Above: Nadhim Zahawi is appointed chancellor of the Exchequer. Picture by Simon Dawson / No 10 Downing Street.

The arrival of Nadhim Zahawi at the Treasury could herald greater pay hikes for public sector workers, leading to increasingly embedded inflation expectations and more forceful interest rate hikes from the Bank of England.

Zahawi has been appointed Chancellor of the Exchequer by Prime Minister Boris Johnson, following the resignation of Rishi Sunak on Tuesday night.

Zahawi's control of the public purse strings could mean higher wage settlements for public sector workers as he had previously sought a 9.0% pay rise for teachers in his former brief as Education Secretary.

He confirmed to Times Radio on Wednesday morning he had been pushing for a 9% pay rise for teachers this year, and 7% next year.

"Now he’s Chancellor, he can grant that," says Tom Newton Dunn, Executive Editor of Talk TV's The News Desk, commenting on the Times Radio interview.

Such pay settlements come in an environment of surging inflation and the Bank of England has warned it is wary it could inflame domestic inflation expectations.

"According to media reports this morning, the new UK plan to deal with the “cost of living crisis” will be to boost public spending & cut taxes. Last time this was tried in the mid-70s, inflation rose even higher - to record levels. Expect the same if this policy is pursued again," says Andrew Sentance, Senior Adviser at Cambridge Econometrics and former member of the Bank's Monetary Policy Committee.

Christopher Graham, European Economist at Standard Chartered, says such wage hikes as envisaged by Zahawi could prompt the Bank of England into delivering successive 50bp hikes.

"Of particular importance will be what happens with public-sector wages over the summer period; specifically how the government responds to cross-sector demands for significant wage hikes," says Graham.

"Material government concessions would likely prompt more concern from the BoE about knock-on effects for private-sector wages," he adds.

The Bank of England's Jon Cunliffe meanwhile raised the prospects for an unusually large 50 basis point interest rate hike at the Bank of England in August by promising action will be taken to control inflation expectations.

In an interview with the BBC on Wednesday the Deputy Governor of the Bank said the Monetary Policy Committee will ensure that the recent surge in inflation does not become embedded in the economy.

"It's our job to make sure that as this inflationary shock passes through the economy we don't find that leaves us with inflation being the new normal, the sort of embedded psychology," he said.

"We will act to make sure that doesn't happen," he added.

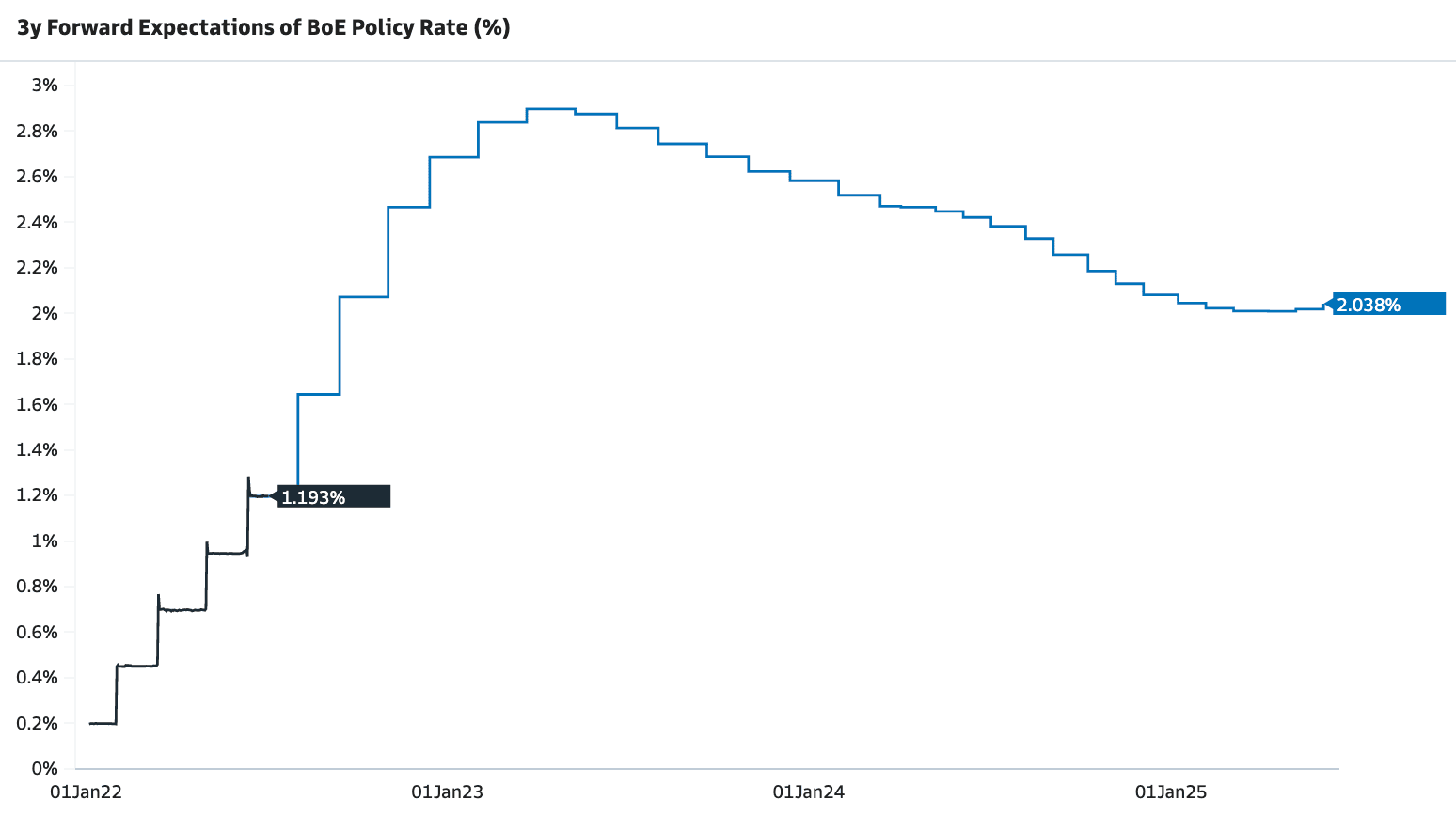

Above: Market implied expectations for Bank Rate. Image courtesy of Goldman Sachs.

