- Now is not the time to fret about spending say economists

- UK sets new Oct. record for borrowing

- Danger government front loads spending cuts, tax rises

Above: The Chancellor Rishi Sunak visits a Wagamama restaurant in central London after delivering the Summer Economic Update. Image © HM Treasury, Gov.uk

The government will potentially 'front load' its fiscal tightening agenda over coming months and years as it scrambles to try and plug the growing hole in its finances before the next election, according to economists who have reacted to news that shows an additional £21BN was borrowed in October.

The UK government has set a new October borrowing record of £21.58BN, according to latest official figures.

This is the sixth largest monthly borrowing figure on record as the government scrambles to plug the sizeable hole in its finances in order to fund its response to the covid-19 pandemic and its economy-crushing lockdowns.

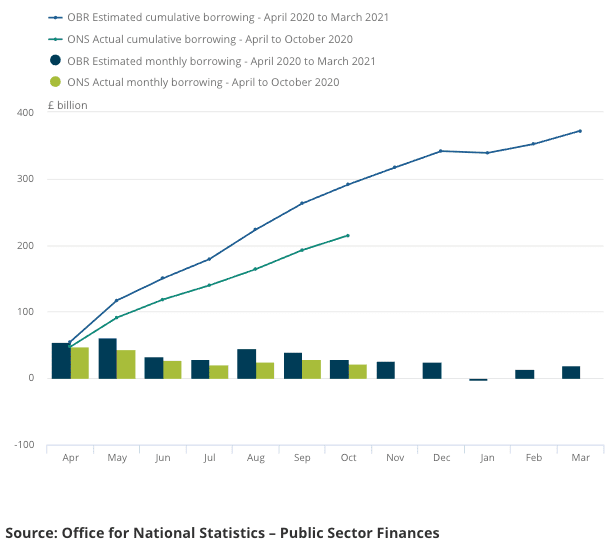

However, the figure of £21.58BN is notably less than the £29.50BN figure markets were expecting the ONS to announce and the debt-to-GDP ratio has fallen from 101.2% of GDP in September to 100.8% in October.

Furthermore, the borrowing data is coming in well below where the Office for Budget Responsibility (OBR) expected it to be at this point:

Regardless of the fact borrowing was less than the market expected and that the OBR might have to revise lower their projections, the scale of the growing debt mountain is still something to behold: in the first seven months of the fiscal year borrowing has reached £214.9BN, which is £57BN more than was spent in the whole of 2009/10, which according to analysis from Capital Economics was the worst year on record in cash terms.

The debt figures come amidst reports that the UK Chancellor Rishi Sunak is apparently considering freezing the pay of public sector workers for three years, in an attempt to get the country's finances under control.

"Rumours today that the Chancellor will freeze public sector pay in 2021/22 - implying falling pay in real terms - are a sign that fiscal policy likely will be actively set to modestly dampen GDP growth next year," says Samuel Tombs, Chief U.K. Economist at Pantheon Macroeconomics.

"The timing of the next general election - May 2024 - also highlights a danger that the government will front-load any required fiscal tightening so that it can ease off before the vote," he adds.

Pantheon Macroeconomics say borrowing will be much lower next year as a medical solution to the covid-19 pandemic is found in the form of vaccines, allowing the expensive income support schemes to finally end in March.

"Taxes likely will rise sharply in 2022, to attempt to stop the debt-to-GDP ratio from rising and to help meet some of the future costs of demography-linked increases in health and pensions spending," says Tombs.

Paul Dales, Chief UK Economist at Capital Economics says that despite the headline figures concerning spending, "low interest rates mean there is no need to rush to tighten fiscal policy."

"With with interest rates set to stay very low for the foreseeable future, we don’t think that will cause an adverse reaction in the gilt market or require the government to raise taxes soon. We expect the 10-year yield to be 0.50% at year-end," says Dales.

"While it is entirely understandable for there to be a debate about these unprecedented levels of public borrowing, one has to question whether now is the right time to do it, given that we haven’t as yet defeated the virus, or even got a vaccine programme in place yet," says Michael Hewson, Chief Market Analyst at CMC Markets.

"It’s hard to imagine that there would have been similar conversations being had in 1940, when the country was one year into the second World War, yet suddenly here we are fretting about the costs of an invisible pandemic that has the potential to wreak economic havoc for some time to come," he adds. "There will be a time to worry about how all of these emergency measures will eventually be paid for, however one has to question whether now is the best to time to be talking about this, at a time when businesses are having to deal with so much uncertainty".