"A drift in medium-term inflation expectations is the development that monetary policy needs to firmly lean against and it should be a key yardstick for whether the MPC’s decisions are effective,” Catherine Mann, Bank of England Monetary Policy Committee.

Image © Pound Sterling Live

Some measures of UK inflation have continued to head in the wrong direction for the Bank of England (BoE) and in this context the details of its latest Inflation Attitudes Survey could be of significant concern to members of the Monetary Policy Committee (MPC) ahead of next Thursday's interest rate decision.

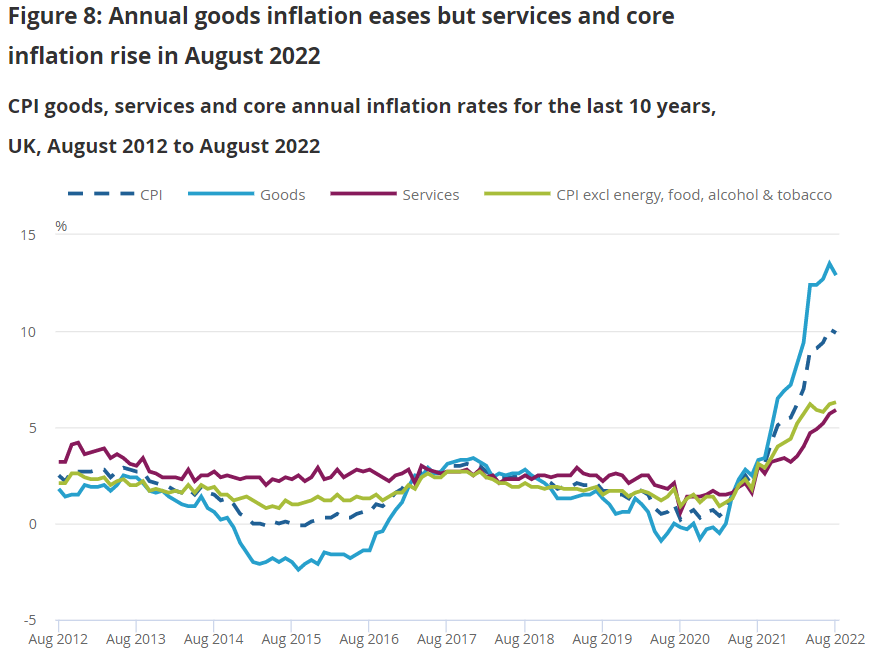

UK inflation was widely reported to have fallen from 10.1% to 9.9% when data for August was released by the Office for National Statistics (ONS) on Wednesday but what went widely overlooked or understated was the fresh upturn in the more important core inflation rate.

This latter measure excludes changes in volatile and currently exorbitant energy and food costs so is often viewed by economists and policymakers as a better guide to domestically generated inflation, which also means that August's increase from 6.2% to 6.3% has very likely aggrieved the BoE.

However, what may be even more concerning are the detail's of the Inflation Attitudes survey released on Thursday and covering responses given in the early days of August.

"Asked to give the current rate of inflation, respondents gave a median answer of 7.6%, up from 6.1% in May 2022," the survey results state in relation to question one.

"Asked about expectations of inflation in the longer term, say in five years’ time, respondents gave a median answer of 3.1%, down from 3.5% in May 2022," the survey results state in relation to question 2c.

Source: Office for National Statistics.

Source: Office for National Statistics.

The two above responses may well be the most concerning for the MPC because they underestimated the true rate of inflation for the relevant month (July) by almost two percentage points while also anticipating that price growth would remain far in excess of the BoE's 2% target even some five years ahead.

Responses to Thursday's survey were collected between August 05 and August 08 but at that time the most up to date inflation data available had been released on July 17 and concerned the month of June in which the overall inflation rate was reported as 9.4%.

June's inflation rate was 1.8% higher than respondents to the survey understood and the implication is that had those respondents known exactly how high inflation really was, their expectations of future inflation may have been nearly two percentage points higher including at the five year horizon.

All of this may seem trivial to readers but it's likely of great significance to the Monetary Policy Committee, given the BoE has stated clearly in all of its most recent policy announcements that its decisions to raise Bank Rate have also been aimed in part at keeping a lid on expectations of inflation.

