Image source: Bank of England. Credit Laura Bell.

Goldman Sachs expects the Bank of England to hold rates through November and December 2025.

Instead, February's Monetary Policy Report looks to be the optimal date for another rate cut.

According to a new research note from Goldman Sachs economists, another cut in 2025 is off the cards because progress to get inflation lower has stalled, leaving headline CPI too high.

In addition, inflation expectations are uncertain, and the Monetary Policy Committee (MPC) wants to evaluate post-Budget data and early-2026 wage information before resuming cuts.

The Bank needs to see what the government is up to and awaits the November 26 budget, which should deliver a contractionary impulse to demand, meaning it can help in getting inflation rates lower.

According to Goldman Sachs the MPC will likely wait to see how strongly the budget weighs on growth and inflation before adjusting policy, meaning February is the first meeting with some credible post-Budget data to chew on.

Key members of the MPC, including Governor Andrew Bailey and Chief Economist Huw Pill, continue to stress vigilance on inflation and view the current Bank Rate as only slightly above neutral. If they see a benefit in waiting, then the MPC will likely comply.

Several members (Lombardelli, Greene, Mann) have argued for slowing or pausing cuts until the inflation trajectory is clearer.

There are reasons not to wait too long, however.

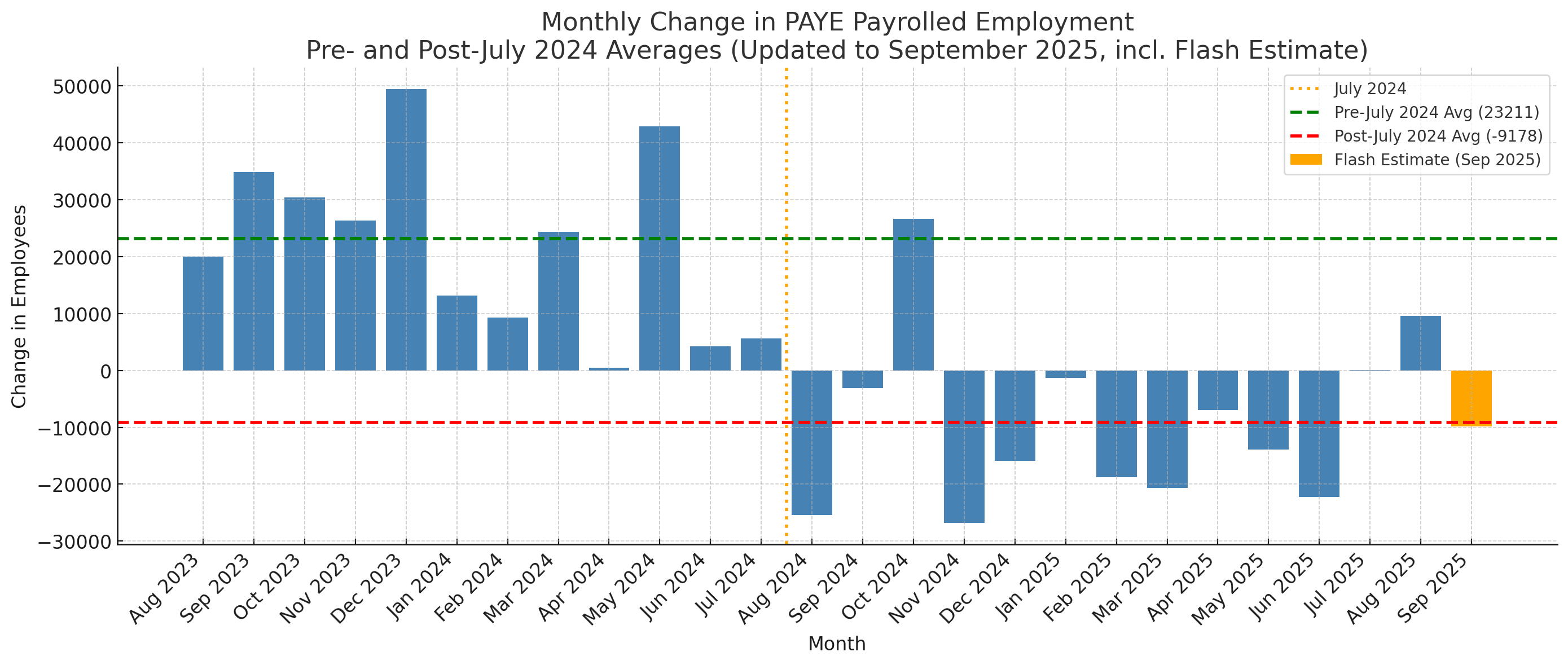

February emerges as the optimal date for a reduction in rates owing to persistent signs of labour market weakness: the UK labour market continues to soften, with the unemployment rate rising to 4.83% in August (from 4.66% in July) and expected to reach 4.9% at the next data release, exceeding the BoE’s estimate of the structural rate.

Above: The UK labour market has only added jobs in two of the months since Labour took power. Source: ONS PAYE series.

Forward-looking indicators such as the KPMG/REC and BoE Decision Maker Panel surveys also point to further loosening ahead.

Falling rates of employment inevitably point to easing wage growth pressures, which in turn limit's inflation's upside potential.

Private sector regular pay growth has slowed more than expected, dropping to 4.4% year-on-year in August from 6.2% in December 2024, and is likely to undershoot the BoE’s forecast of 4.6% for Q3.

Forward-looking pay surveys (Indeed, Brightmine, KPMG/REC, DMP) indicate additional moderation in wage pressures.

The 26 November Budget is also expected to take the pressure off inflation as it delivers around £30bn (1% of GDP) in fiscal tightening, up from £20bn previously projected.

This will likely come through tax-side adjustments and is expected to drag demand by around 0.3%, further cooling the economy and reducing inflationary pressure.

While underlying services inflation has stalled recently, Goldman expects “significant progress” in early 2026, as rent and wage-sensitive components ease and regulated price effects fade, creating room for the BoE to resume cuts.