Image © Adobe Stock

UK economic growth forecasts are being revised lower and inflation forecasts raised as economists gauge the impact of Russia's invasion of Ukraine and subsequent international sanctions.

Initial assessments show that the UK has a relatively small direct exposure to Russia, although the fallout from surging oil and gas prices are seen as the most significant source of economic headwinds.

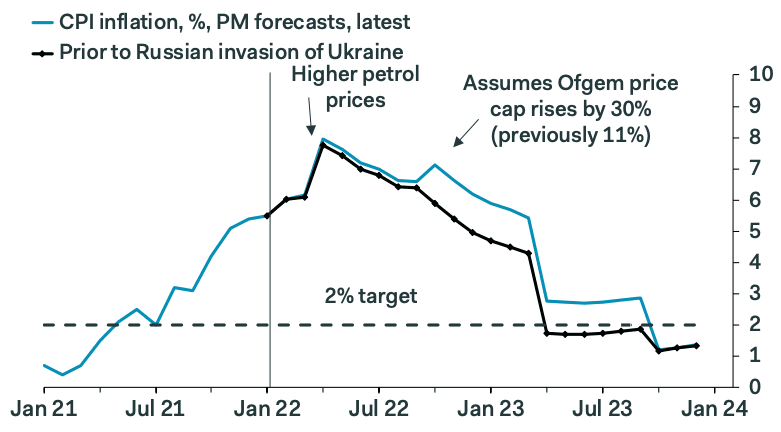

"The outlook for the U.K. economy has darkened following the Russian invasion of Ukraine. We have hiked our forecast for the peak rate of CPI inflation in April to 8.0%, from 7.7%," says Samuel Tombs, Chief UK Economist at Pantheon Macroeconomics.

The direct hit to the UK economy from UK and international sanctions on Russia is expected to be relatively contained, with analysts at Capital Economics say just $3BN (0.1%) of the UK banking system’s foreign claims are tied up in Russian banks.

This is far smaller than Germany, France and Austria.

Indeed, Bank of England Governor Andrew Bailey last week told the Treasury Committee that "the UK banking system’s exposure to Russia is very low".

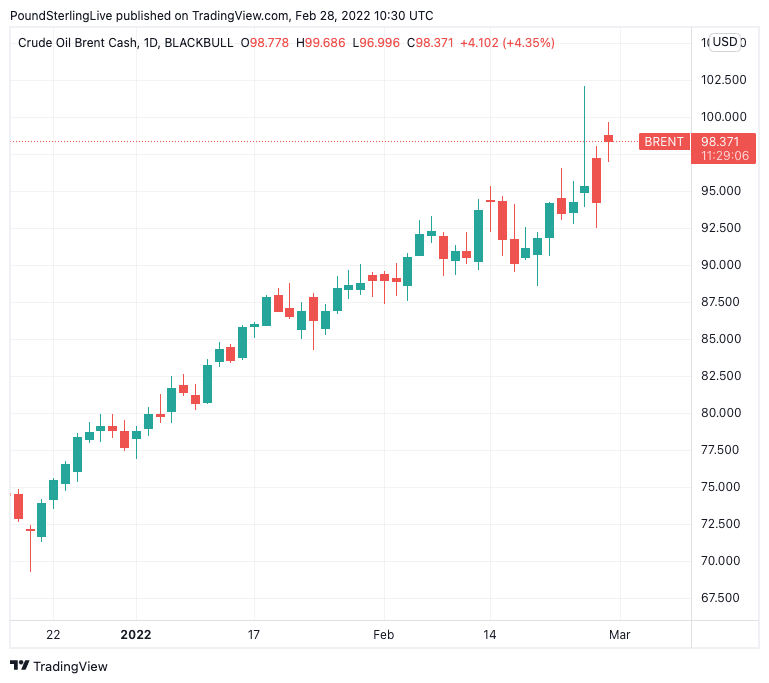

But oil and gas prices have risen sharply in the wake of Russia's invasion of Ukraine and weekend news of significant economic sanctions placed on Russia by Western nations and allies.

Above: The price of Brent crude in 2022.

Sanctions include was the ejection of the majority of Russian banks from the SWIFT financial commutations system and the isolation of the Central Bank of Russia.

