Above: ECB President Mario Draghi is expected to announce the ECB is maintaining a policy of ultra-easy money supply at this week's policy event. Image © European Central Bank

- House prices have risen strongly since 2014

- Low interest rates set by the ECB are the catalyst

- Risk of a bubble forming, particularly in France and Belgium

House prices in the Eurozone are dangerously close to forming a bubble, says German lender Commerzbank, and the situation is only likely to get worse.

Analysis from the Frankfurt-based lender suggests a Europe-wide house price boom is one of the unintended consequences of the European Central Bank’s (ECB) easy monetary policy since the financial crisis.

By cutting interest rates the ECB has made lending excessively cheap and this has fuelled a rise in demand for mortgages, and consequently house prices, which have been going up consistently since 2014.

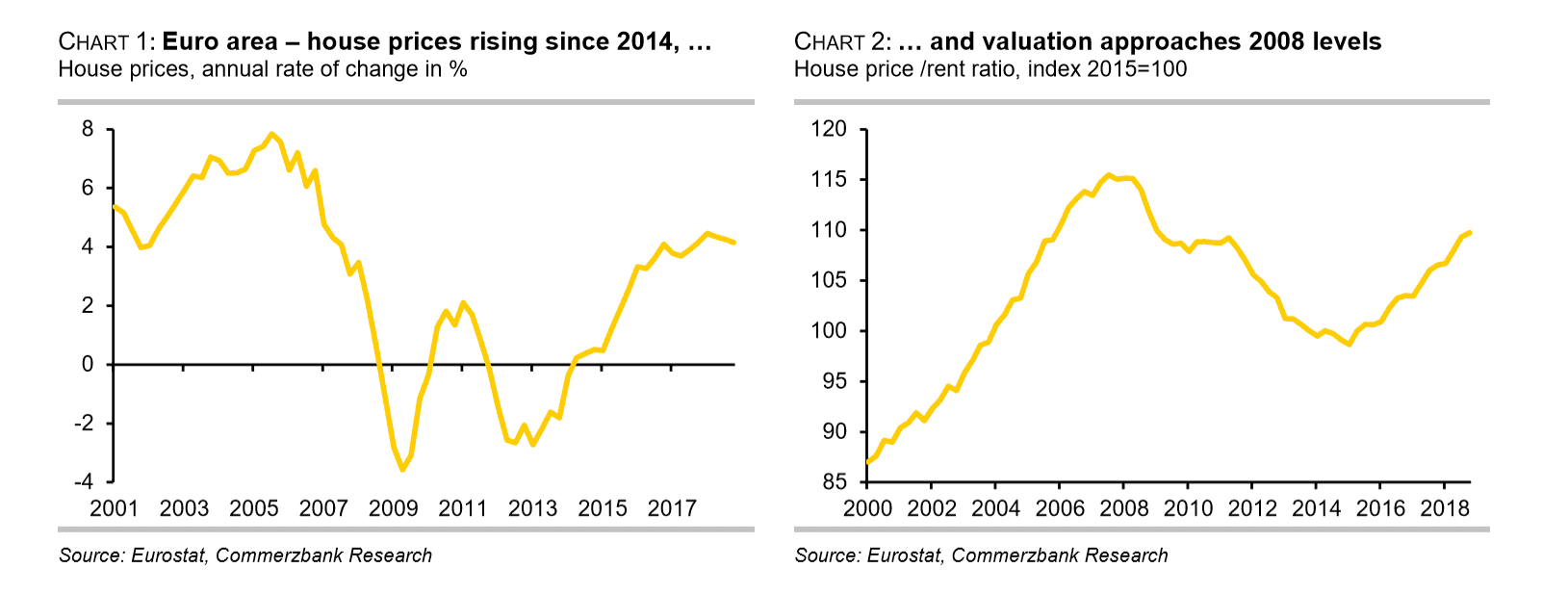

“House prices have been rising across the Eurozone since 2014 when the ECB's key interest rates approached zero and the first steps towards quantitative easing were taken,” says Dr Ralph Solveen, an analyst at Commerzbank.

This article comes a day ahead of the ECB's next scheduled policy decision announcement, at which policy-makers are expected to announce they will continue to sit on the current 'easy money' settings as long as necessary.

The chart below shows the rate of growth, both in annual percentage terms and using the house price to rent ratio.