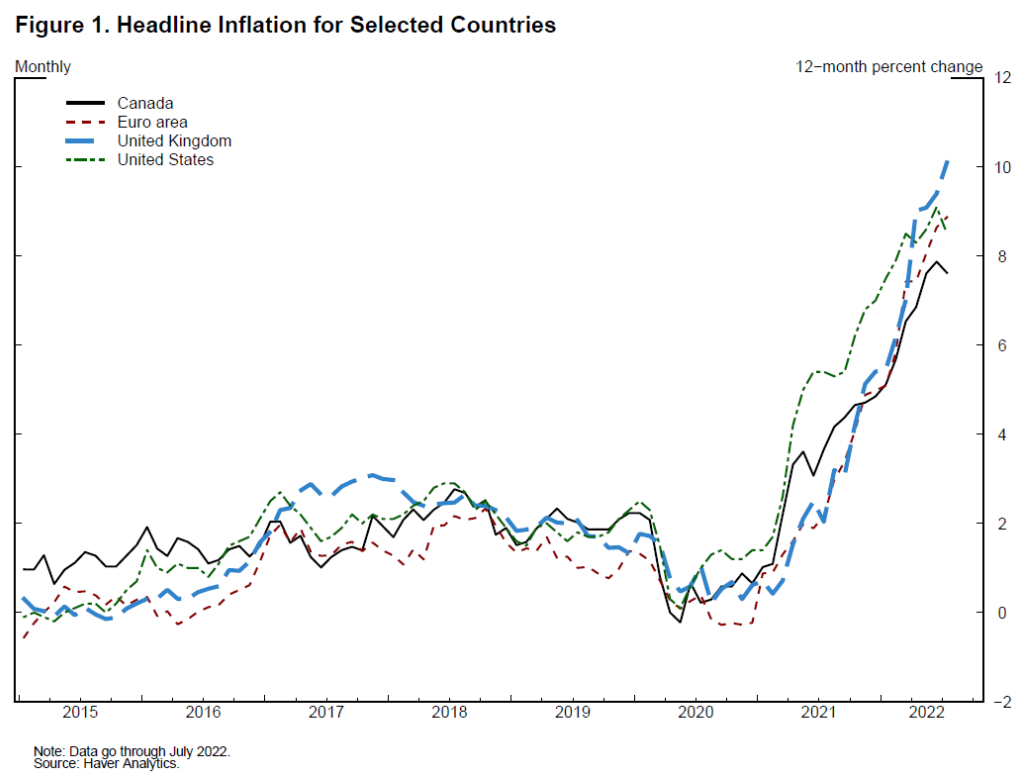

Above: UK inflation compared with other countries' inflation rates in July. Source: Federal Reserve.

Above: UK inflation compared with other countries' inflation rates in July. Source: Federal Reserve.

"Eight members of the Committee judged that a 0.5 percentage point increase in Bank Rate, to 1.75%, was warranted at this meeting. For these members, a more forceful policy action was justified. Against the backdrop of another jump in energy prices, there had been indications that inflationary pressures were becoming more persistent and broadening to more domestically driven sectors," minutes of the BoE's August MPC meeting stated.

"In a tight labour market and an environment in which companies were finding it easier to pass on price increases, a higher and more protracted path for CPI inflation over the next 18 months could increase the risk that an eventual decline in external price pressures would not be sufficient to restrain expectations of above-target inflation further ahead. Some of these members also judged that spending could be stronger than was assumed in the August Report projections," the minutes also stated.

Other than the upside risk, what's most notable about Thursday's survey expectations is that they are medium-term expectations, which are the most important because they can influence longer-term expectations and prices across the economy in a manner that can lead to permanent economic damage.

"A drift in medium-term inflation expectations is the development that monetary policy needs to firmly lean against and it should be a key yardstick for whether the MPC’s decisions are effective,” MPC member Catherine Mann told a conference at the University of Kent earlier in September.

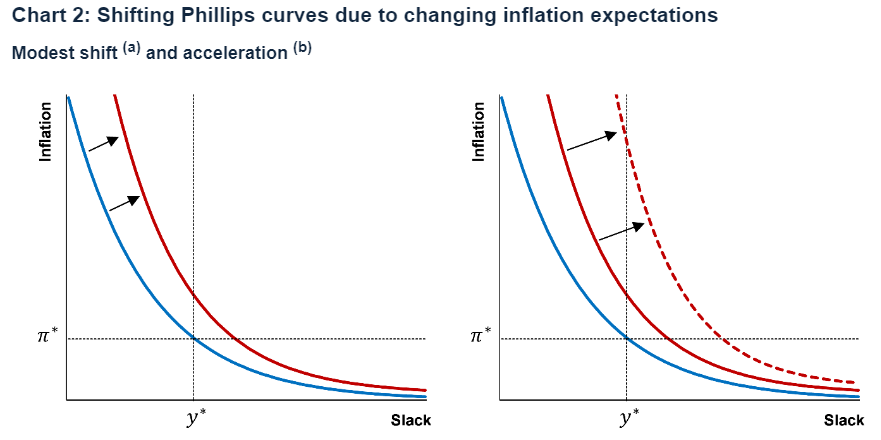

Source: Bank of England.

Source: Bank of England.

The above chart shows how higher levels of unemployment and lower economic growth potential can become permanent features of economies if and when any upward drift in short-term inflation expectations is allowed to go unattended to because it can neccessitate permanently higher interest rates.

"Looking through the lens of inflation expectations, achieving the remit depends on ensuring that inflation expectations in the short-term do not become adaptive, and that medium-term inflation expectations do not drift, so that long-term expectations remain anchored," Mann said.

"In the more nuanced formulation of the Phillips curve discussed below, inflation today does not simply depend on past inflation but depends as well on markets, firms, and household’s expectations, and crucially, how these expectations react to each other, are formed over time, and interact with our and others’ policy choices. The MPCs’ evaluation of inflation expectations therefore should take a central role in monetary policy decisions," she also later argued.

August's edition of the Inflation Attitudes Survey came one week ahead of a Septermber interest rate decision that many analysts and economists expect will see the BoE announcing its largest increase in Bank Rate thus far, and after the benchmark for borrowing costs was lifted to 1.75% back in August.