The promise of action underscores market pricing for a 50bp hike in August as the central bank seeks to ensure inflation does not accelerate.

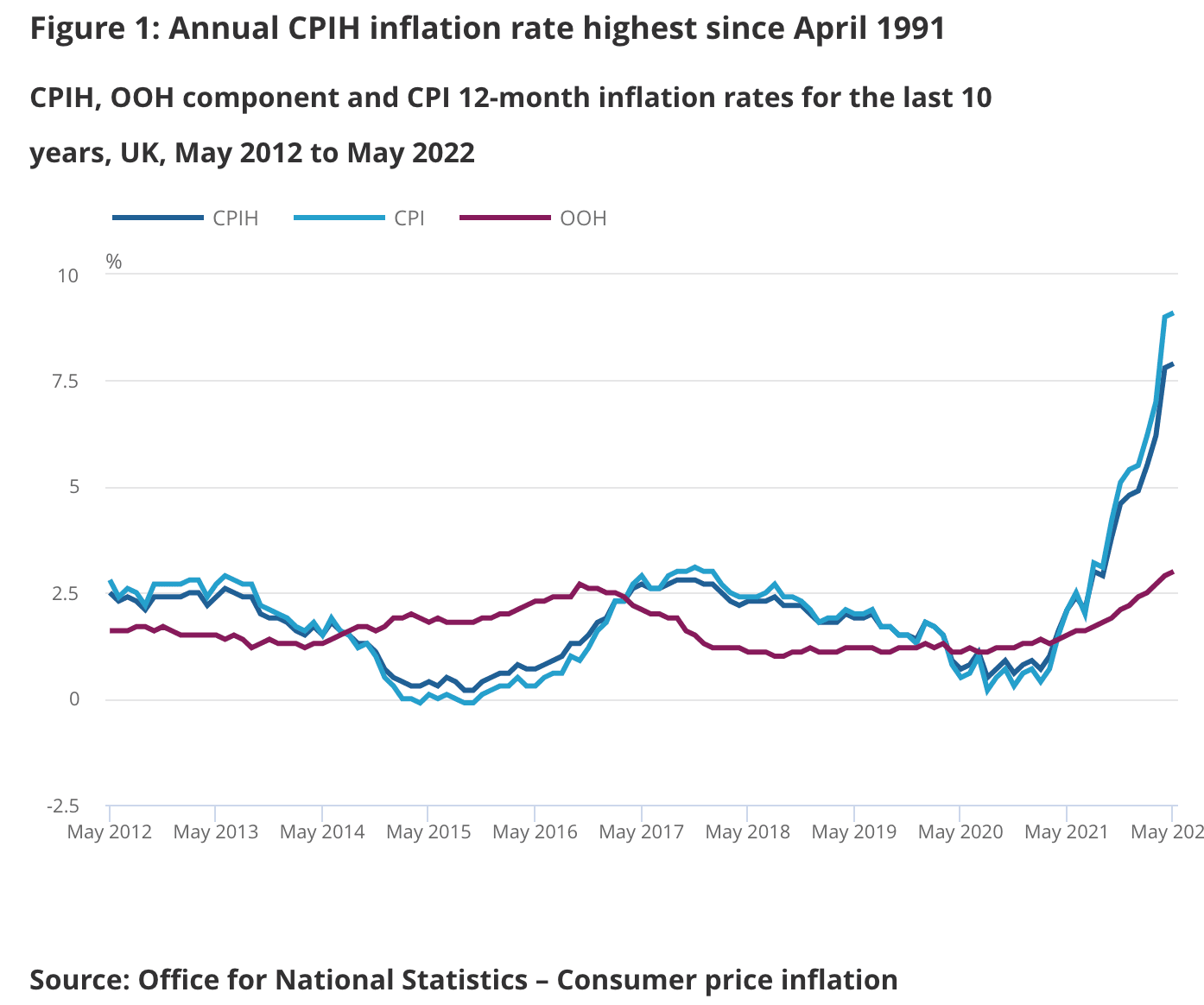

The UK saw inflation reach 9.1% in May and the Bank of England's June update showed forecasts for a peak near 11% in October.

The Bank said at the time of June's update - where it raises rates by a further 25 basis points. - that it would act "forcefully" if it saw signs of inflationary pressures becoming more persistent.

"We think a 50bps hike by the Bank of England (BoE) is now more likely than not in August," says Standard Chartered's Graham.

Analysts say the 75 basis point hike at the Fed in June will keep the pressure on other central banks, such as the Bank of England, to rapidly raise interest rates.

Standard Chartered also says market current market pricing (45bp currently priced in for August) and slightly better-than-expected economic data releases (June PMIs, May retail sales) means a larger hike in August is now their base case.

But Graham says a 50bp move will likely be a one-off event which would disappoint market expectations for two such hikes by November.

"We think September’s meeting will be a close call, but on balance still see a 25bps hike. However, this view is predicated on our expectation that headline growth data will show further signs of slowdown by then and labour-market data will begin to show signs of inflecting," says Graham.

He says any upside surprises on either the labour-market front or in inflation expectations could prompt another 50bp hike by the Bank.

Such a surprise could yet be delivered by the incoming Chancellor.