The ECB is expected to continue to ease monetary policy by announcing an extension to its cheap loan programme (TLTRO III) at the June meeting on Thursday, June 6. It is also expected to keep interest rates in negative territory for an indefinite period of time.

Its reasons for doing this are subdued growth in the region itself and in the wider global context due to trade tensions. The continuation of this policy stance is likely to push house prices even higher, threatening a bubble.

A further consequence of the ECB’s policy is that by keeping interest rates low it makes the returns on “other financial assets” relatively less attractive, further fuelling demand for property, and creating a positive feedback loop which drives prices even higher.

House Fever

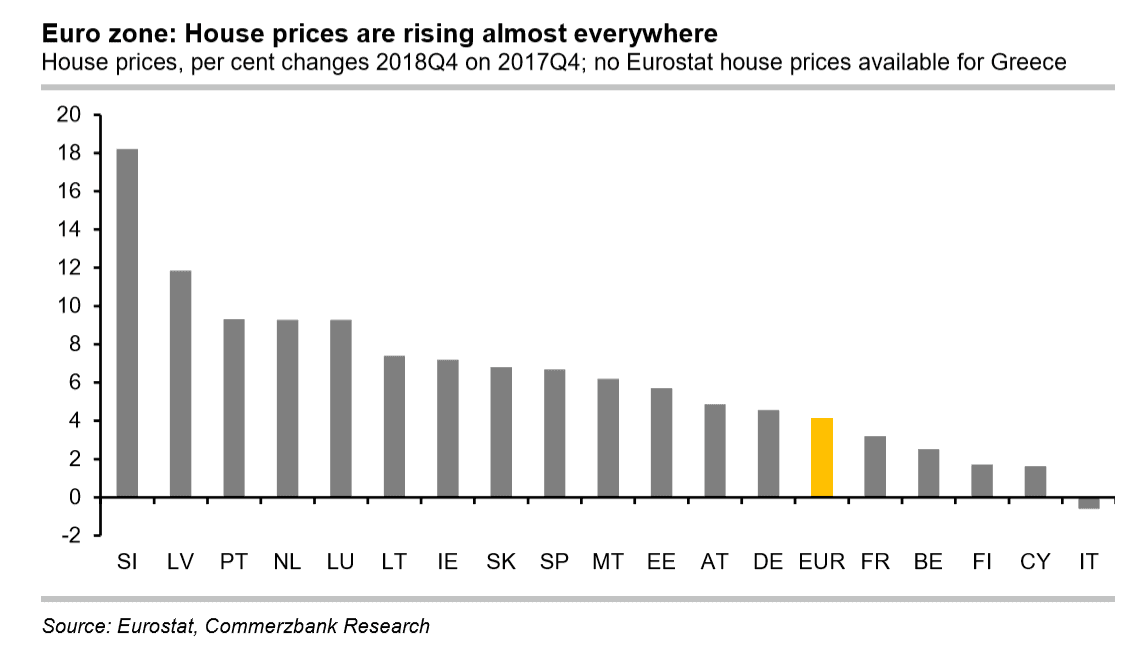

Between the end of 2017 and the end of 2018, house prices rose by an average circa 4.2% in the Eurozone as a whole, as shown on the chart below; which includes individual countries and also the Eurozone average (highlighted).

All the countries in the Eurozone participated in the rise bar Italy which saw a small decline.

Those that saw the biggest rises are Slovenia, where house prices surged 18%, Latvia (11.75%), Portugal (8.5%) and the Netherlands (8.4%).