This could make it harder for clients of Russia to pay for gas, oil and other commodity deliveries, potentially squeezing supply further and pushing up prices.

UK Business and Energy Secretary Kwasi Kwarteng on Monday said "unlike Europe, we're not reliant on Russian gas. But like others, we are vulnerable to high prices set by markets".

Higher oil prices will continue to be felt on UK forecourts and raise the costs of doing business while delivering another external inflationary shock.

The RAC on Monday reports that on Sunday the average price of litre of petrol reached £1.51 in the UK, a record and the first time it has gone above £1.50. Super-unleaded reached £1.63 and diesel went to £1.54.

The average full tank would now cost £83-£85.

"Global inflation is set to increase due to supply chain disruptions. In particular, oil prices broke through the USD 100/bbl level on 25 February and we believe that there is scope for these to continue rising towards the USD 150–170/bbl range," says Carlos Casanova, Senior Economist Asia at UBP.

Above: "Inflation to peak at 8.0% in April and only fall to 6.2% by year-end" - Pantheon Macroeconomics.

Goldman Sachs says short-term oil prices are on track to reach $110 - $120 a barrel.

"Barring a breakthrough in peace negotiations, we believe this leaves commodity prices having to rally sharply as we see demand destruction as now the only significant remaining balancing mechanism," says Goldman Sachs economist Damien Courvalin.

"Our 1-month Brent price forecast to $115/bbl (from $95/bbl previously), with significant upside risks on further escalation or longer disruption," he adds.

Pantheon Economics says big increase in natural gas futures prices meanwhile suggests that UK energy regulator Ofgem will increase its energy price cap by about 30% in October, well above the 11% increase we had previously assumed.

"The accompanying rise in global food prices and small depreciation of sterling will also boost overall CPI inflation," says Tombs.

Independent research providers Capital Economics have hiked their UK Inflation forecasts following recent developments, saying the Russian/Ukraine conflict is most likely to influence the UK economy via higher inflation.

"This threatens to keep CPI inflation further above the 2% target this year," says Paul Dales, Chief UK Economist at Capital Economics, referring to the Bank of England's mandated 2.0% inflation target.

UK CPI inflation was already at 30 year highs at 5.5% in January and is heading to 8.0% by April, according to Capital Economics.

Pantheon Macroeconomics have meanwhile revised up their forecast for CPI inflation in the fourth quarter of 2022 to 6.7%, from 5.5%.

The Bank of England is expected to be "unusually sensitive to any further signs that higher inflation is leading to higher price expectations and/or faster wage growth," says Dales.

Capital Economics says the existing inflation outlook may also prompt further hikes to 1.25% this year.

They think the Bank will either rise further or stay high, which is why they think the further rate rises to 2.00% next year are likely.

"Higher inflation caused by the Russia/Ukraine conflict may raise that risk," says Dales.

But Pantheon Macroeconomics are not so hawkish on their Bank of England interest rate forecasts noting that UK wages will struggle to keep up with inflation and the economy will also struggle more than expected.

They forecast GDP in the fourth quarter of 2022 to be only 1.5% higher than a year earlier.

"We doubt, therefore, that domestic demand will be strong enough for high inflation to become embedded. As such, we think the MPC will increase Bank Rate only to 1.00% by the end of this year, well below the 1.75% rate priced-in by the overnight index swap market," says Tombs.

"For now, we expect 25bp hikes at the next two meetings—March and May—but this timing might slip, depending on the fallout from events in Ukraine. We also expect the plan for active gilt sales to be set out in August, with sales starting in Q4 at a pace of £10B per quarter," he adds.

Oxford Economics says the prospect of higher inflation will stoke the Bank of Englnad's fears that a wage-price spiral will develop, but the additional squeeze on households also increases the risk of a more abrupt slowdown in activity.

A squeeze on incomes will lower growth in 2022-2023 and result in "very low" inflation on a medium-term timeframe (2023 onwards), according to Andrew Goodwin, Chief UK Economist at Oxford Economics.

Oxford Economics now expect only two 25 basis point rate hikes this year, in March and May, rather than the three they were expecting before this week's revision linked to the Russia-Ukraine crisis.