Image © Adobe Images

Britain's labour market continues to soften.

Wages are down and the unemployment rate is up: these are the headlines from Tuesday's release of UK labour market statistics.

The country's unemployment rate rose to 5% in March from 4.9% in February said the ONS on Tuesday, while adding the average earnings rate fell to 3.4% from 3.6%, a level that most economists agree won't worry policy makers at the Bank of England.

Meanwhile, more timely estimates for payrolled employees in the UK fell by 104K (0.3%) between March 2025 and March 2026, and decreased by 28K (0.1%) between February and March 2026.

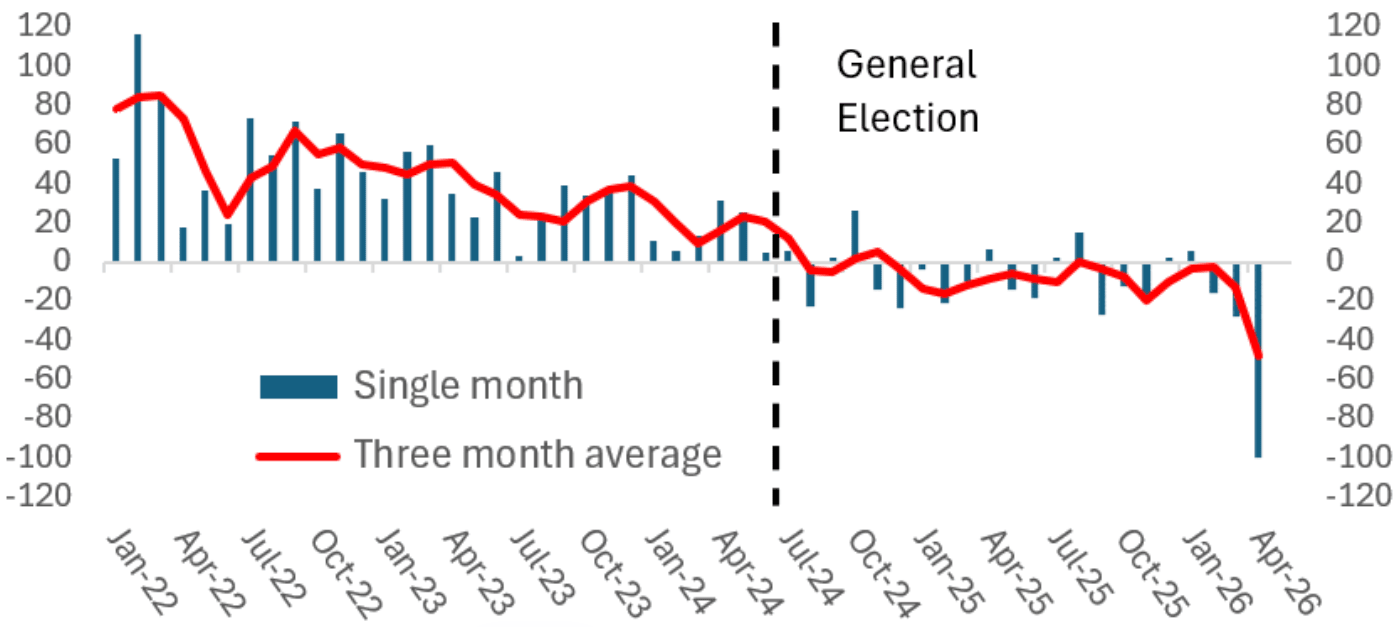

Image courtesy of @julianHjessop

"The latest ONS data offers the first tentative signs that the wider global economic backdrop is beginning to weigh on the UK labour market. After remaining broadly stable for much of the past year, vacancies fell by 28,000, taking them to their lowest level in five years," says Jake Finney, Senior Economist at PwC.

Economists at the British Chambers of Commerce (BRC) predict the labour market will deteriorate further, forecasting the unemployment rate to increase from 5.0% to 5.5%.

"A further drop in vacancies, now at their lowest outside the pandemic for more than a decade, suggests businesses are pausing recruitment. This is unsurprising as labour costs remain a key concern," says Patrick Milnes, Head of Policy for People and Work at the BRC.

For the Bank of England, today's data confirm there is no imminent need to raise interest rates as easing wages and rising unemployment can help lower consumer demand in the economy, which in turn reduces inflationary pressures in the coming months.

"The 100k (0.21%) m/m fall in payroll employment in April according to the provisional estimate will make the Bank of England (BoE) wary of pushing the labour market over a tipping point that triggers recessionary dynamics," says Andrew Wishart, Senior UK Economist at Berenberg.

Presently, the Bank is concerned that the spike in fuel prices that followed the war in the Middle East will creep into other segments of the inflation basket, thereby snowballing the effects of a conflict sparked thousands of miles away.

By raising interest rates, the theory goes, the Bank can put a lid on those second-round effects.

The market currently shows investors think the Bank will have to respond to these rising prices by hiking rates on at least two occasions this year, and maybe even three.

However, these labour data will go some way in countering that pricing if they confirm the chance of second-round effects are limited.

"In the UK, the MPC faces an uncomfortable trade‑off as another energy shock coincides with an already fragile domestic backdrop. Markets priced in as many as four hikes at one point, but we suspect the Bank will instead talk tough and stop short of tightening policy," says David Rees, Head of Global Economics at Schroders. "We doubt that growth will be resilient enough to force tough-talking central banks in Europe and the UK to raise interest rates."