. "Expectations for ECB policy easing are building as well but already negative rates and uncertainty about future leadership are complicating the ECB’s situation."

'Policy easing' refers to the ECB either cutting interest rate again or increasing their complex quantitative easing programmes: both are technically negative for the Euro.

Sintra, Portugal is the location of the ECB's Forum on Central Banking - an annual get-together of global central bankers. Back in 2017 Draghi and other central bankers signalled the time to tighten monetary policy - I.e. look at cutting quantitative easing and raise interest rates. This coordinated signal prompted some strong trends in global currency markets.

2019 could however see the opposite message adopted.

"Next week markets will certainly search for dovish signals," says Keller. "The extended forward guidance at last week’s ECB meeting to keep rates “at their present levels” until mid-2020 underwhelmed markets, prompting ECB officials in recent days to stress their readiness to act if necessary, be it through rate cuts and/or restarting QE."

* Advertisement