Some say the Canadian economy has stalled and so the Bank of Canada will slow the pace of its policy normalisation but others argue such concerns are overblown and the Bank will pursue higher interest rates.

Opinion is divided over whether the Canadian Dollar can continue the September bull run that propelled it near to the top of the G10 basket, posing a dilemma for those who are holding out for a better exchange rate in either direction.

The conundrum comes after recent data pointed toward a pause in the Canadian recovery and policy-makers began putting distance between themselves and the bullish mood that has gripped currency speculators since the Bank of Canada surprised markets with its second interest rate hike in early September.

“We suggested in the summer that “the market must be prepared for the hawkish case to recede as quickly as it materialised.” Whether it has receded remains to be seen; but it is certainly at risk,” says Neil Mellor, senior currency strategist at BNY Mellon.

In the absence of a consensus directional call from the analyst community, Canadian Dollar buyers should watch the value of the Loonie against the US Dollar for clues as to where other exchange rates might head next.

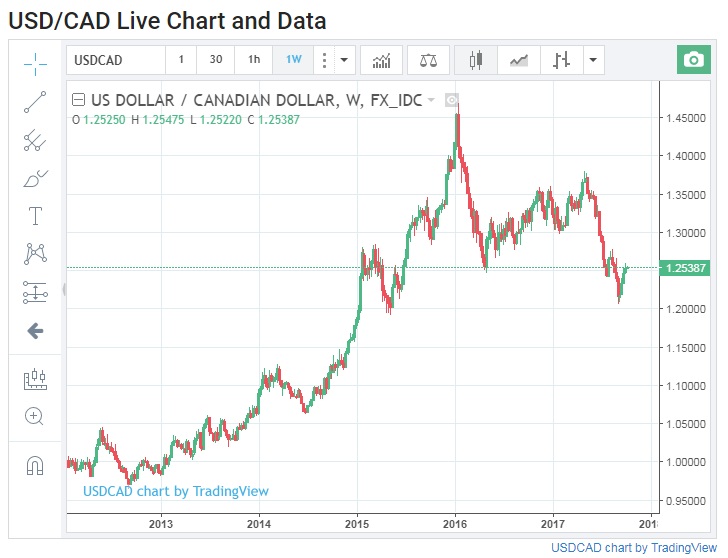

“CME data shows a net long, 78k non-commercial contracts in the CAD,” says Mellor. “A move toward and successful test of the late August high at 1.2662 would certainly leave such positions looking increasingly vulnerable to a sizable adjustment, thereby providing sustenance for a marked move lower in the CAD.”

There are grounds to think USD/CAD rate may go higher over the short term. The Federal Reserve has kept a steady hand of late and in its September round of projections, signalled to markets that it will stay a gradual course toward a higher Federal Funds rate.

Meanwhile, the Canadian economy saw economic growth grind to a halt in July, with GDP growth coming in at 0% for the month, thanks mostly to weakness in the oil and gas sector.

“Canadian data has become more mixed: spending has been holding up and the labor market remains the bastion of strength it has been all year. But the broader economy came to a halt in July and exports have now fallen for three months in succession, which points an accusatory finger at the CAD’s year-to-date performance,” says Mellor.

BoC governor Stepeh Poloz and his deputy Timothy Lane both struck an almost dovish tone in speeches at the end of September, warning of the effect a rapid strengthening of the Loonie can have on the domestic economy. The shift in stance came as speculators continued to pile on Canadian Dollar longs.

Many economists now expect the BoC will sit on its hands for a few quarters as the economy digests the two recent rate hikes that took the Canadian policy rate to 1%. One economist, at Capital Economics, has even forecast the BoC might reverse its recent hikes once into next year.

“If the BOC sticks with a “wait and see” stance as we expect, then it has all the makings for a fresh divergence play in USD/CAD. Two year sovereign debt spreads – which favored Canada last month for the first time since May 2015 – have bounced back sharply in the USD’s favor, and the bulls have taken full advantage,” says Mellor.

But not everybody has been spooked by the recent stall in Canadian data, the strength of the Loonie or the central bank’s focus on the currency.

The JPMorgan foreign exchange team has offered a view that is the fundamental opposite of the emerging consensus among economists and other strategists.

JPMorgan Says BoC To Keep Moving As Currency Strength Overhyped

Strategists at JPMorgan have written to clients saying they see the summer move in the Canadian Dollar as being in line with historical responses and the recent stutter of economic data as just a short term anomaly.

“The 4% USD/CAD retracement since 8 Sept is largely a convergent policy repricing of the USD towards CAD, rather than an unwind of the monetary bullish shift that had driven CAD’s repricing,” says Daniel Hui, a strategist at the US bank.

Hui forecasts the BoC will use its October policy statement to signal to the market an intention to pursue a continued gradual tightening over the quarters ahead.

“Recent comments regarding the currency, which recognize its inevitable influence in exports and inflation, but which also notes its endogeneity to the new policy stance and the improved macro outlook motivating it, to us do not constitute an active pushback,” says Hui. "Any shift in policy framework or rhetoric away from the still-relatively modest pricing in short-end CAD rates would be hard to square with the implicit comfort/urgency signaled by the recent back-to-back hikes.”

If the BoC eases off on the dovish rhetoric and continues to indicate further policy normalisation in October, Hui says the USD/CAD rate could fall below 1.20 around year end and may go as low as 1.1600 in the New Year.

“The assumptions behind this forecast remain the expectation that BoC remains on the path of at least quarterly hikes (and supported by the incoming data),” writes Hui. “This should lead benchmark BoC rates to exceed Fed fund rates (which are rising more slowly), and support a slightly steeper money market curve.”

Get up to 5% more foreign exchange by using a specialist provider by getting closer to the real market rate and avoid the gaping spreads charged by your bank for international payments. Learn more here.