Image © Adobe Images

Investors see a diminishing chance of a Bank of England interest rate cut in August following today's inflation release, but economists are nearly unanimous in thinking a 25 basis point cut will happen.

Both camps can't be right.

A Reuters poll published last week showed that 63 of 65 economists expect the Bank of England to cut rates by 25 basis points to 5% on Aug. 1. Yet the market attaches a 32% chance of such an outcome after the ONS reported Wednesday that UK services inflation remains stubbornly high.

Ahead of the inflation release that also revealed the headline rate had fallen to 2.0%, the market saw a little more than 50% chance of an August rate cut.

The Pound follows the market's lead and has risen in response to the paring of expectations for said cut. Thursday's Bank of England decision will be crucial as it could provide insight as to whether the Bank will err in favour of market pricing or attempt to bring market pricing in line with economist thinking.

"The markets vs economists gap should narrow, to the detriment of GBP, if any other Monetary Policy Committee members join Dave Ramsden and Swati Dhingra in voting for a rate cut on Thursday," says Robert Howard, a Reuters market analyst.

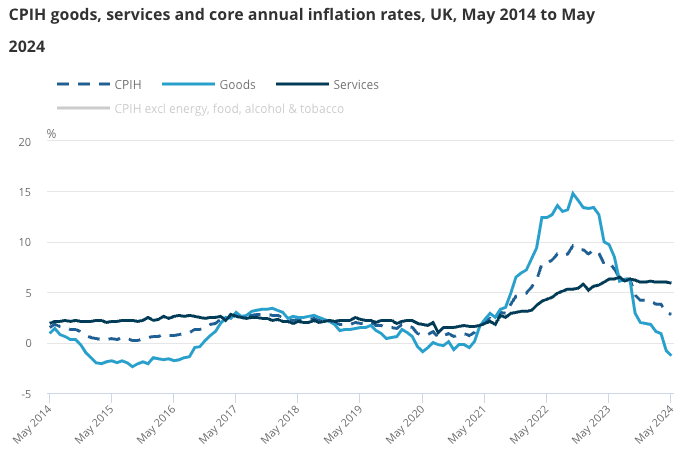

Above: If services inflation remains stuck here, headline CPI will rise again.

Caution will be in abundance amongst other members of the MPC, as the Bank will have to address the sticky services inflation print and acknowledge that headline inflation could well creep higher again over the coming months.

Services inflation is now the single most important UK data print on the calendar. In May, it came in at 5.7%, ahead of expectations of 5.5%.

The problem for the Bank is that once the favourable base effects of previous upside inflation drivers drop out of the comparison in coming months, headline inflation will start to rise again unless services inflation falls.

"Our base case has been for an August cut, but this will be reliant on these broader signals continuing to decisively soften over the next month’s data," says Victoria Clarke, UK chief economist at Santander CIB.

She explains the Bank of England needs more data to decide if it has a problem. "We think the Bank of England is left waiting for more reassuring data here, either in the shape of a more decisive moderation in services CPI or with all other broader signals on pay, jobs momentum and future price-setting pointing in a softer direction."

Gabriella Dickens, G7 economist at AXA Investment Managers, says the Bank will press ahead with the first cut in August, despite slightly stickier services inflation.

"Admittedly, services inflation remained sticky," says Dickens, but "we expect to see services inflation continue to tick down over the coming months, in part due to base effects following the chunky increases in 2023".

Additionally, AXA expects the headline rate looks set to remain around the 2% target in June, before ticking up again in July, as Ofgem’s Energy Price Cap falls by less than it did a year ago. The headline rate will probably rise no higher than around 2.5% in the second half of this year, as core goods CPI inflation remains in negative territory and food CPI inflation falls further.

"We remain comfortable with our call for the first 25 basis points cut in August, with a further one in November," says Dickens.