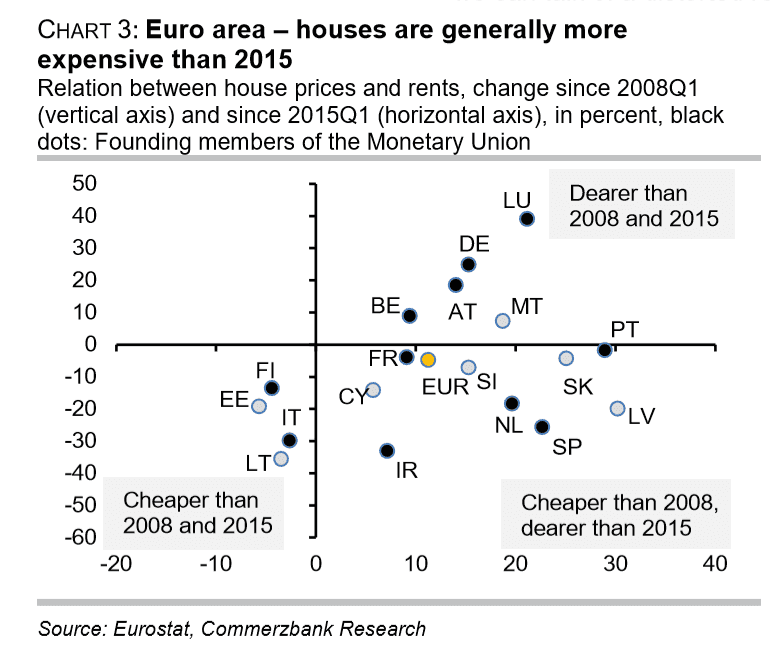

The most concerning rises have occurred in Belgium, Luxembourg, and France - from a bubble perspective. These countries experienced both a boom in the years following monetary union and again since 2014.

In addition, they did not correct that much after the great financial crisis (GFC), for this reason, Dr Solveen dubbs them as “long-term high priced”.

Also, concerning are prices in Spain and Ireland. These suffered a boom-bust pattern with a surge following monetary union followed by a crash after the GFC.

Although prices are still not as high as they were when the bubble burst in 2008-09, they were so elevated at their peak that they don’t have to reach those elevated levels to raise concern.

Less concerning are Austria and Germany where prices fell following monetary union. Even though they have also boomed since 2014, they have so from a lower base.

Italy and Finland are of least concern because house prices there have not participated in the post-2014 boom to the same extent.

Time to move your money? Get 3-5% more currency than your bank would offer by using the services of foreign exchange specialists at RationalFX. A specialist broker can deliver you an exchange rate closer to the real market rate, thereby saving you substantial quantities of currency. Find out more here.

* Advertisement

Great Financial Crisis Mark 2?

Given fears of a bubble forming what are the implications both for ECB policy and the outlook for the economy?

The ECB could respond to house price inflation in a variety of ways. Apart from raising interest rates which is a blanket response, they could also use more ‘surgical’ macro-prudential rules to limit lending, as has worked in Australia and other countries.

The ECB may not, therefore, feel under pressure to raise interest rates anymore quickly because of the risk of a house price bubble forming.

Given the close correlation between the Euro and interest rates, the single currency is unlikely to benefit, therefore, from a change in broad policy.

More concerning is whether a bursting of the real estate bubble could trigger a region-wide crisis, as happened in the Great Financial Crisis.

It seems less likely this time around, mainly because the risk profile of borrowers appears to be different now than it was at the peak of the housing boom in 2008/09.

Research from the European Systemic Risk Board (ESRB) which was set up by the EU in the aftermath of the GFC, suggests European homeowners now are older and have higher incomes than before the GFC.

This seems to indicate banks have tightened lending criteria to ensure another crisis does not occur.

“We find evidence of a considerable change in borrower characteristics since 2010: new borrowers have become older and have higher incomes than before the crisis in most countries,” says Jane Kelly, Julia Le Blanc, and Reamonn Lydon, researchers for the ESRB, in a paper “Pockets of risk in European housing markets: then and now”.

The homeowners most at risk from a housing crisis are those with high leverage. Pre-GFC these were more likely to be homeowners in ‘boom-bust’ countries like Ireland and Spain rather than other EU member states. This seems to have been what exacerbated bubble-formation and the crash in those countries in particular.

However, the ESRB does not find the same levels of high leverage either in boom-bust or in other countries, now, therefore the risk of a crisis is lesser.

The profile of the current property owner appears to be much more affluent than before, suggesting risks could be more easily absorbed.

“We do not find similar credit easing as before the crisis in either group of countries. Instead, there is some evidence that more affluent households have shifted their portfolios towards housing at a time when real returns on deposits or other forms of (less) risky investments are at an all-time low,” says the ESRB.

Finally, the rise in the house price to rent ratio is self-correcting, since when house prices rise to a high level relative to rents it becomes more financially prudent to rent rather than buy, according to Hamza Abdul- Samad a writer at Mashvisor, a property news and advice website.

As such, the current high level of the ration could act as a break on house prices.

* Advertisement